Wealth managers' Q3-23. What a mixed bag! (part 2)

Some flying high. Some steady-as-she-goes. Some riddled with uncertainty.

In part one of this two-part post I provided a comparison of wealth managers’, investment managers’ and platforms’ Q3-23 trading updates. The chart below provides a quick reminder of the most important “who did what” in the sector in Q3.

I discussed the two largest players, St James’s Place and Hargreaves Lansdown, in some detail in part one, so let’s dig into some of the others.

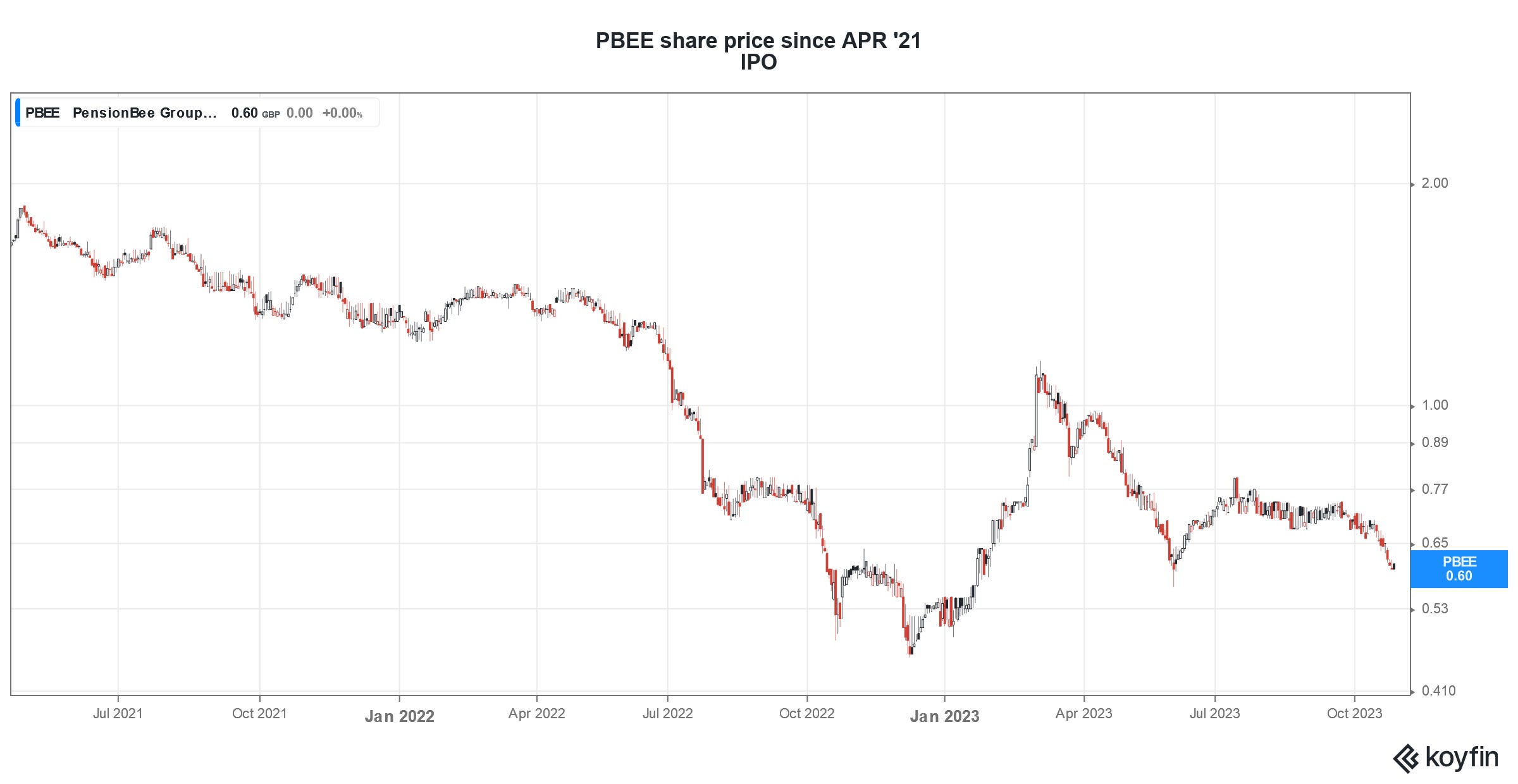

PensionBee on track with growth targets

The smallest company in our peer group, this direct-to-consumer (D2C), earlier-stage pensions provider continues to gain market share in its target space. Its AUA of £4bn is still dwarfed by incumbents Hargreaves Lansdown (£135bn) and AJ Bell (£76bn), but it is certainly makings inroads.

While PensionBee’s customer growth rate in percentage terms is unsurprisingly much higher than incumbents, what may be a surprise is that the absolute number of net new customers added has been mostly higher than AJ Bell’s D2C business in recent quarters and not far off that of Hargreaves Lansdown (PensionBee added more customers than HL in the most recent quarter).

It says it’s still on track to reach breakeven EBITDA in FY24 (on a monthly basis by end-FY23), a goal set at the time of its Apr 2021 IPO. That would be a remarkable achievement given the market headwinds it’s faced since the IPO.

But despite that, its share price has taken a hammering. Investors now need to decide if the fall has been over-done for this company which has so far delivered what it promised to.

Tatton flying high

Tatton doesn’t report quarterly, only half-yearly, so we have to look at this one over a six-month period. But whichever way you slice or dice it, this specialist model portfolio service (MPS) provider, servicing smaller financial advisers, continues to grow at a remarkable (and consistent) clip. It really has appeared to have carved out a lucrative sweet spot in the market.

Last week I published my Equity Development research note - Growth rate head-and-shoulders above peers (again) on this business, and the chart on page 1 of my note really says it all.

AUM grew 8% over the half-year to £13.7bn. Net inflows totalled £910m (7% of opening AUM), showing remarkable strength and consistency (H1-23: £907m, H2-23: £887m).

And Tatton’s growth leadership was not a one-off. It also had the highest net flow rate in the preceding 12-month period. Have a read of the full research note here.

And if you are looking into Tatton, I would also highly recommend listening to this Investors Chronicle podcast The Companies and Markets Show: The 2023 AIM special (Spotify link). Tatton is discussed between 2.00 and 11.00 minutes - performance, business model, competition, and valuation.

AJ Bell consistent strong performer

Another strong AUM growth performance in Q3 continues a period of AJ Bell consistently being one of the faster growing companies in this sector.

What investors should also remember about AJ Bell, and what distinguishes it quite substantially from Hargreaves Lansdown, is that its advised platform is actually larger than its D2C platform.

Measured by AUA it’s more than double the size of the D2C platform (£48bn v £22bn) but in terms of revenue its only slightly bigger (£50m in H1-FY23 vs £47m). By number of customers, it’s the other way around (317k D2C v 159k advised). The D2C channel is also growing faster.

So there is a fair amount of diversification across the two main client segments in this business, as shown in the table below (source: AJ Bell website).

Like HL, it has recently benefited from an elevated NIM on client cash, offset to a small degree by lower transactional fees in areas such as stocks and fund investments. So there is the future risk of revenue yield falling when interest rates fall.

But with good AUA growth momentum in difficult market conditions; revenue growth of 37% (H1-FY23 over H1-FY22); PBT growth of 61% (H1-FY23 over H1-FY22); and a PBT margin of 40% (H1-FY23), the business is looking in good shape. It does command a premium PE ratio compared to most in the sector, but this doesn’t look excessive. And it certainly looks worthy of a second look from investors.

Quilter - needs to deliver on growth

Over the last few years Quilter has been on an ‘efficiency journey’, which is ongoing and aims to boost its operating margin over the longer-term. It has a strong balance sheet and trades at a seemingly-low multiple, with some speculating that it might be an attractive takeover target.

That may be, but any substantial upside for investors will surely be dependent on Quilter improving its growth trajectory? Right now, it remains a growth laggard.

Rathbones - all about the Investec W&I acquisition

Like Quilter, Rathbones’ growth has lagged the sector recently.

But its profile has now totally changed with the recent acquisition of Investec Wealth & Investment, which kicked it up from around £60bn AUA to £100bn.

This combination really is an acid test of how true the ‘scale benefits’ argument is in the wealth management sector.

Encouragingly, the deal isn’t Investec ‘cashing out’ - according to the deal announcement:

Following completion, Investec Group will have an economic interest in Rathbones' enlarged share capital of 41.25% with Investec Group's voting rights limited to 29.9% of Rathbones' enlarged total voting rights. Existing Rathbones shareholders will have an economic interest of 58.75% and voting rights of 70.1%. The terms of the Combination imply an equity value of approximately £839 million for Investec W&I UK.

Here’s the logic, again according to the deal announcement:

the Boards of Rathbones and Investec Group believe that the Combination will:

enhance and enrich the client proposition across investment management, financial planning, fund management and banking services;

create a leading multi-channel distribution capability across private clients, intermediaries and charities, through an expanded network in 23 locations across the UK and Channel Islands;

attract and retain the best industry talent through a leading employee proposition;

leverage Rathbones' investment in technology and operating model to deliver an optimal client experience whilst improving operating efficiency across the larger combined business;

deliver significant value creation through the strong fit between the two operating models, with target annual run-rate cash synergies of at least £60 million, driven primarily by cost savings as well as higher net interest income;

generate attractive financial returns for Rathbones: (i) expected to be accretive to underlying EPS in the first full year following completion; (ii) targeting low-teens underlying EPS accretion in the third full year following completion; and (iii) targeting double-digit post-tax return on invested capital in the third full year following completion;

support the Enlarged Rathbones Group in maintaining a resilient capital position through all-share consideration with earnings accretion underpinning its progressive dividend policy; and

establish a long-term strategic partnership between Rathbones and Investec Group to leverage attractive collaboration opportunities.

It’s got all the right buzzwords. Time will tell if management can deliver on this.

Brooks Macdonald

I published my Equity Development research note on 12th October covering Brooks Macdonald’s Q3 FUM update.

“FUM increased marginally from £16.85bn on 30 Jun 23 to £16.86bn on 30 Sep 23. As flagged in the FY23 results release of 14th Sep 23, net flows were slightly negative for the quarter at -£70m, although BM has indicated it expects positive flows for the whole of FY24.

It’s important to keep this small negative quarterly net flow number in context: it follows nine consecutive quarters of positive flows (achieved despite difficult market conditions) and a period where BM recorded a higher organic growth rate than peers for 6 out of 8 quarters.”

You can read more details in the full note at this link: Well-flagged sluggish quarter but price fall looks over-done.

The note goes into some detail of how wealth/investment managers’ share prices have been battered over the last 18 months or so, and in my view, are looking undervalued. Extract from note here:

And I highlight that large foreign wealth managers were already seeing substantial value in UK acquisitions when prices were a lot higher. When the acquisition of Brewin Dolphin by RBC was announced on 31 March 2022, its PER jumped from 16.9 to 27.2, a premium of 62% to its share price the day before the deal was announced.

“They are surely seeing even more value now”

Then bizarrely, on 13th October, Reuters ran this article: “Brooks Macdonald lines up defence adviser amid takeover interest, sources say”.

The price jumped over 6% on that day.

Interesting times in the wealth management space. Be sure to subscribe to this newsletter to keep up to date with the latest results in the asset and wealth management sectors.

Please read the Investing in the Investors disclaimer here.

Disclosure: At the time of writing, Paul Bryant was a shareholder in a number of companies discussed in this post, and covered Tatton Asset Management, Brooks Macdonald, Mattioli Woods, and PensionBee as an analyst on behalf of Equity Development Limited. Read Equity Development’s research on Tatton here, Brooks Macdonald here, Mattioli Woods here, and PensionBee here (Please read this link for the terms and conditions of reading Equity Development’s research).