Asset managers' clients not looking so smart

UK-listed asset managers delivered strong returns in Q4-23 (they have been for well over a year now). But clients are still pulling money out. Flows surely follow strong returns? But when?

This is not investment advice. Please read TheInvestors.blog disclaimer here.

Asset managers had a good Q4 of 2023, with most recording solid AUM growth.

The growth story was however all about market movements and investment returns, with most major indexes sharply up (MSCI AWCI: +11.2%; S&P 500: +11.2%; NASDAQ: +13.6%; FTSE 100: +1.7%).

[Note that returns for the first three indexes above are show in US$ terms, and those UK asset managers reporting AUM in GBP (all except CLIG & Ashmore in the above chart) would have had a currency headwind on their USD holdings of around 4% in Q4 23 as the GBP/USD rate moved from 1.22 to 1.27 over the quarter.]

Meanwhile, investors remained nervous and continued to withdraw money from asset managers.

The net withdrawal of funds from most of these asset managers has been going on for two years now, starting in early 2022 (the middle section of the bottom chart in the graphic below) when markets started to tank (the middle section of the top chart in the graphic below).

We don’t know exactly where most of that capital has gone, but it has been widely mooted by asset managers that most of the outflows are asset allocation decisions out of equities and into cash or fixed income assets.

If that is the case, then the timing of recent withdrawals by asset managers’ clients isn’t looking like such a smart decision. They’ve been pulling funds and missed a strong rally. In the top chart below, look at the plethora of green bars to the right of the chart (since Q4 22) indicating mostly positive (and very strong) investment returns (with the exception of Q3 23). And then contrast that to the plethora of red bars in the bottom chart over the same period, indicating quite strong net outflows, and hardly different from the carnage of 2022. There’s a massive mismatch.

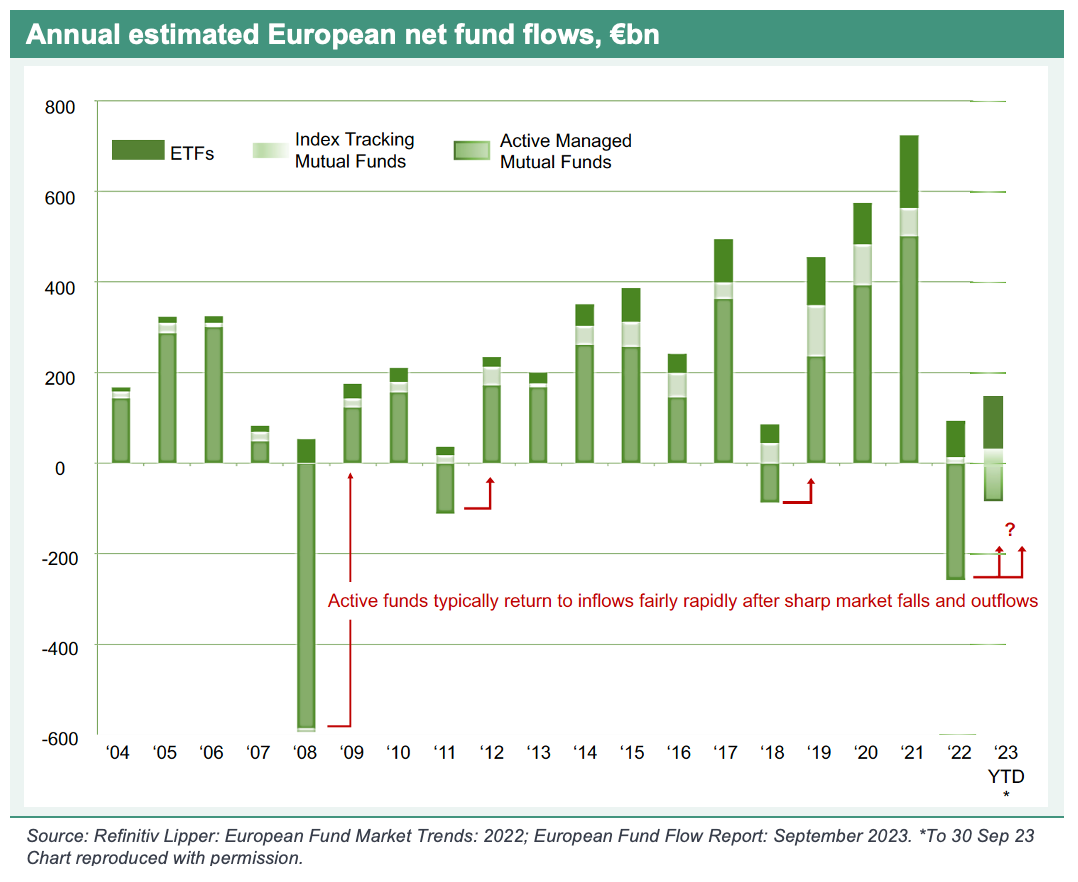

History suggests this mismatch doesn’t last for that long. In recent months, I have used the chart below in a few of my Equity Development research notes to highlight the historical trend that after market falls, flows into active funds tend to quickly bounce back and revert to their positive longer-term trend. These active net flow recoveries can be clearly seen after 2008 (financial crisis), 2011 (sovereign debt crisis), and 2018 (multiple factors) – highlighted in red.

That bounce back into active funds hasn’t happened yet after the 2022 market falls, and appears to be taking longer than usual. Investors seem to be showing more caution than after previous market falls. Perhaps that’s understandable given the enormity of geopolitical uncertainty we face, as well as the uncertainty around inflation and interest rates. But so far, that caution has cost them money.

If markets and asset managers continue to produce good returns, the turnaround in flows is surely just a matter of when, not if? The potential pothole is if markets sink again. That’s not going to help flows.

I am (cautiously) leaning towards an improved net flow situation showing its face soon. And I think Polar Capital CEO Gavin Rochussen provided a sensible outlook in its recent AUM update:

“Despite global equity markets rallying in the final quarter (of 2023), the ‘risk-off’ stance by investors resulted in net outflows in the quarter … (but) with peak interest rates in sight and declining inflation rates, investors will, we believe, begin to seek additional exposure to equities.”

Let’s see.

I will shortly be publishing reviews of individual asset managers’ and wealth managers’ performances for Q4 of 2023 (not all results are in so I am waiting for the last few to be released). So be sure to subscribe to get notified when those posts drop. All posts are freely available so just choose the free option on the subscribe page to receive everything.

And if you do think TheInvestors.blog is worth telling others about and sharing, I’d me most grateful if you do.

This is not investment advice. Please read TheInvestors.blog disclaimer here.

Disclosure: At the time of writing, Paul Bryant was a shareholder in a number of the companies mentioned in this publication, and covered Impax Asset Management and Polar Capital as an analyst on behalf of Equity Development Limited. Read Equity Development’s research on Impax Asset Management here, and on Polar Capital here. (Please read this link for the terms and conditions of reading Equity Development’s research).