UK asset managers are about to report Q3 data. Here's a primer.

Q2 was a fascinating mix of resilience, potentially changing fortunes, and ongoing struggles. There's a few key trends and data points investors should look out for in Q3.

[Upfront, I need to apologise for not publishing a Q2 review sooner - I took the summer off from writing!].

A tough Q2

It was another tough quarter for asset managers as many investors remained nervous and parked their money in cash (more on that trend, and which companies benefit, in this newsletter in the next few days).

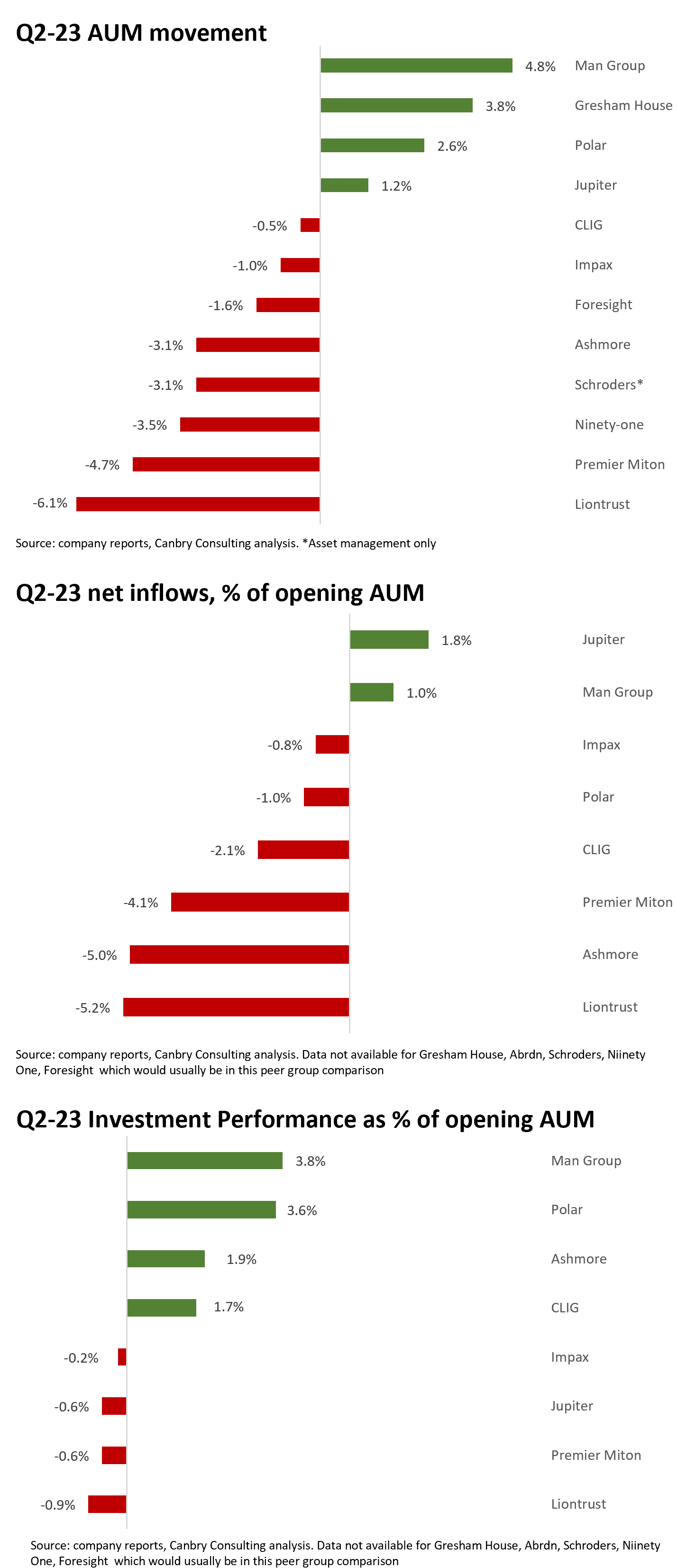

Net flows continued to be mostly negative with the median net flow rate of the peer group now negative in every quarter since Q4-21.

And while some had solid investment performances, three of the top four investment performances (which includes currency movements) were assisted by reporting AUM in dollars (MAN, Ashmore & CLIG). The other AM’s in this peer group report AUM in GBP, and suffered a currency headwind of around 2.0-2.5% on their dollar and euro denominated assets due to an appreciating pound.

But at a company level there are some fascinating insights. I’ve split my commentary on individual companies below into those demonstrating resilience, those looking like their fortunes are changing, and those that have ongoing struggles.

After that, I highlight another key trend to watch. The differing characteristics of retail versus institutional investors.

Resilience

Man Group (LON:EMG) had a good quarter recording positive flows and a strong investment performance. In fact, nine out of the last ten quarters have shown positive net flows.

Interestingly, in Q2, long-only strategies attracted net inflows (negative in Q1) whereas absolute return strategies’ (designed to make money in rising or falling markets) net flows turned negative following a positive Q1).

In Q3, I’ll be interested in seeing if any more obvious trends emerge in absolute return versus long-only flows (providing possible clues to the balance of power between investor caution and more bullish sentiment) .

Also worth noting is that the Q2 data above was part of half-year results, released on 1 August 2023, which saw the share price hammered with a big fall in performance fees (share price down around 12% from 31 Jul 23 to the time of writing).

Impax Asset Management (LON:IPX) - on an absolute basis the numbers don’t look great but on a relative basis not too bad at all.

ESG has been out of favour, so Impax's very small net outflow looks good compared to other AMs. And remember its net flows were positive during the worst of 2022, except for 1 quarter which saw a tiny outflow. In fact, it has recorded only two quarters of negative flows since 2015!

I think there’s a clear flight to quality happening in the ESG/sustainable investing space which should benefit Impax. I wrote about this in May in a research note covering Impax’s half-year results “Poised to thrive in ‘sustainable investing 2.0’ “.

This point is reinforced by Morningstar’s latest research “SFDR Article 8 and Article 9 Funds: Q2 2023 in Review” which highlights Article 8 funds (with ‘light’ sustainability credentials) leaking assets while Article 9 funds (with the highest sustainability credentials) continuing to attract assets.

There’s no doubt it’s challenging times in the ESG/sustainable investing space but over the medium to long term, I think Impax should thrive. And while its share price probably ran too far in the ESG euphoria of 2021, the price is now one-third of that level! It’s surely worth a second look?

Gresham House (LON:GHE) - looking strong once again but doesn't split flows and investment performance on a quarterly basis. Sadly, with Gresham House being acquired, it looks like we'll be losing this one from public markets soon.

Changing fortunes?

Polar Capital Holdings (LON:POLR) had a very strong investment performance in Q2, no doubt benefiting from the tech stock rally, but probably just as importantly, after heavy outflows in 2022, the net flow situation continued to improve.

As I wrote in a recent research note: ‘Investment returns mean that FY24 starts well’

“Polar reported continued demand and inflows into its Sustainable Emerging Market Stars, European ex-UK Income, Healthcare Blue Chip, Biotechnology, and Smart Energy Funds with combined net inflows of £313m. Importantly, with 38% of AUM in technology strategies, the rate of net outflows from open-ended technology funds continued to declinewith 38% of AUM in technology strategies, the rate of net outflows from open-ended technology funds continued to decline.”

The key indexes most appropriate to Polar’s AUM haven’t done a huge amount to date in Q3 (although healthcare and insurance indexes are positive) so I’m not expecting fireworks, but I will be watching Polar’s net flow commentary carefully. In particular, if investors start piling back into tech, this stock could be very interesting. It’s one to watch.

Jupiter Fund Management (LON:JUP). After a really torrid period the new strategy under new CEO Matthew Beesley is showing positive signs with a second quarter of positive flows out of last three. Institutional flows were strong while retail flows were weak (see additional comment below).

This is another fund manager whose share price is trading around one-third of 2021 levels. Another one to watch.

Ashmore (LON:ASHM). I'm torn between putting this one in the 'changing fortunes?' or 'ongoing struggles' category.

With an emerging market debt focus - which is looking much more positive as an asset class - Ashmore delivered a strong investment performance in Q2. But investors are still withdrawing funds.

The key question is when will inflows return? Surely flows must follow returns at some point? When they do, this is one AM which could benefit tremendously.

Ongoing struggles

Liontrust Asset Management (LON:LIO). Q2 was another quarter of heavy outflows (six in a row now).

Since the release of its Q2 trading update Liontrust has had its bid to acquire Swiss asset manager GAM rejected. The message from shareholders to management was loud and clear … that’s a good thing, focus on fixing the core business first! The share price jumped 11% in the three days following the bid rejection (but has drifted lower again since).

Liontrust is now less than one-quarter of its 2021 share price peak. Credibility needs to be re-built. It simply has to turn the net flow situation around. Fast.

Premier Miton (LON:PMI). No sign of a turnaround in net flows here with only one positive quarter of net flows in the last seven.

Ninety One (LON:N91). AUMs were down again so no obvious good news. I suspect this AM will also need to demonstrate a return to net inflows before much investor interest is stimulated.

But it is an interesting one. In May 2023, commenting on the annual results, I wrote about a potential ‘deep value’ investment case: Ninety One (asset management). Tough, tough year, but ... The byline was: “Year on year comparatives grim. Price down 7% on results day, 40% since Jan ‘22. A deep-value diamond or 'structurally challenged mid-sized player'?” Give it a read.

Institutional v retail differences continue

When we zoom out from individual company analysis the difference in behaviour between retail and institutional investors is becoming increasingly clear.

Asset managers with an institutional investor client base bias are definitely looking stronger when it comes to net flows. Man, Impax, and Polar are all institutional-channel dominated and have relatively strong flows.

And while Jupiter has a large retail investor client base its new strategy has an emphasis on the institutional channel - and this is where its positive flows are coming from.

Meanwhile, Liontrust and Premier Miton have a bigger emphasis on the retail investor channel and have struggled.

I’ll be commenting on the Q3 updates of UK asset managers in the first few weeks of October 2023. Make sure you keep up to date with these and all of my updates on the asset and wealth management sectors by subscribing:

Please read the Investing in the Investors disclaimer here.

Disclosure: At the time of writing, Paul Bryant was a shareholder in a number of the companies mentioned in this publication, and covered Impax Asset Management and Polar Capital as an analyst on behalf of Equity Development Limited. Read Equity Development’s research on Impax Asset Management here, and on Polar Capital here. (Please read this link for the terms and conditions of reading Equity Development’s research).