Is that a chink of light?

A look back at UK-listed asset managers' H1-25 & a look forward to H2 and beyond. Part 1: The (confusing) AUM picture.

TheInvestors.blog is not investment advice. Please read the disclaimer here.

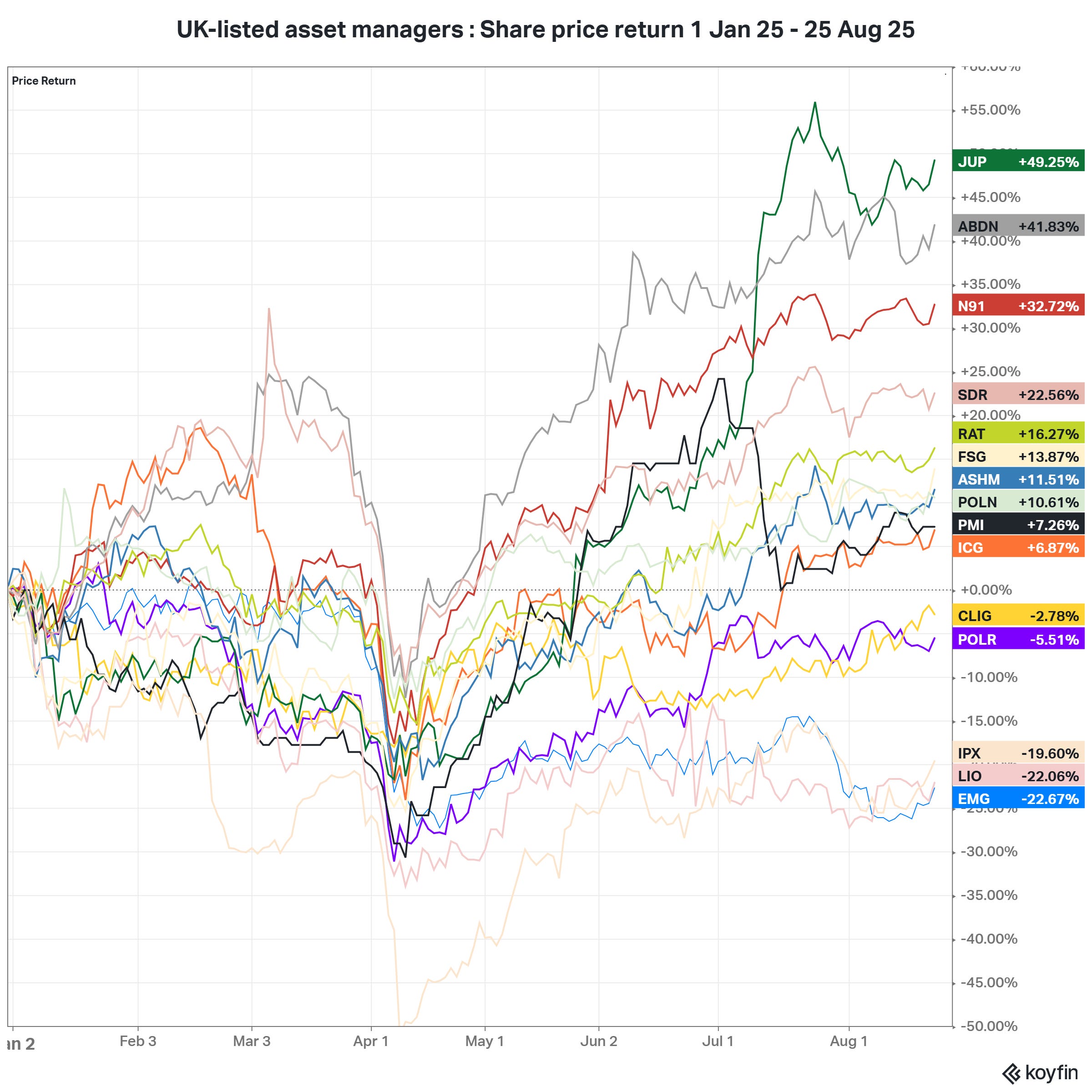

Share prices of UK-listed asset managers have mostly enjoyed a pretty good 2025 to date, with some strong recoveries since the early-April ‘liberation-day’ market falls.

There are some obvious stories. On the positive side, Jupiter’s announcement of its acquisition of CCLA Investment Management on 10 July 2025 was particularly well received, and that was on top of an already-decent recovery. Underperformers were Impax (hit hard by the loss of one particularly large mandate), and Liontrust (with persistently heavy outflows).

Some moves are less obvious, confusing even. Aberdeen’s sharp rise is not that easy to explain (surely it can’t just be that the ‘Abrdn’ era is ending?). And in the case of Man Group (ticker EMG in the chart above), it’s hard to pin down a specific reason for its heavy share price fall, especially given its AUM growth, and crucially its net flows, have been strong compared to others (see below).

So, as we approach Q3 updates, I take a look at UK-listed asset managers' fortunes in H1-25, and the outlook for H2 and beyond. This post (part 1 of 2), looks at AUM - the crucially important ‘top-line’ for asset managers. In part 2, I’ll be digging below the AUM line and look at the impact of strategic changes, cost cutting measures, acquisitions, and management changes, and how they might be affecting share price

Hidden forces in top-line AUM numbers

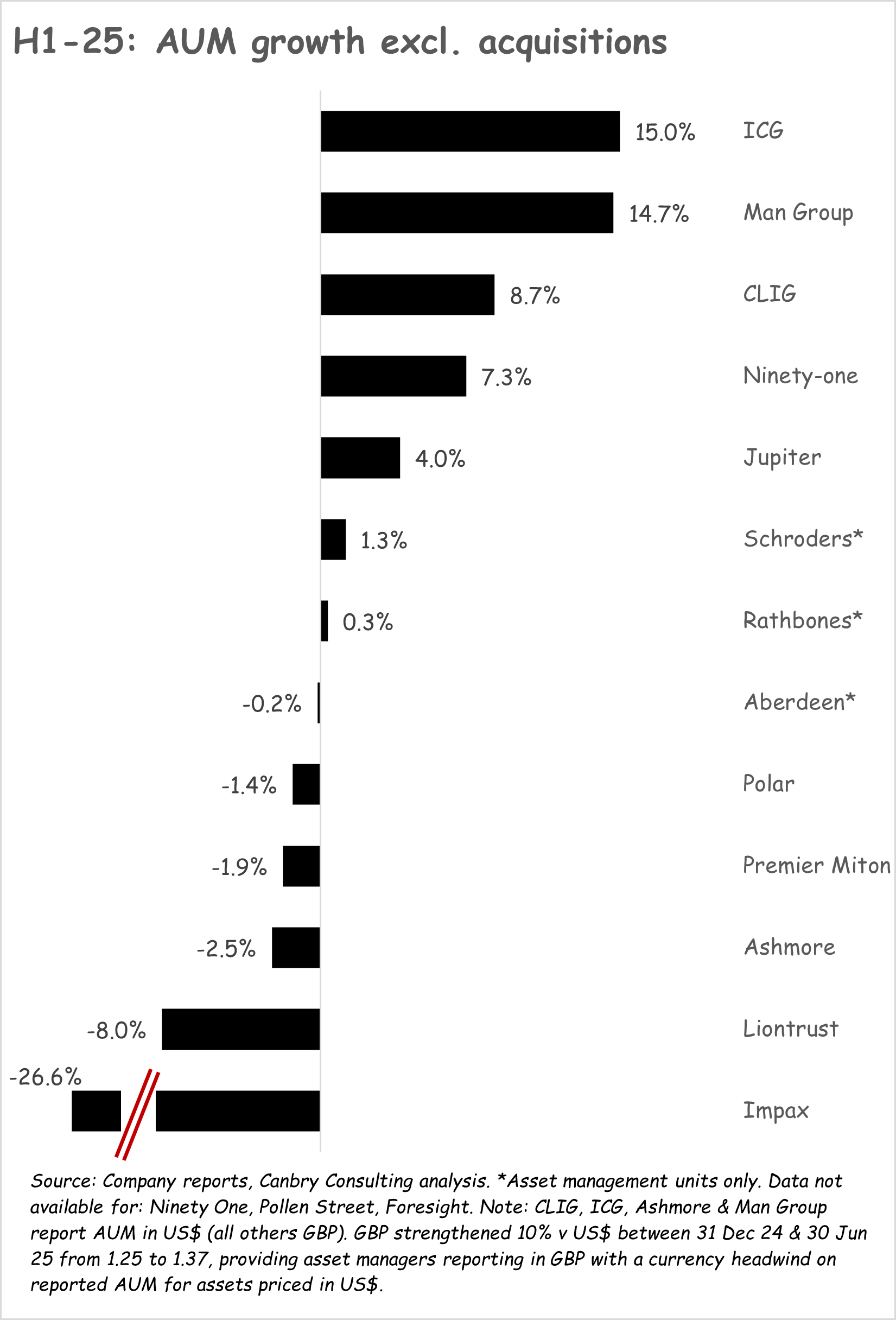

At first glance, it looks like there are a few clear growth-leaders and laggards when it comes to AUM, and a fairly large group ‘in the peloton’. But AUM comparisons in H1 are distorted in some cases because of currency moves.

ICG, Man, CLIG (City of London Investment Group), and Ashmore report AUM in US$. The others shown in the chart below report in GBP. And over H1-25, the GBP strengthened 10% v the US$ from 1.25 to 1.37. This means those reporting in GBP had a currency headwind on that part of their AUM priced in US$ [US$1m of AUM on 1 Jan 25 = £800k; that same US$1m of AUM on 30 Jun 25 = £730k]. So, it’s a little generous to label ICG, Man, and CLIG as the AUM ‘growth-leaders’ in H1.

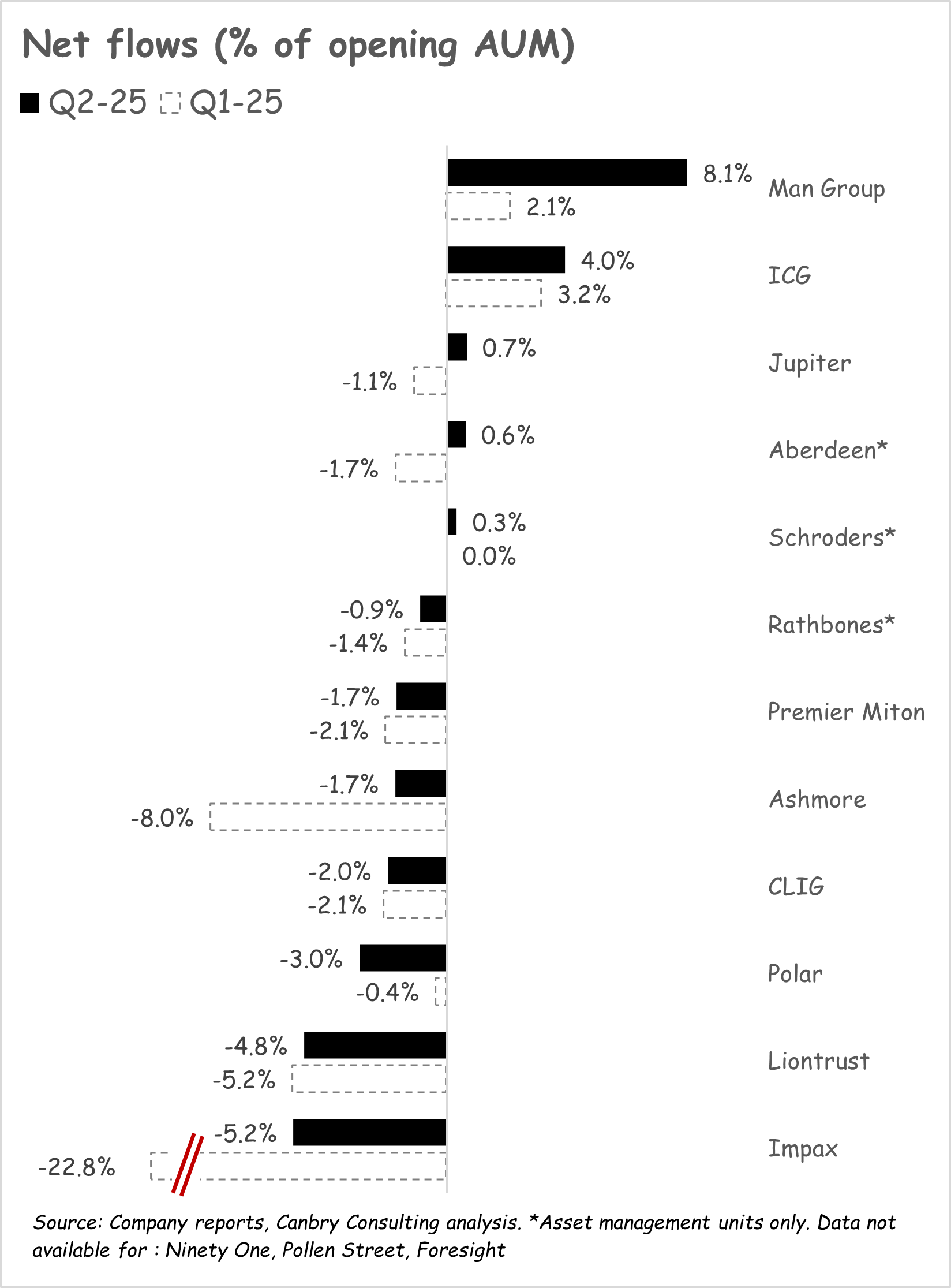

To better understand the AUM picture, it’s helpful to separate the impact of net flows (one of the most important metrics for asset managers - their ability to attract and retain AUM from clients) versus investment performance, and also to look at Q1 and Q2 separately.

Net flows looking (a little) more positive

Generally, it’s been a tough H1-25 for flows, with the obvious exceptions of Man Group (making its heavy share price fall seem a little strange, as clients are clearly backing it - but more on that in part 2), and ICG (the private markets specialist which has conducted a number of successful fundraisings, and also benefits from client assets being ‘locked-in’ to a greater degree than funds which invest in publicly-listed securities).

But on the whole, it’s an improving picture, with all except one of our peer group reporting an improved net flow position in Q2 compared to Q1. And even some of those asset managers with negative net flows reported tentative positivity in Q2 and into July (see commentaries below).

Company specific points worth highlighting include:

Man Group: The positive flows in both Q1 and Q2 were driven by long-only strategies (around 50% of AUM), with alternative strategies (absolute return, total return and multi-manager) experiencing negative net flows. The CEO’s review stated:

Total net inflows were $17.6 billion for the period, our strongest six months on record, 11.5% ahead of the industry. A particular highlight was a $13.2 billion subscription from a single client in systematic long-only, reflecting our ability to provide customised, quant-driven solutions at scale. Our continued market share growth during the first half of 2025 validates our position as a trusted partner serving our clients' evolving needs. Although alternative strategies have experienced headwinds recently, client engagement and dialogue on defensive alpha remain strong as we enter the second half of the year, reinforcing the fundamental importance of differentiated liquid solutions in the current environment.

ICG: Demand is clearly still strong for this private markets specialist. Its trading statement for calendar-Q2-25 stated:

Investment landscape remains very attractive for a number of strategies, including structured capital, secondaries and real assets equity.

Ninety One: Quarterly net flow data is not reported (only half-yearly with the latest data to 31 Mar 25). But commentary for the year ending 31 Mar 25 suggests a more positive net flow environment.

This was a year of two halves. The second half of the year (Oct 24 - Mar 25) reflected a turnaround with net inflows of £0.4 billion, our first positive net flow half-year in two years. This followed a tough first half, to end on net outflows of £4.9 billion for the full year. This is an improvement from the prior year’s net outflows of £9.4 billion… Overall, client activity improved steadily throughout the year. The inflection in flows mid-year supports our belief that clients are beginning to re-risk selectively and that demand is returning for differentiated active strategies.

Jupiter: After a prolonged period of net outflows, a welcome return to positive flows was reported in Q2 (and into July). Interim results commentary (on 25 July) stated:

Although we still saw small outflows for the first half, we generated net positive flows in the second quarter. Momentum in the institutional channel is strong and we have seen a month-by-month improvement in retail demand over the time period. We have generated net positive flows so far in July.

Aberdeen: A mixed bag for its investments unit with no clear trends visible (yet?). Investments makes up around 70% of AUM (this commentary does not refer to its adviser unit and interactive investor) Interim results stated:

…net outflows of £4.1bn (H1 2024: £1.0bn outflow), including the previously announced redemption of a low margin mandate… Excluding this previously announced redemption, Institutional & Retail Wealth delivered a net inflow of £4.4bn (H1 2024: £0.4bn inflow), reflecting significant mandate wins in quantitative strategies and fixed income partially offset by equities and liquidity outflows.

Schroders: Also a mixed bag for its asset management unit (c. 80% of AUM). Key messages from the interim results commentary: included:

Public Markets business saw small net outflows of £0.5 billion in the first half of the year. Within this, equities saw positive net flows of £3.5 billion (H1 2024: net outflows of £7.8 billion)… Fixed income saw net outflows of £2.0 billion (H1 2024: net inflows of £1.6 billion)… Multi-asset saw net outflows of £3.6 billion (H1 2024: net outflows of £3.4 billion)… Schroders Capital generated gross fundraising of £6.0 billion (H1 2024: £5.2 billion), with particularly strong contributions from the private equity and private debt and credit alternatives pillars… Schroders Capital NNB was £2.3 billion (H1 2024: £3.0 billion).

Rathbones: Net flows were weak but improving for its asset management unit which makes up around 15% of AUM. The interim results stated:

Single strategy funds have continued to perform well. Net outflows in the second quarter reduced to £0.2 billion (Q1 2025: £0.3 billion), supported by resilient gross inflows and a notable reduction in gross outflows, particularly from our Global Opportunities Fund. Flows into our multi-asset fund range were broadly flat in the quarter

Premier Miton: Another case of weak but improving flows. Its calendar-Q2-25 quarterly update stated:

There were encouraging signs of progress during the Quarter despite reporting a net outflow overall. Demand for our absolute return and fixed income funds remained good… Notably, net outflows from our UK equity funds reduced by over 50% compared to the average of the previous four quarters, reflecting improving investor sentiment and solid fund performance… Shortly after the Period end, on 7 July 2025, we successfully onboarded a new institutional absolute return mandate seeded with $50 million. In parallel, we are advancing discussions on an additional institutional mandate, which we are seeking to finalise before year-end.

Ashmore: It’s been an awful period for this EM fixed income specialist. You have to go back to 2021 to find a quarter with positive net flows. But Q2 was a huge improvement on Q1. Its latest quarterly trading update stated:

Net flows improved from the prior quarter with significantly lower redemptions... Overall, net flows were positive in equities, flat in external debt and alternatives, and there were net outflows in the blended debt, local currency and corporate debt themes… investors are beginning to rebalance portfolios away from heavily overweight US positions towards more attractively valued asset classes, including those in EM. While recent EM mutual fund inflows have been concentrated in exchange traded funds, previously this has been a precursor to broader institutional behaviour.

CLIG: Smallish net outflows have persisted for over a year now. Its trading update for the FY to 30 Jun 25 stated:

Net outflows were weighted more heavily to the first half of the financial year (Jun 24 - Dec 24) when macroeconomic uncertainty rattled markets. The second half withdrawals (Jan 25 - Jun 25) were characterised by some profit-taking after very strong performance by our investment teams. This was particularly true in the International Equity and Emerging Markets strategies.

Polar: A disappointing calendar Q2 of 2025 followed a strong run of net flows compared to other asset managers (see my research note of 30 Jun 25 for details of this). Flows were negatively impacted by outflows from its Technology Fund, the closure of an institutional mandate managed by the Healthcare team, and an asset allocation change by a single Emerging Markets Stars client, with Polar noting the new business pipeline for the Emerging Markets and Asia team remains strong. But many funds attracted net inflows. The AUM update covering calendar Q2-25 stated:

There has been continued demand for a broad range of our funds during the quarter. Those in net inflow include the Artificial Intelligence, Asian Stars, Financial Credit, Global Insurance, North American, Japan Value, European Income, Global Absolute Return and International Small Company funds.

Liontrust: Significant and persistent net outflows continued in calendar-H1-25, with its UK retail funds and MPS hard-hit. Management maintain a positive outlook, but that’s yet to be seen in net flows. It’s latest quarterly update stated:

Liontrust has spoken for the last nine months about how investors will need to search wider for alpha going forward and why this means a more positive environment for active management. We have now begun to see investors, led by institutional clients, turn more towards actively managed funds and diversify geographically, with Europe and the UK outperforming the US stock market over the first half of 2025.

Impax: This sustainable investment specialist is now looking for a return to stability following the loss of a very large St James’s Place mandate In calendar-Q1 of 2025 (see my research note covering its results for the half-year to 31 Mar 25 for full details of this). Flows in the quarter to 30 June were much improved, but still negative, and positive in the month of June. Impax’s latest quarterly update states:

The majority of our AUM follows investment strategies that have outperformed their generic benchmarks this calendar year, and in our larger listed equities business, there was a significant reduction in net outflows compared to the previous two quarters, with positive flows in June, reflecting strong institutional client commitments and fresh momentum in our wholesale channels in Europe.

So, a real mixed bag for flows in the sector, but probably fair to say that the outlook is improving, albeit with a degree of caution. Now let’s look at the impact of investment returns on AUM.

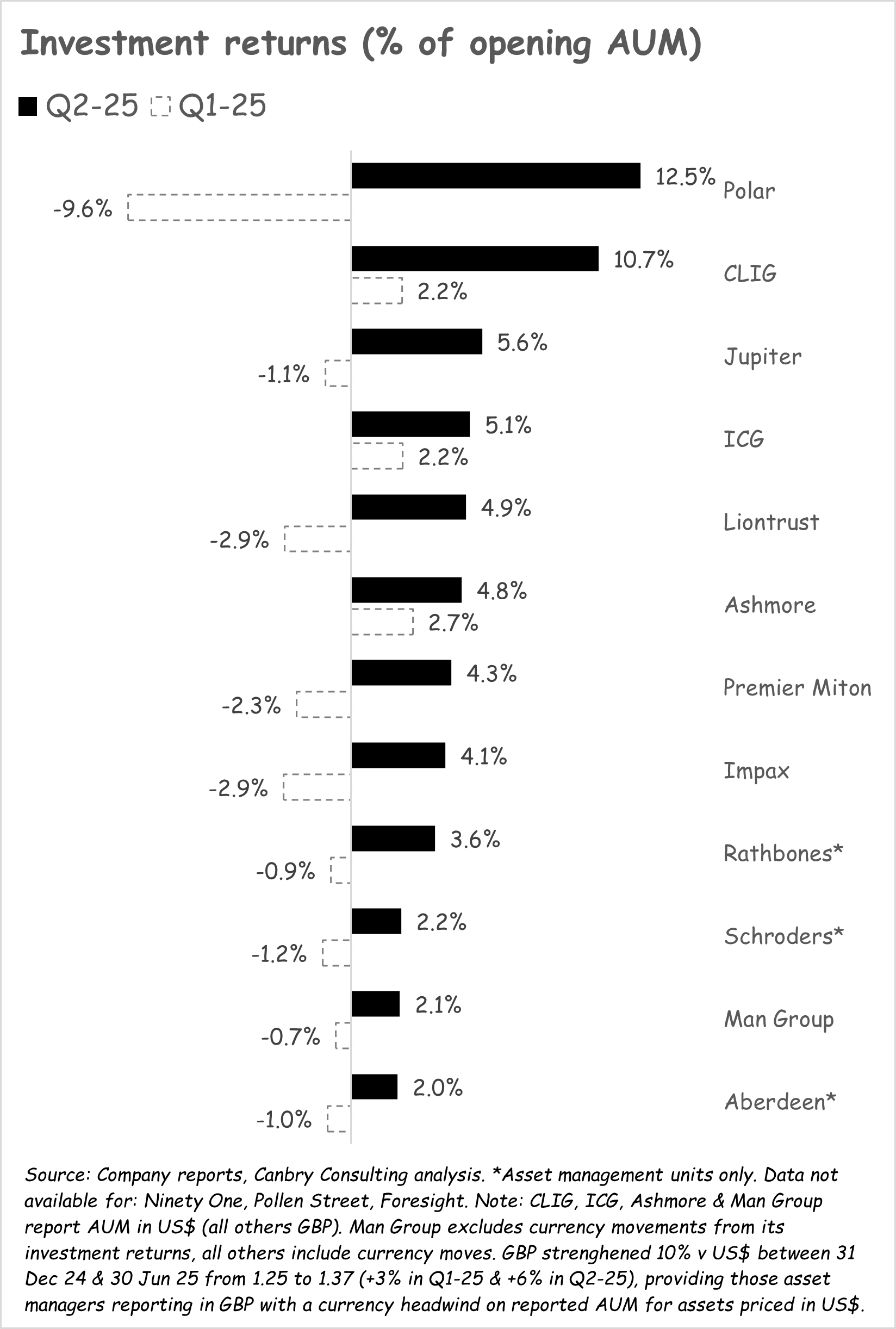

Volatile investment returns (a gross understatement)

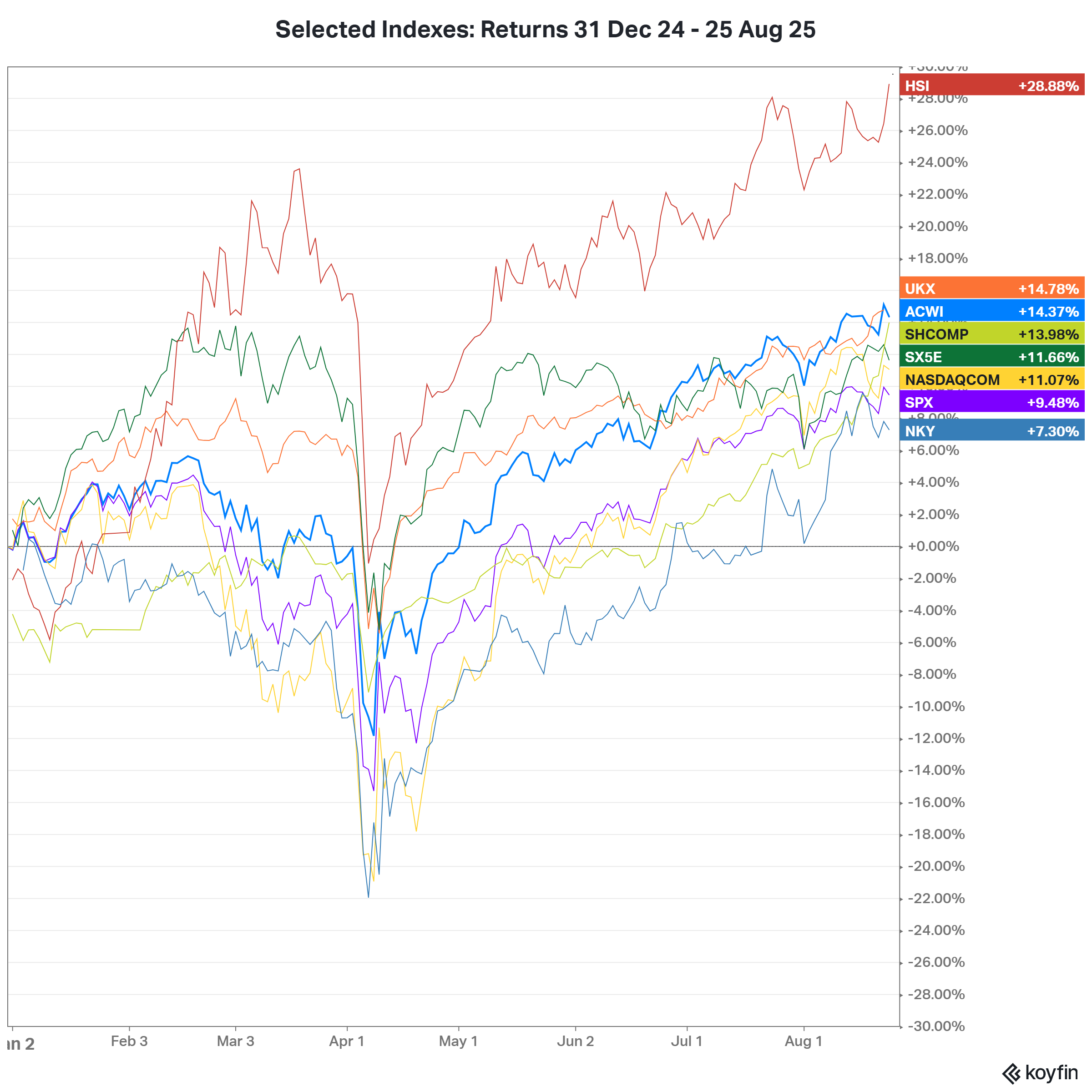

To a degree, and especially over the short term, asset managers are subject to the movements of the markets they invest in. And H1-25 had some pretty big movements! Major equity indexes have mostly returned 7.5% - 15% in 2025-to-date, with the exception of Hong Kong, which ran away. But falls around April’s ‘tariff turmoil’ resulted in 20%+ falls from the start of the year in some cases. The chart below shows the context asset managers have been operating in during 2025.

That translated to some pretty big investment return differences, and swings between Q1 and Q2. Polar Capital, with a heavy exposure to technology equities, had an especially large investment return swing between those two quarters. It’s also worth flagging again the impact of currency movements in the chart below (see note below chart).

I reckon the main message when it comes to investment returns’ impact on AUM is that asset managers are experiencing some pretty intense buffeting, as markets remain volatile.

While cautious optimism is the prevailing outlook for H2 flows, who knows what markets might hold?

Look out for part 2 of this post next week

In part 2, I’ll be digging below the AUM line and start looking at the impact of things like strategic changes, cost cutting measures, acquisitions, and management changes, and how they might be affecting share price moves.

Be sure to subscribe to TheInvestors.blog below to get notified when part 2 drops and to keep up to date with the UK asset and wealth management sectors.

And if you think TheInvestors.blog is worth telling others about and sharing, I’d be most grateful if you do.

Disclosure: At the time of writing, Paul Bryant was a shareholder in a number of the companies mentioned in this publication.

Very good detailed research.