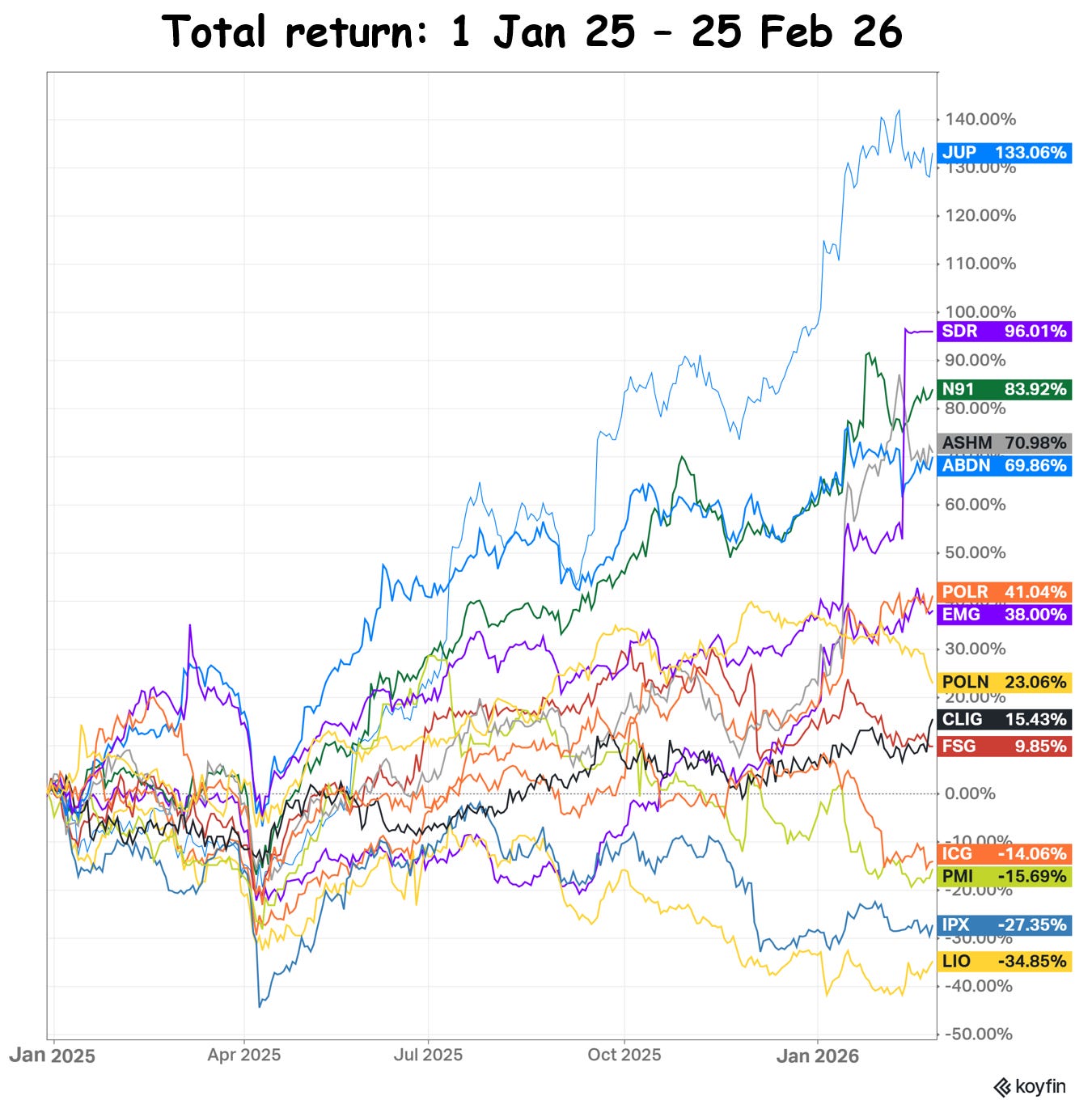

Jupiter jumps again (and there might be more to come)

Jupiter has turned from laggard to leader. The share price has had a huge recovery. Fundamental valuation suggests there might be even more upside.

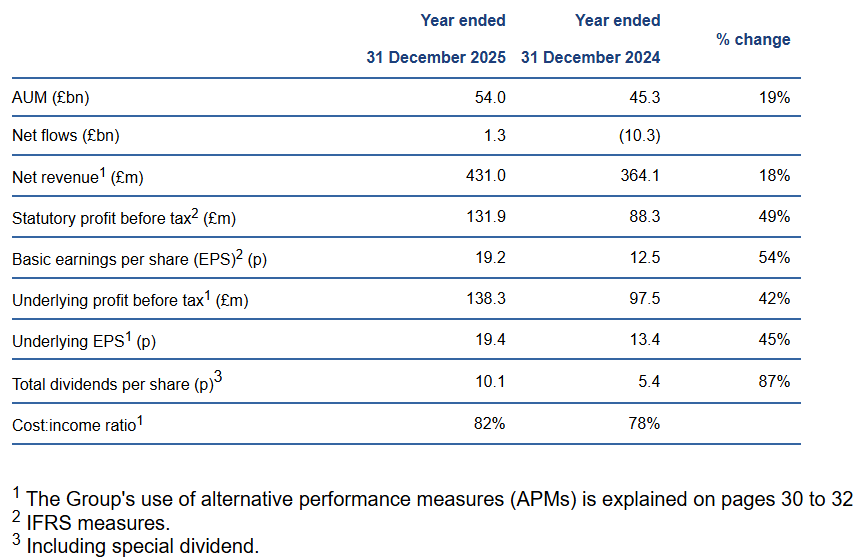

Jupiter released its 2025 results today. The dramatic turnaround is well on track. Here’s the summary from the results release:

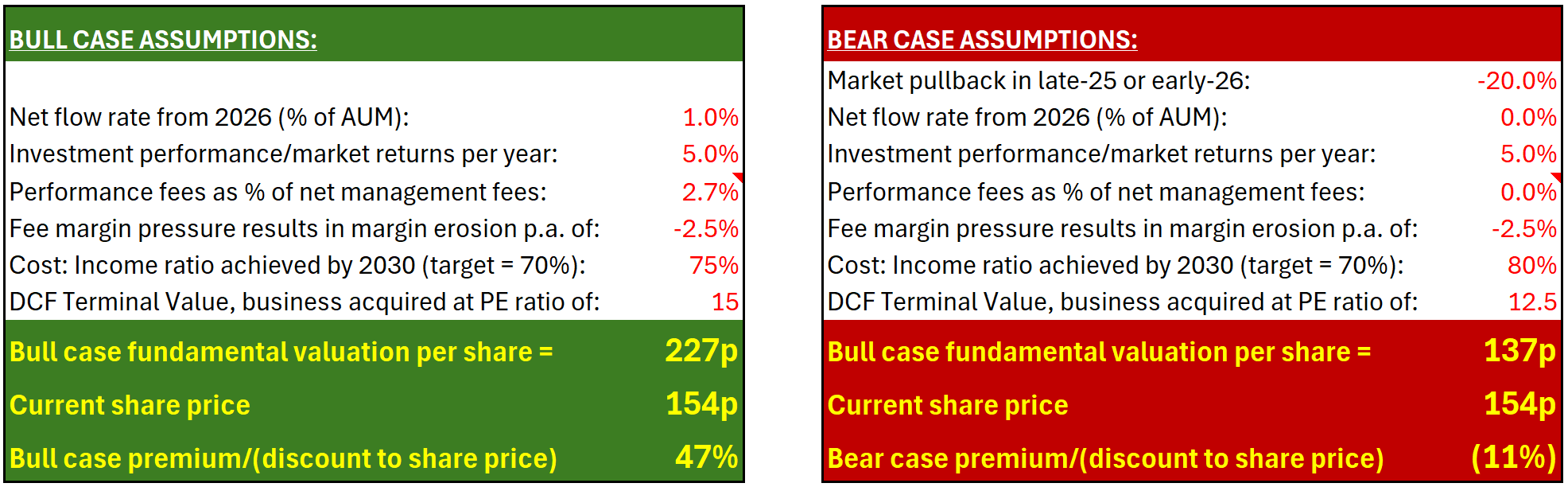

In Oct 25, I went into some detail on Jupiter’s valuation in this post:

At that time, my bull case DCF valuation produced a fundamental valuation of 227p per share, my bear case 137p. The current share price (26 Feb 26) is 195p, up c. 3.5% on the day of this results announcement. Here’s the assumptions behind those previous valuations (share prices in the table are at the time of publication of the above post).

And here’s a steer on how the above forward assumptions align with the actual 2025 performance and management’s commentary and outlook from their presentation earlier today (spoiler: they look a bit conservative):

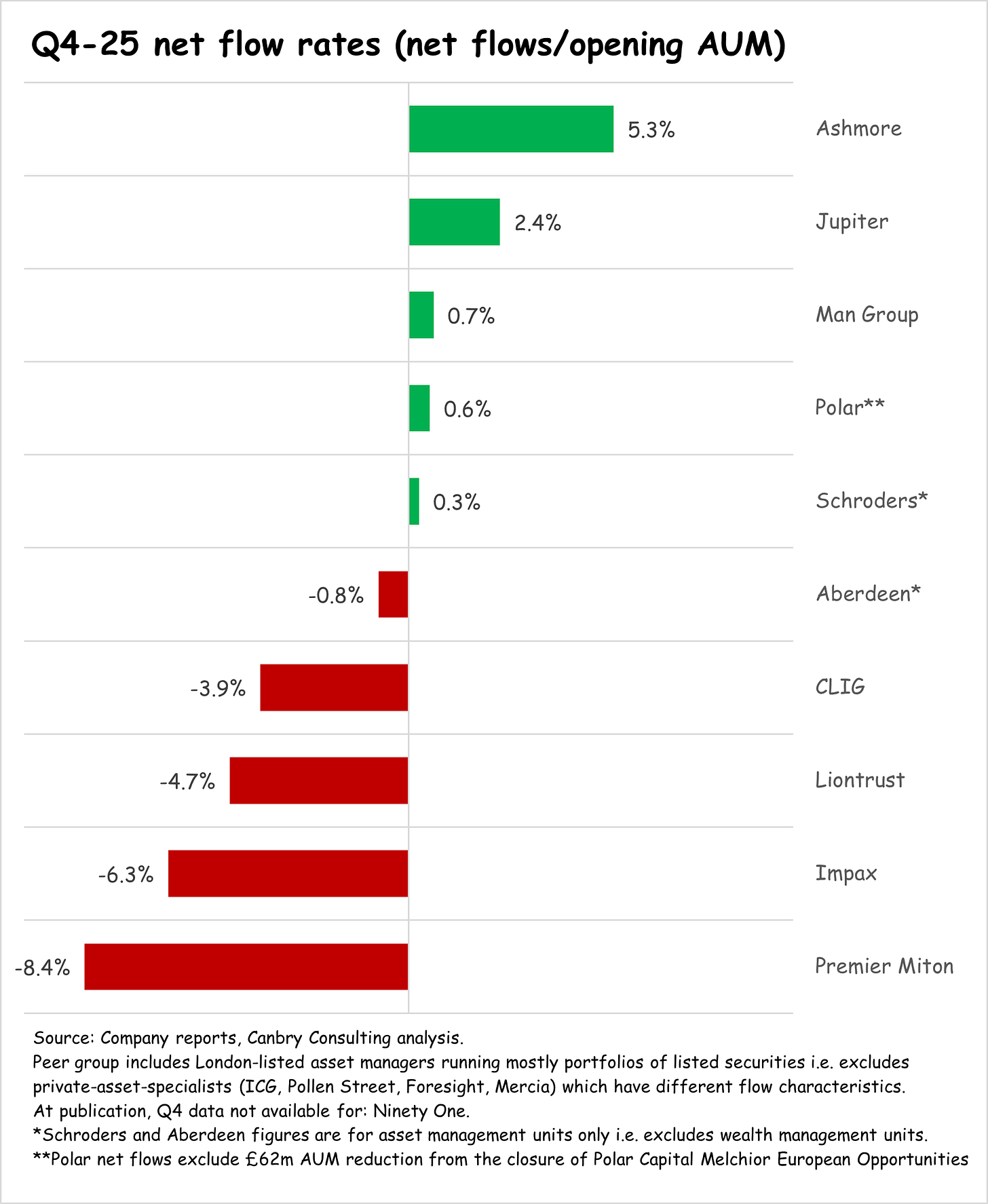

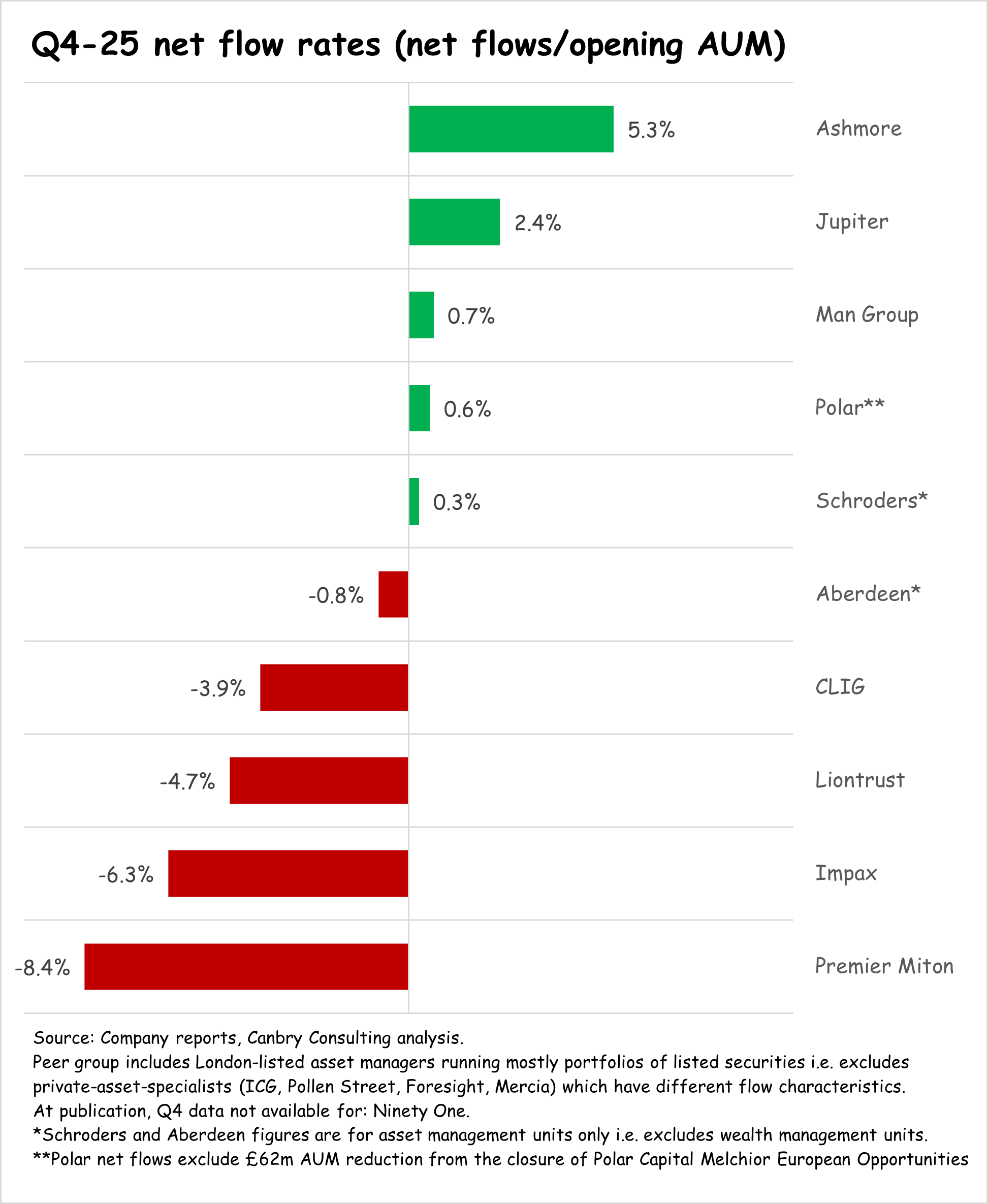

Net flow rate: Net flow rate over 2025 was +2.9% but it jumped in Q4 (+2.4% in Q4 alone - nearly the highest in the sector - see chart below). Management have said positive flow momentum has continued into Q1-26 with £1bn+ of net flows, that’s around +1.8% of AUM in 2 months alone. My bull case net flow rate assumption is looking light.

Investment performance: Looking forward, there’s obviously huge uncertainty around this assumption. But in 2026, so far so good. The MSCI ACWI is up 4.7% year to date.

Performance fees: Jupiter knocked it out of the park in 2025 with £120m of performance fees (up from £31m in 2024). As a percentage of net management fees, that’s 27%, 10X my assumption of 2.7% which was based on historical averages. The large performance fee number has also been the main driver of Jupiter announcing a special dividend. (The total 2025 dividend including the special dividend translates to a yield of c. 5%). The jump in performance fees in 2025 will obviously push my bull case valuation upwards. Management have guided around £20m in 2026 which is about double my previous assumption. My bull case performance fee assumptions are looking light over the short term. Of course, there’s no guarantee of these materialising.

Fee margin: Net fee margin closed 2025 a touch lower than my previous assumption (65bps versus my assumption of 66bps). Management have guided a reduction to 63bps for 2026 which is slightly lower than my previous assumption of 64bps. My net fee margin is looking slightly high, but not materially so.

Cost: Income ratio: This was 82% in 2025, about in line with my assumption. Management have maintained their target of 70% by 2030, and stated in the results announcement they have increased confidence in meeting this target. Mine is a little more conservative at 75% by that time. If management meet their targets, my cost assumptions are looking a little high.

In summary, Jupiter’s 2025 performance has been far higher than my previous assumptions, driven mainly by a big jump in performance fees. However, management’s outlook and guidance going forward are also mostly higher than my previous bull case assumptions. My bull case valuation is clearly going to go up from the previous 227p per share. I’ll be posting full details of this revised valuation soon…

Shareholders have enjoyed stellar returns from Jupiter over the last year or so (following a huge fall in the share price over 2022, 2023, and 2024). But there may very well be more juice to come in Jupiter’s jump.

Be sure to subscribe to TheInvestors.blog to get notified when my updated valuation drops and to keep up to date with the UK asset and wealth management sectors.

And if you think TheInvestors.blog is worth telling others about and sharing, I’d be most grateful if you do.

Disclosure: At the time of writing, Paul Bryant was a shareholder in Jupiter Fund Management.

Bit of director buying too - the day after these results. https://www.londonstockexchange.com/news-article/JUP/director-shareholding/17481368