Lies, damned lies, and PE ratios (part 1 of 2)

When valuing asset managers, the (usually) useful PER can sometimes be misleading. There is a fix.

This is not investment advice. Please read TheInvestors.blog disclaimer here.

Price earnings ratios (PERs) can certainly be useful when looking at asset manager valuations. Because most have little or no debt, one of the main weaknesses of the PER – not taking debt levels into account - is not such a big deal.

I use it a lot in my work as an equity analyst (or at least a modified version – which I will explain), especially as a relative valuation tool to compare the value of an asset manager to peers or to its own valuation history (see the EndNote: PER versus DCF at the bottom of this post).

But sometimes, PERs in asset management can become extremely distorted and serve no purpose whatsoever, or even be downright misleading.

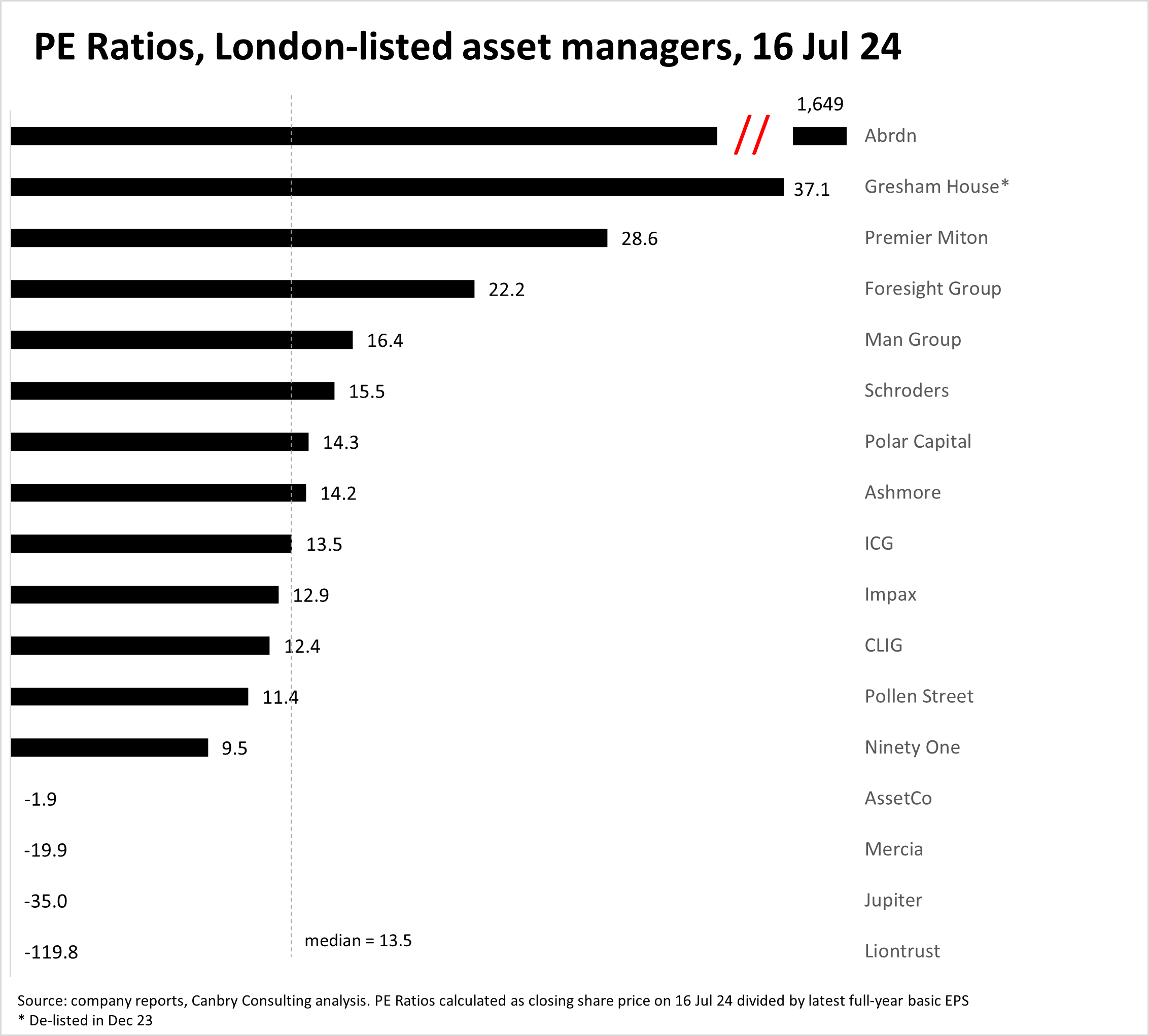

Take a look at the current PERs for a group of London-listed asset managers [I know negative PERs don’t make sense, but I’ve included these deliberately in the chart below just to illustrate the results of the maths behind PERs, so bear with me on this].

While there’s a reasonably clear clustering in the 10-22 PER range which may be useful to analyse in a bit more detail, there’s also almost as many ‘outliers’ well outside this range.

For example, Abrdn’s PER of over 1,600 (yes, the maths is correct) is clearly an anomaly (it made a very tiny profit in its last financial year, and we know what happens when you divide by nearly-zero). And Gresham House saw it’s PER jump from 23 to 36 on 17 Jul 23 on the announcement that its board would be recommending the acceptance of a takeover offer (it subsequently delisted in Dec 23).

Meanwhile AssetCo, Mercia, Jupiter and Liontrust made statutory losses, making their PERs meaningless (with a negative PER you can’t answer the question ‘how many times earnings are you paying for the company?’ which is the whole point of PERs).

Then to add insult to injury, take a look at the chart below, which shows how PERs can change from one day to the next because of the volatility of asset managers’ statutory earnings. The black bars show the PER at the end of the day on which the latest full-year results were announced, while the grey bars show the PERs from the day before (with that grey PER based on the previous year’s earnings).

There are some wild swings, with a mix of reasons behind these swings: some are driven by the accounting rules applicable to asset managers, while others are certainly due to a change in fundamentals, for example:

I mentioned Abrdn’s distorted PER of around 1,600 above, but now highlight that just the day before, its PER was actually negative (because it made a loss in the prior financial year - heavily impacted by a non-cash impairment charge on intangibles added to the balance sheet, such as customer contracts, on the execution of previous acquisitions).

Premier Miton’s PER jumped from 9.5 on 4 Dec 23 to 24.2 on 5 Dec 23 after basic EPS fell from 6.5p in its FY22 to 2.5p in FY23, mainly due to a sharp fall in revenue – so no distortion there due to fundamentals. The drop in revenue was well flagged and baked into the share price which didn’t move much when earnings were announced on 5 Dec 23 (from 62p to 60.5p), but the move in eps had a huge impact on PER.

ICG’s PER fall from 23.6 on 27 May 24 to 14.5 on 28 May 24 was largely due to a jump in eps from 98p to 166p, which was in turn largely driven by some big gains in its on-balance-sheet investment portfolio (+£405m in FY24 v +£173m in FY23). These are both realised and unrealised gains, so are very much influenced by fair value accounting rules.

Mercia’s PER fell from +48 on 1 Jul 24 to negative on 2 Jul 24 (without the share price moving much) as basic EPS fell from 0.64p in FY23 to -1.71p in FY24, mostly due to a non-cash impairment of an on-balance-sheet investment.

And Jupiter’s and Liontrust’s PERs also fell from the +9-12 range pre-results announcement to negative as basic EPS moved from positive to negative territory. In the case of Jupiter, this was largely driven by a non-cash £76m impairment on the goodwill related to its 2020 Merian acquisition; but in the case of Liontrust, it was more fundamental than accounting, with revenue falling 19% and administrative costs increasing 3%.

You get the picture … these dramatic moves in PERs just diminish the usefulness and credibility of the metric, especially when it is calculated using statutory earnings.

It’s tempting to toss the PER out as a valuation or valuation comparison tool entirely. But I think that would be removing a really useful tool from investors’ armoury.

There is a way to modify the PER for asset managers to get a very good comparative valuation tool of asset managers’ underlying businesses. And when combined with some fairly straightforward balance sheet analysis, its usefulness ratchets up again.

In part two of this post ‘Will the real PE Ratio please stand up’, I’ll explain this modification, and illustrate its use when looking at the above cohort of asset managers. I’m pretty sure you’ll find that analysis to be an eye opener.

It will be published sometime during the week commencing Monday 22 Jul 24, so be sure to subscribe to TheInvestors.blog to see that analysis and also to keep up to date with further developments in the UK asset and wealth management sectors.

And if you know of anyone who you think might be interested in that post or this newsletter more generally, please share these details, I’d be most grateful if you do.

EndNote: PER vs DCF

As an analyst covering asset managers (AMs), my go-to valuation methodology is usually a discounted cash flow (DCF). This is intended to give my readers a good idea of the fundamental value of the business under review, given my growth and profitability assumptions.

If readers think those assumptions are too aggressive (or conservative), they will of course conclude that my fundamental value is too high (or low). Even if they do, the DCF and its assumptions should be a useful data point for investors – highlighting potential discrepancies between fundamental value and current market value. It’s an exercise in forming an opinion on the absolute value of a business.

But I also try and add a data point around relative value in my research notes - the value of an asset manager compared to peers, and compared to its own valuation history. I try to present a picture of which AMs are commanding premium or discounted valuations compared to peers, why that might be the case, and in particular, to flag when those premiums or discounts don’t seem to make sense.

Usually, I would use the price earnings ratio or PER to do this, and although it is definitely overly-simplistic and certainly not robust as a standalone valuation tool, it is a useful ‘back-of-the-envelope’ comparison between valuations. Especially when used in its modified form which will be explained in part 2 of this post.

Disclosure: At the time of writing, Paul Bryant was a shareholder in a number of the companies mentioned in this publication, and covered Impax Asset Management, Polar Capital, and Mercia Asset Management as an analyst on behalf of Equity Development Limited. Read Equity Development’s research on Impax Asset Management here, on Polar Capital here, and on Mercia Asset Management here. (Please read this link for the terms and conditions of reading Equity Development’s research).