Ninety One (asset management). Tough, tough year, but ...

Year on year comparatives grim. Price down 7% on results day, 40% since Jan ‘22. A deep-value diamond or 'structurally challenged mid-sized player'?

We know when the very first bullet point on a results announcement is “A year of significant headwinds”, the numbers are going be ugly. Indeed, for asset manager Ninety One (LON:N91), they were. In the FY ending 31 Mar 23:

Assets under management (AUM) fell 10% to £129bn;

Revenue fell 6% to £627m; and

EPS fell 19% to 18.2p (on the 17 May 23 closing price of 160.40p, that’s a PER of 8.8).

The CEO’s report stated: “The 2023 financial year has been difficult for our industry and for Ninety One. Coming off a record year in 2022, we faced the combination of higher inflation, the fastest rise in interest rates since we started the business, heightened geopolitical uncertainty, a liability-driven investing (“LDI”) crisis in the UK, significant bank failures in the developed world and energy shortages across the world. All of this led to unprecedented risk-aversion among asset owners. This created significant headwinds for a firm like ours, which primarily offers “risk-on”, public-market strategies. Furthermore, and regrettably, we have to mention the deterioration of economic prospects in our original home market, South Africa, where we have a substantial business… These circumstances have impacted our results, in particular, our net flows.”

All of that is valid, with Ninety One's AUM decline over the period being just below a London-listed asset manager peer group median.

[For a more detailed look at the UK-listed asset management sector over 2022 and in Q1-23, you may want to read my recent newsletters: Want to know how UK asset managers differ from each other? 2022’s bear market will show you!; and Tug-of-war between investment returns and net flows in Q1-23.]

Investors Chronicle didn’t mince words in its very-to-the-point take on Ninety One's results: “the shares have little immediate attraction. Sell.”

Of course, they might be right. But I think that might be a bit of a hasty take. Yes, it was a grim year for Ninety One. But when, even in such grim year, a business:

generates £213m of PBT at a margin of 34%;

has cash on the balance sheet of £380m and no borrowings;

produces a dividend yield of over 8%;

has a pretty low valuation multiple; and

its top-line AUM and revenue declines are undoubtedly mostly due to exogenous market conditions (which asset managers are by their nature exposed to);

I do think it’s worth a more detailed look.

Below, I’ll give a brief outline of the business and highlight some of the key points I’ll be digging into in more detail as part of my own research. (This is not investment advice, do your own research!).

Global asset manager with an EM slant

Ninety One has origins in South Africa, where it still has substantial operations as well as being listed on the Johannesburg Stock Exchange (in addition to its London-listing).

Over the years, it has expanded to become a global operation with around 40% of its AUM sourced from clients in Africa, 19% UK, 16% Asia Pacific and the Middle East, 13% Americas, and 12% Europe ex UK. It services these clients from 21 offices around the world.

It is an active investment manager, with a range of specialist teams covering equities (45% of AUM), fixed income (26%), multi-asset (17%), a South African fund platform (8%), and alternatives (3%). Around 57% of AUM is deployed in emerging markets.

Clients are mostly institutional investors such as pension funds (66% of AUM) with 34% of AUM coming from other clients via financial advisers. Interestingly, in FY23, nearly all net outflows were attributable to the institutional client base, with net flows from the advisor channel almost flat. The results presentation stressed that more than 50% of FY23’s outflows were attributable to three institutional clients ‘de-risking’ portfolios.

But despite a tough FY-23, Ninety One’s longer-term growth record is impressive.

Source (all of the above figures in this section and the above chart): Ninety One results presentation 17 May 2023

A return to top line growth is key

Looking forward, I think the key call for investors is whether the last year or so is a blip driven by particularly poor market conditions or, as in the opinion of Investors’ Chronicle and Numis (quoted in the IC article), the business is ‘a structurally challenged mid-sized player’.

Of course, cost control and margins are important, but the key driver of future cash flows for Ninety One is likely to be top-line AUM.

I think there’s two potential growth catalysts:

markets moving towards a more risk-on stance, which typically favours active managers, and

the relative attractiveness of Ninety One’s product suite compared to other managers.

Prospects for ‘risk-on’ and ‘active’

CEO Henrik du Toit took a cautious position on this one in the results presentation. He said while he isn’t seeing a major change in risk appetite among clients yet, he thinks market conditions have stabilised, that the major risk adjustments in client portfolios have already happened, and that more ‘normal’ allocations by asset owners are now likely to return.

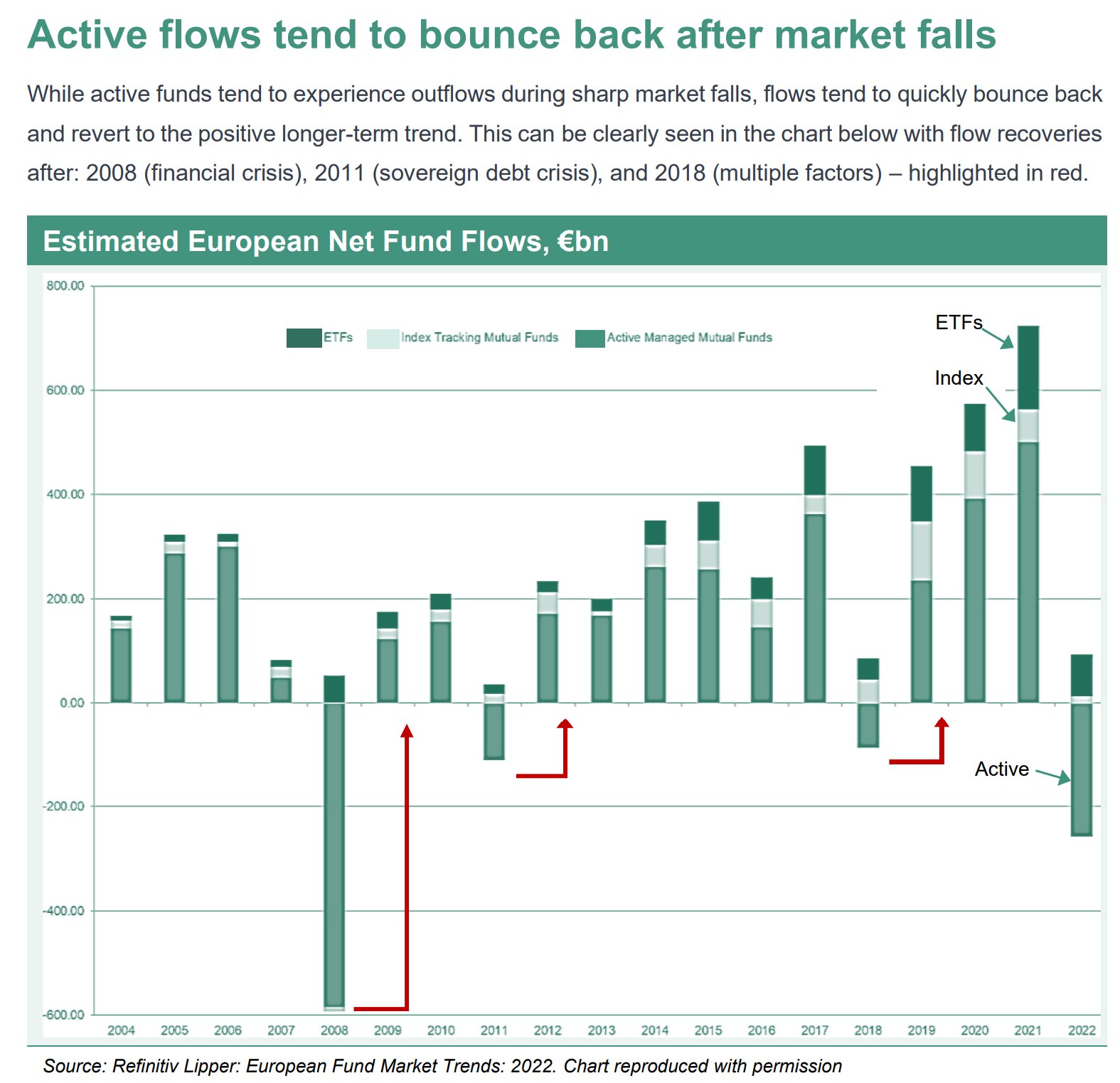

We simply don’t know when risk appetites will turn more positive, but history suggests that when they do, flows into active managers could ratchet up. I presented the historical evidence for this in one of my previous Equity Development research notes on Polar Capital (another UK-listed active manager), from which the chart below is extracted.

So that’s a potential ‘cyclical’ tailwind for Ninety One when overall market sentiment turns.

Prospects for Ninety One’s competitive positioning

This is the interesting piece of the Ninety One puzzle for investors. I think this is anything but a ‘me-too’ UK asset manager.

Building on its EM roots, it’s offering has evolved into an interesting menu of investment strategies for clients and it’s worth having a browse around its investment strategies website page (and looking at its track record versus benchmarks etc). But the recent results presentation highlighted four key potential growth areas:

Global and international equity

EM equity

EM fixed income (including specialist credit)

Sustainability and impact.

I think the overlap between EM investing (both equity and debt), and sustainability strategies is particularly interesting and a potential key differentiator for Ninety One. In Europe, we tend to look at sustainable investing as a fairly clear-cut space which often excludes anything with smokestacks and has a heavy emphasis on renewable energy, EV’s, waste reduction etc.

But when you start looking at emerging markets and the US, sustainable investing strategies are a more complicated affair, often because of energy security and cost concerns.

Coal-dependent South Africa is an obvious example of this with government displaying a healthy degree of skepticism over the potential of renewables, and especially over how quickly a transition to renewables could be rolled out. To get a flavour of how different the conversations are in South Africa (and in some other African countries) compared to the UK and Europe have a read of this article and this one with comments from the South African mineral resources and energy minister.

The difference in attitudes has also been highlighted by Ninety One research which found that only 29% of UK asset owners believed that climate-related investing leads to lower returns, but 44% did in North America and 52% in Southern Africa.

Addressing concerns over how the transition to renewables is managed is an area where Ninety One has been building up relevant internal capacity and knowledge in not-so-mainstream areas such as ‘transition finance’. It has a fascinating report on its website called A disorderly transition which explains this and highlights some of the investment opportunities. Here’s a teaser:

“Transition investments or transition finance is the burgeoning investment category that will support high-emitters in their efforts to reduce emissions. This is distinct from climate solution providers which offer the products and services that drive decarbonisation. This is not a free pass for investors to own high-emitting sectors. Instead, responsible investors must distinguish between companies that have a credible transition plan and those that can’t or will not change sufficiently. Investors need the assurance that these ‘transition investments’ have the capacity to reduce emissions in the long run… This is fertile ground for active managers seeking performance from companies who are facilitating the transition rather than perpetuating the problem, and where the market does not fully understand or price-in the transition potential.“

***

Hopefully the above provides some initial food for thought if you are going to look into adding Ninety One to your portfolio. But a lot of research is needed to decide if this is indeed a deep-value diamond or a 'structurally challenged mid-sized player'!

Make sure you keep up to date with all of my updates on the asset and wealth management sectors by subscribing:

Please read the Investing in the Investors disclaimer here.

Disclosure: At the time of writing, Paul Bryant was a shareholder in a number of the asset managers mentioned in this publication, and covered Impax Asset Management and Polar Capital as an analyst on behalf of Equity Development Limited. Read Equity Development’s research on Impax Asset Management here, and on Polar Capital here. (Please read this link for the terms and conditions of reading Equity Development’s research).