If you grasp Asset Managers' Q1...

...then congratulations, because what a mixed bag of a quarter it was! Share price moves ranged from +45% to -30% and fundamentals were all over the place too.

TheInvestors.blog is not investment advice. Please read the disclaimer here.

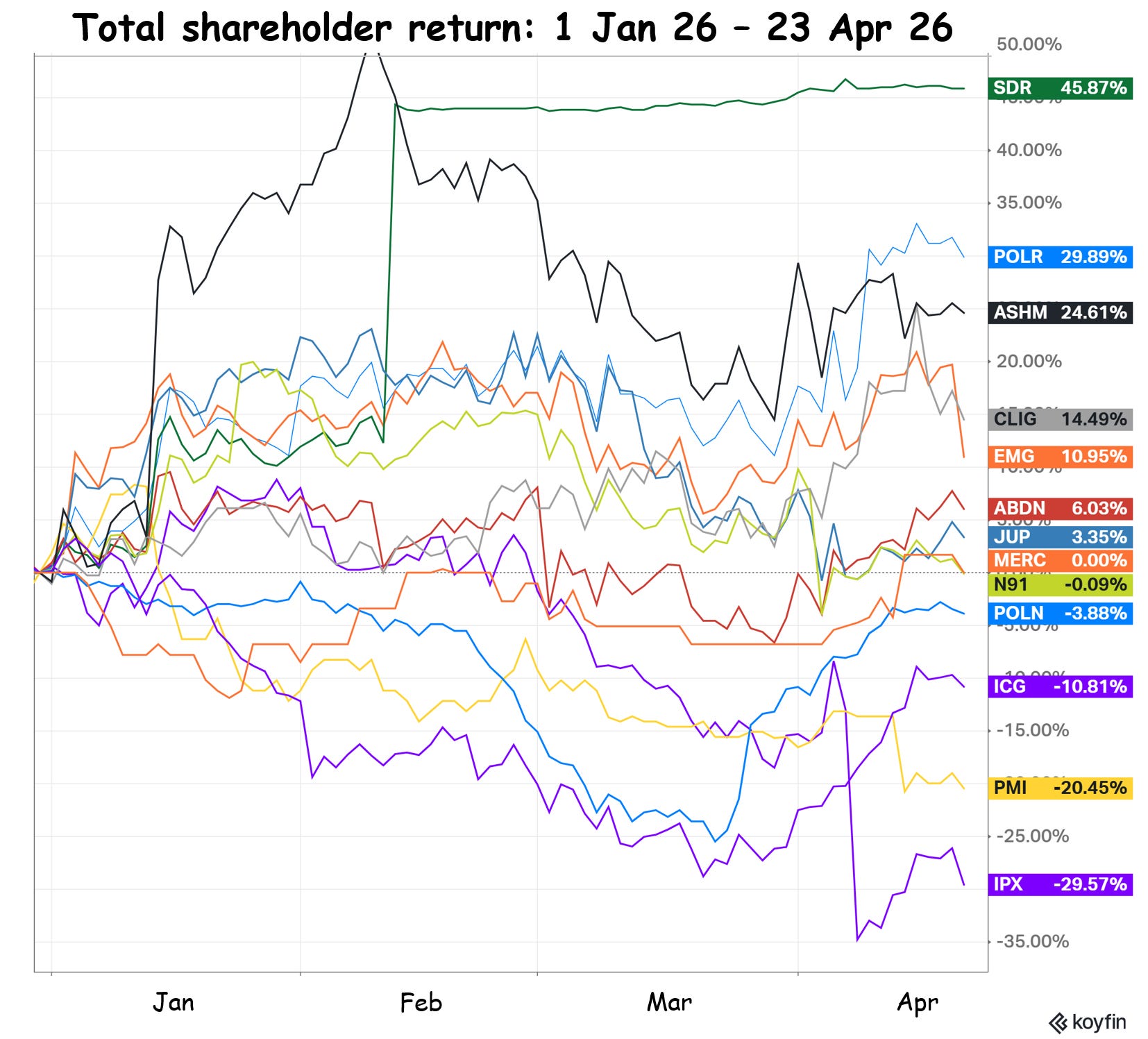

The year-to-date share price chart shows just how wild the ride has been for the UK-listed asset management sector in 2026.

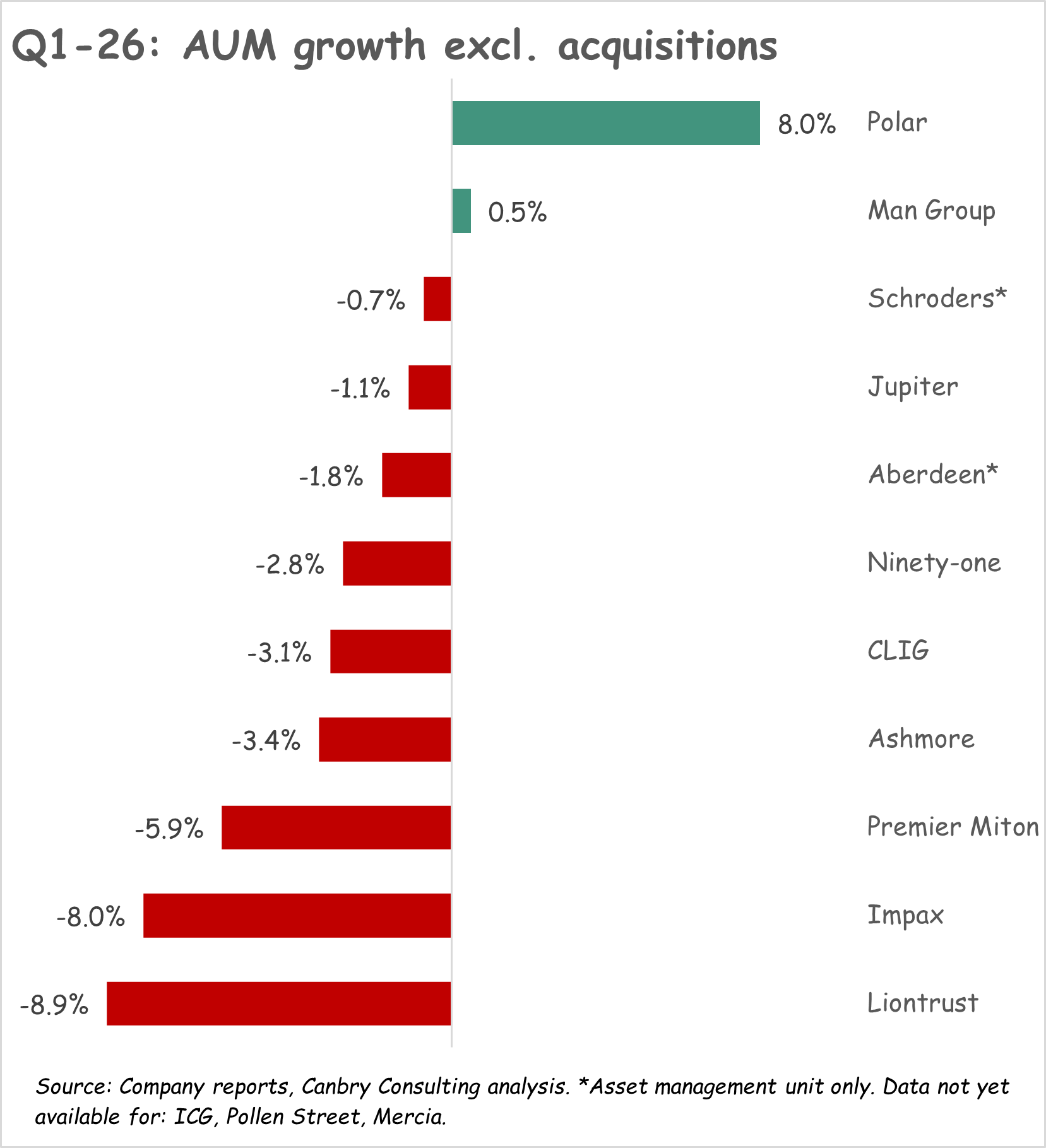

AUM growth during Q1 was mostly negative, with many managers reporting that January and February were stronger months, but the escalating conflict in Iran made for a much weaker March.

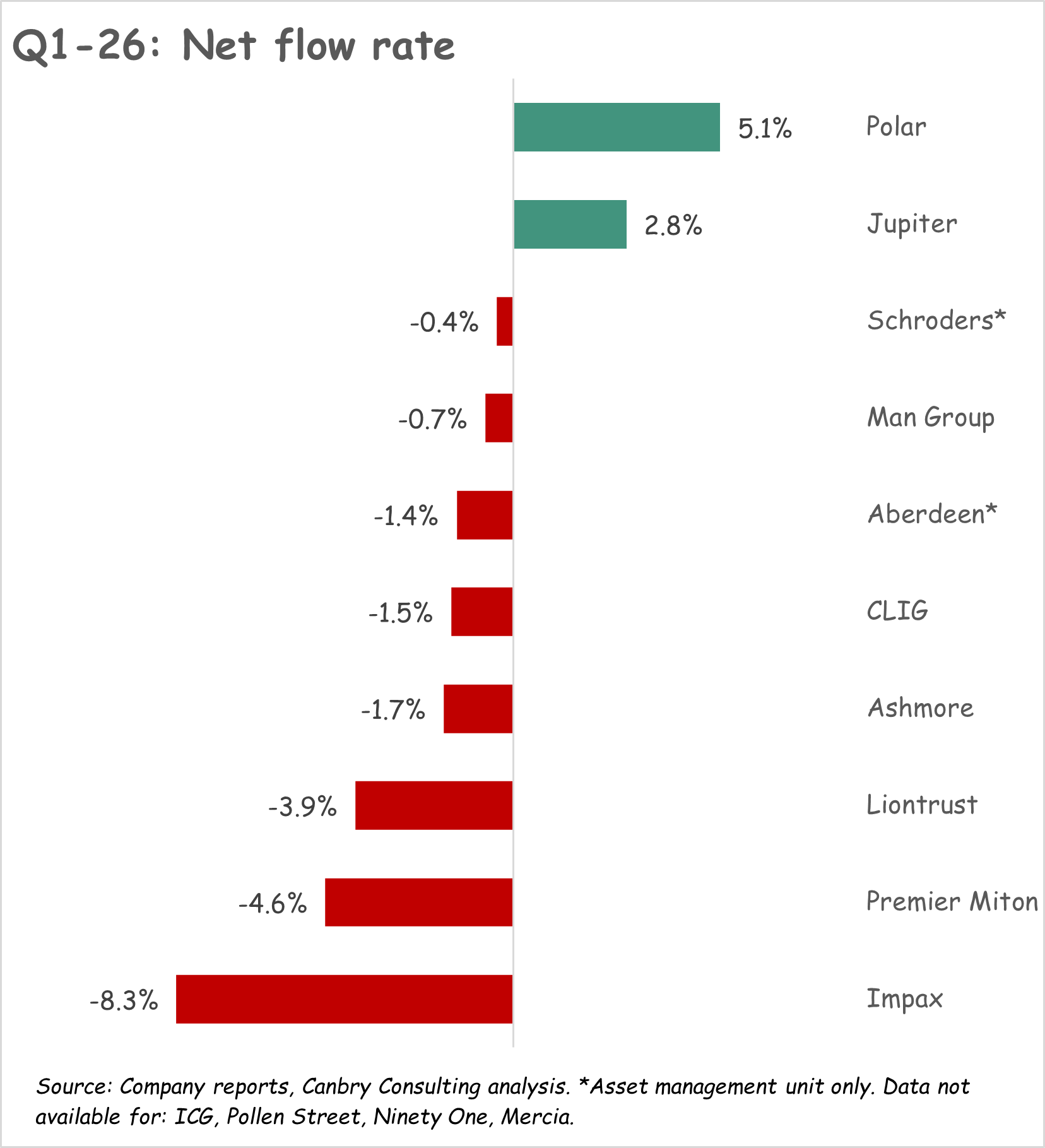

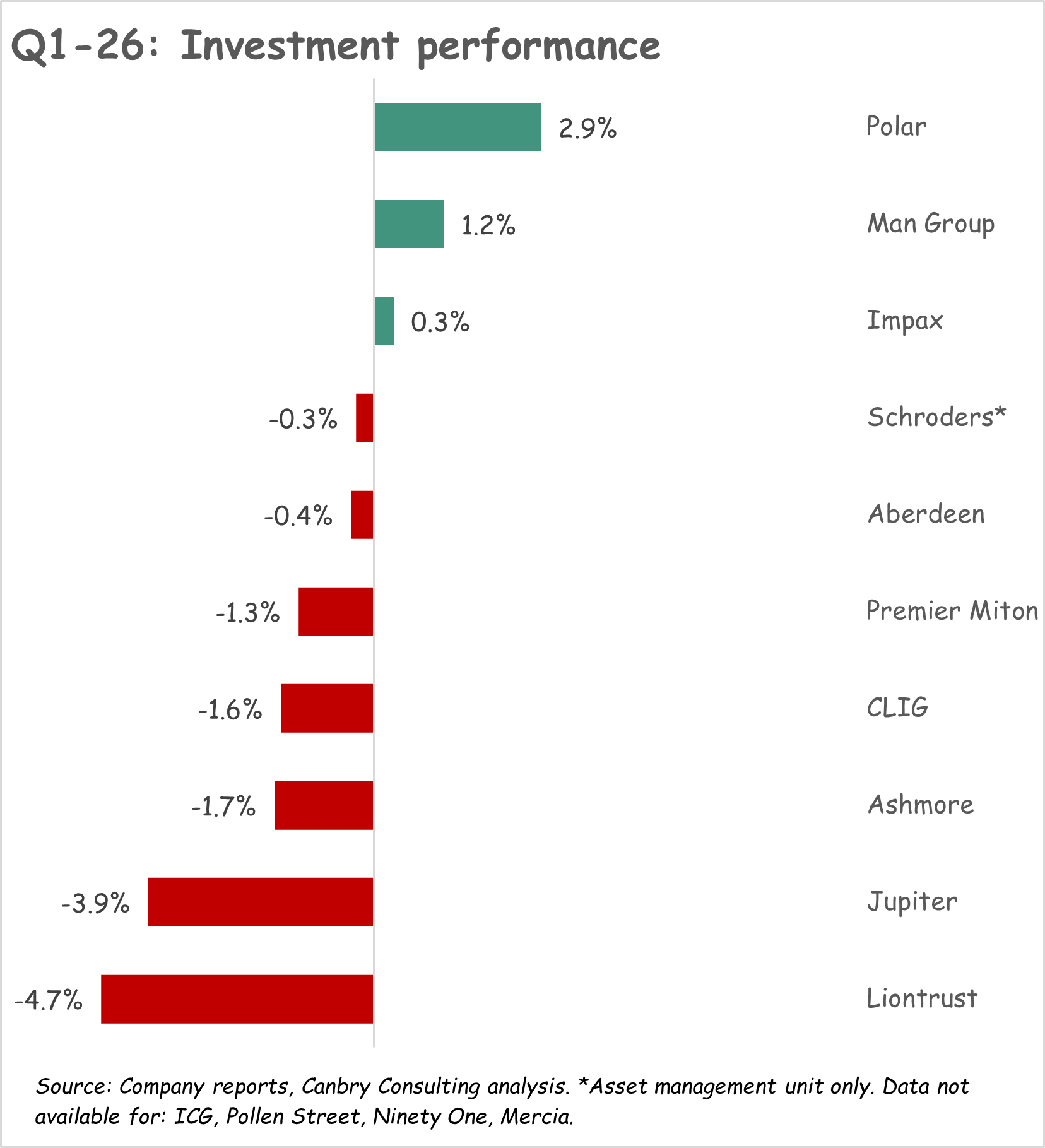

At a company level, here are some key points (net flow and investment performance charts are shown below these bullets):

Polar Capital: Knocked it out of the park. Huge jump in net flows to £1.4bn and very strong investment performance. Share price up c. 10% since Q1 AUM update. Its Global Technology and Artificial Intelligence funds were key contributors to flows and investment performance. But these are not index-hugging funds. The Global Technology fund returned +6.9% net in Q1 versus -7.5% for the benchmark Dow Jones Global Technology Net Total Return Index. The AI fund returned +11.1% versus -3.2% for the benchmark MSCI ACWI TR Index.

Man Group: Strong investment performance (driven by its alternatives portfolio) but net flows turned negative (-$1.6bn) after 5 successive quarters of positive net flows. There was a redemption of $6.1bn from a single client during the quarter. So outside of that, flows look good. The market didn’t like the update though, shares fell 7% on the day.

Schroders: Share price jumped on the announcement of a takeover by US-headquartered Nuveen (c. 30% premium to the share price on the day before the announcement). Quarterly performance was pretty good compared to others.

Jupiter: Very strong net flows. Four quarters of positive net flows now. Very poor investment performance hit AUM though. Completed CCLA acquisition which added £15bn of AUM (total now £68.4bn).

Ninety One: Middle-of-the-pack organic performance but Sanlam deal added £16.5bn of AUM (total now £172bn).

Ashmore: Weak quarter. Net flows turned negative again after a very strong Q4-25. Investment performance was negative too. The share price had strong momentum until mid-Feb but has since fallen c. 20%. All eyes are on the investor rotation in emerging markets - and if this has stalled?

Premier Miton: Heavy outflows and weak investment performance. With AUM down to £9bn, lack of scale is a real issue now. Cost cutting exercise announced. Share price down 8% on the day of the update.

Impax: Heavy outflows in the quarter but one of only 3 asset managers to record a positive investment performance. Downgraded revenue expectations. The share price fell 25% on the announcement. Impax says investment performance has improved substantially, especially for its thematic strategies. During the quarter, 63% of AUM outperformed. And it’s hard to argue with the company statement: “Longer term, the fundamentals that underpin our investment thesis continue to strengthen, particularly in the areas of renewable energy and energy efficiency, key components of energy security, which is already a priority globally in light of the currently elevated geopolitical tension.” But its all about turning net flows around.

Liontrust: Heavy outflows persist although not quite as bad as the last few quarters. Very weak investment performance. Announced 2 institutional mandate wins totalling £500m (not yet in AUM number). This is also all about turning net flows around.

Mercia: While it doesn’t report full AUM details quarterly, private markets specialist Mercia Asset Management had a strong final quarter of its FY26 (ending 31 March). This from my recent Equity Development research note. “Mercia has announced it expects EBITDA to be materially above expectations... Fundraising in H2 was strong, with Q4 alone seeing £200m of new funds raised (from successful VCT and EIS raises) or proposed increases to existing mandates (both quantum and duration). Impressively, there were no redemptions in FY26.”

Here’s the comparison of net flows.

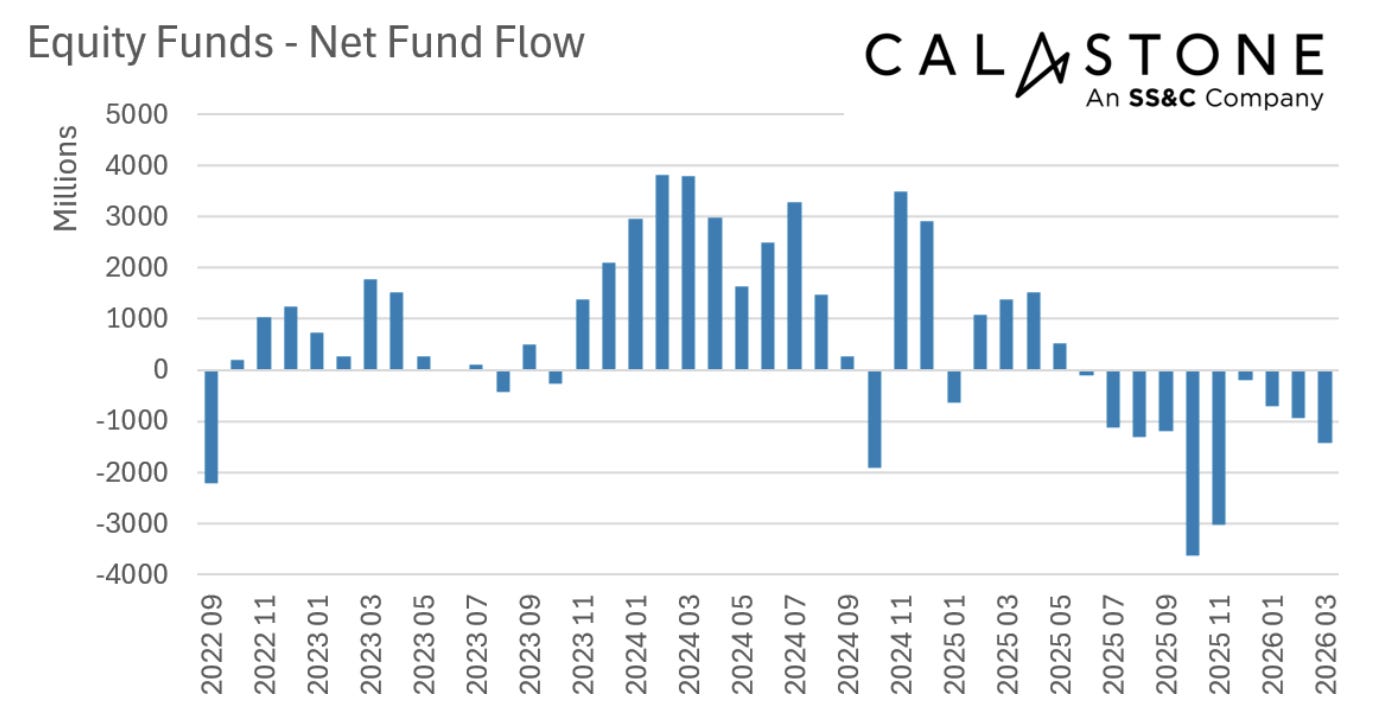

The above should also be read in the context of the net flow environment more generally, which saw UK funds suffer heavy outflows during Q1 (after a much improved Dec-25).

[Calastone measures orders from UK-based investors into funds domiciled in the UK. Note that this has nothing to do with where the underlying assets are invested].

And here is the investment performance comparison. [MSCI ACWI (GBP): -1.27%].

Subscribe to TheInvestors.blog below to keep up to date with the UK asset and wealth management sectors.

And if you think TheInvestors.blog is worth telling others about and sharing, I’d be most grateful if you do.

Disclosure: At the time of writing, Paul Bryant was a shareholder in a number of the companies mentioned in this publication, and covered Impax Asset Management, Polar Capital, and Mercia Asset Management, as an analyst on behalf of Equity Development Limited. Read Equity Development’s research on these companies by clicking on each. And please read this link for the terms and conditions of reading Equity Development’s research.