D2C platforms fly high in Q1

AJ Bell D2C & interactive investor (owned by Aberdeen) drive upgrades and share price jumps - in an otherwise 'slow news' quarter in wealth management

TheInvestors.blog is not investment advice. Please read the disclaimer here.

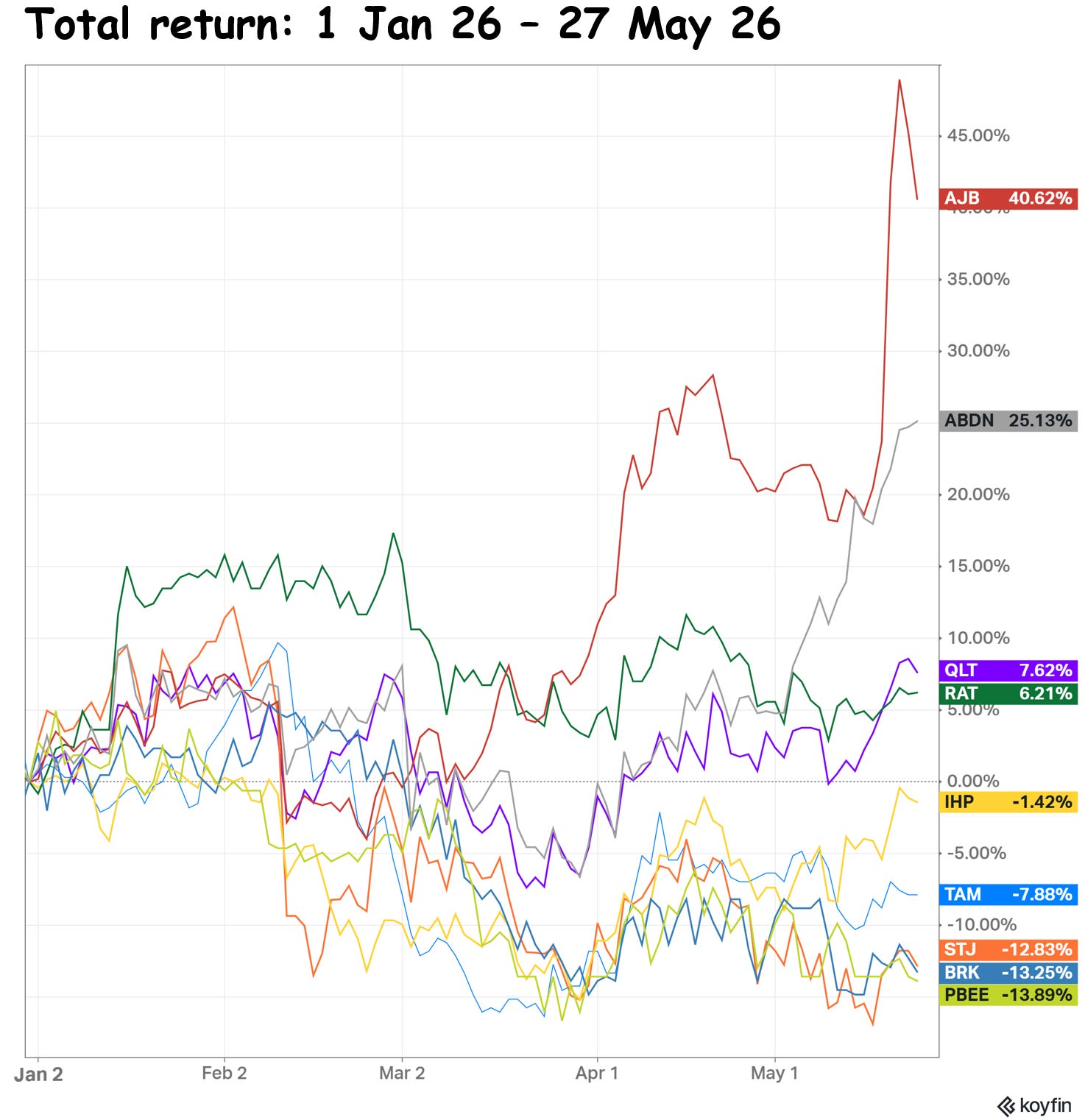

In the London-listed wealth management sector, there are two significant share price stories so far in 2026: AJ Bell (+41%) and Aberdeen (+25%).

It’s not always the case that share prices correlate with fundamentals in the short term, but in Q1, they gave a pretty good steer.

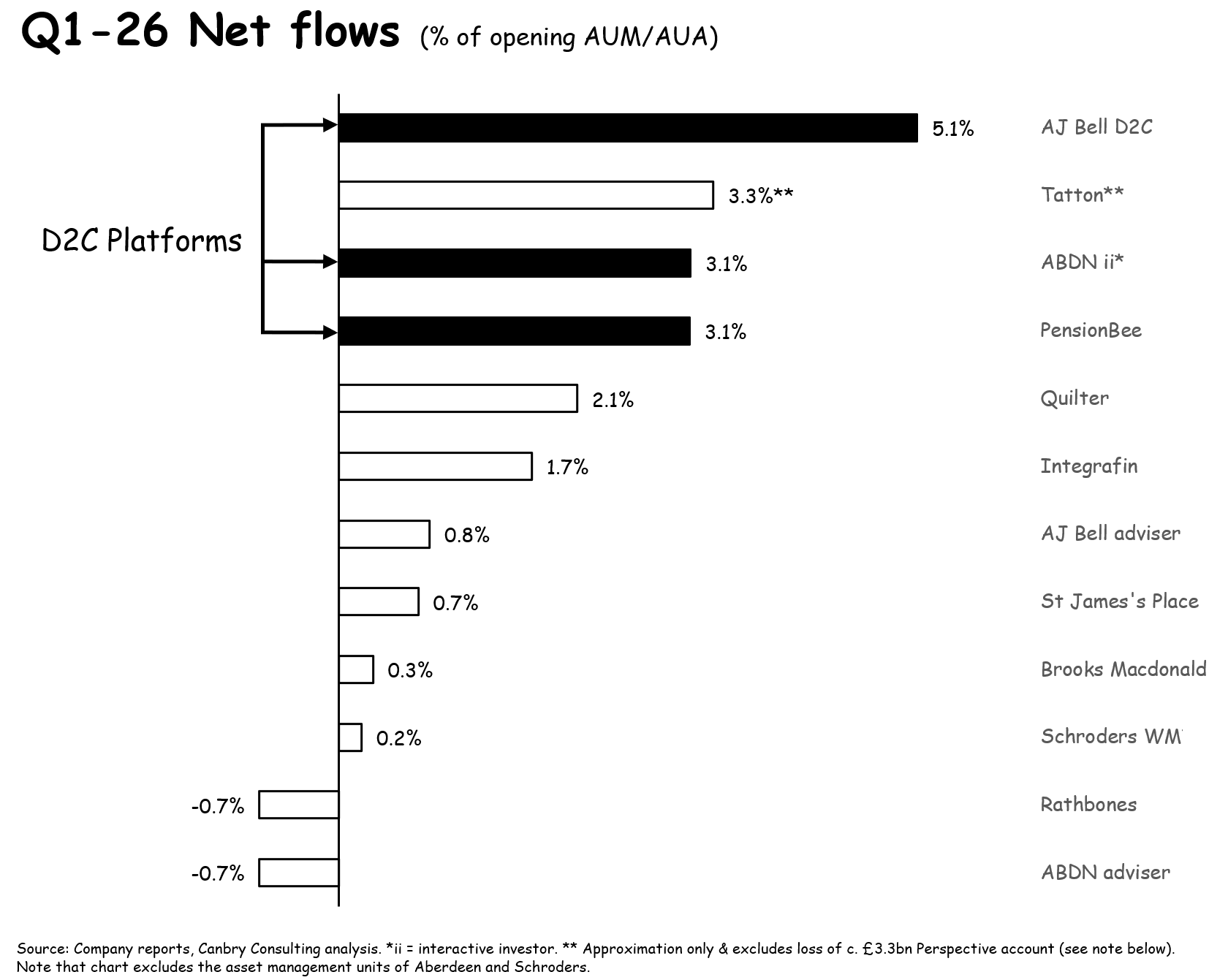

Net flows are one of the most important metrics in wealth management, and you can see how strong these were for AJ Bell D2C and Aberdeen’s interactive investor in the chart below (Tatton and PensionBee had unique situations in Q1 which are discussed in more detail after the chart).

Two things to bear in mind in the company discussions below. 1) Q1 is usually a strong quarter for wealth managers as it includes the run-up to the UK tax-year-end. Investors are often making sure they have utilised their annual tax-free ISA allowances etc so there tends to be a flurry of investment activity. So I’ve compared net flow performances to one-year prior, Q1-25. 2) Q1 was a weak quarter for investment performance contribution to AUA. January and February were relatively strong, but things turned around in March as the conflict in Iran ratcheted up. The median investment performance contribution to AUA in Q1 was -1.6%.

AJ Bell

It was a strong quarter for AJ Bell, but especially for its D2C business:

Total customer numbers: +50k to 723k (+7% in the quarter, +22% y-o-y)

D2C customer numbers: +46k to 534k (+9% in the quarter, +28% y-o-y)

Advised customers: +4k to 189k (+2% in the quarter, +7% y-o-y)

Total AUA: +1% in the quarter to £110bn, +20% y-o-y

Total net flows +£2.7bn in Q1-26 v +£1.8bn in Q1-25

D2C net flows +£2.2bn in Q1-26 v +£1.4bn in Q1-25

Adviser net flows +£0.5bn in Q1-26 v + £0.5bn in Q1-25

But the real surge in the share price was with the release of interim results on 21st May, when the impact of the above customer and AUA strength on financial results and outlook became clear. Shares jumped 15% on the day with: PBT +35% to £93bn; AJ Bell stating it expects full year revenue margin, PBT and PBT margin to be higher than previously guided; and a further £15m buyback programme was announced (following on from the previous £50m programme).

Aberdeen

Aberdeen (and Schroders) have a different characteristic to others in this peer group. The bulk of their AUM/AUA is in their asset management businesses. Aberdeen has £383bn AUM in asset management, and £173bn in wealth management (£95bn interactive investor; £79bn adviser). But interactive investor is the jewel and crucially important at group level. It generated £155m of adjusted operating profit in 2025, compared to £86m by adviser and £64m by asset management.

Interactive investor’s impact is clearest when you look the strength of its performance in the quarter, the relative weakness in the rest of the group, and then the positive share price reaction of the group.

In Q1:

Interactive investor added 13k customers to reach 513k and generated net flows of +£3.0bn (its highest ever quarterly net flow), compared to +£1.6bn in Q1-25.

Adviser recorded net outflows of -£0.6bn (Q1-25: -£0.6bn).

Asset management recorded net outflows of -£5.4bn (Q1-26: -£6.4bn).

Shares didn’t react immediately following the Q1 update, treading water for a few days. But then went on a rip, rising 19% between the 5th May and the 27th May.

Proactive reported an upgrade by Citi which included the comments: “Citi highlighted significant re-rating potential across Aberdeen’s business divisions, particularly the investments arm and interactive investor (ii), the direct-to-consumer investment platform acquired in 2022…. suggesting the market is not yet giving full credit to ii’s growth trajectory or the strategic optionality within the wider group.”

Tatton

There’s an anomaly in Tatton’s flow rate analysis this quarter. The above chart excludes the impact of the loss of its Perspective Financial Group mandate from Jan 26, which reduced AUM by c. £3.3bn. It looks like a big headline AUM impact but in reality, it’s just not that big of a deal. This loss was well-flagged from back in June 2025, and it was a low margin account making up c. 14% of AUM but only 2.4% of revenue.

Aside from the Perspective account loss, Tatton maintains exceptionally strong flows and from the details released in its April trading update, it looks on course to exceed my forecasts, and well on course to reach its medium-term growth goals. You can see a summary of my latest research note below:

PensionBee

PensionBee’s UK business looks to be in fine shape and continues to grow strongly. Net flows were solid in the quarter: £221m versus £214m in Q1-25. It added 10k new customers to reach 315k. And AUA was £7.5bn on 31 Mar 26, up 29% y-o-y, with PensionBee announcing it had reached £8bn on 27 Apr 26.

But as I’ve previously written, the share price looks stuck until we start seeing some numbers out of its new venture in the US. It’s a potentially game-changing move for PensionBee, looks well thought out, but it’s early days. My previous post covering this below:

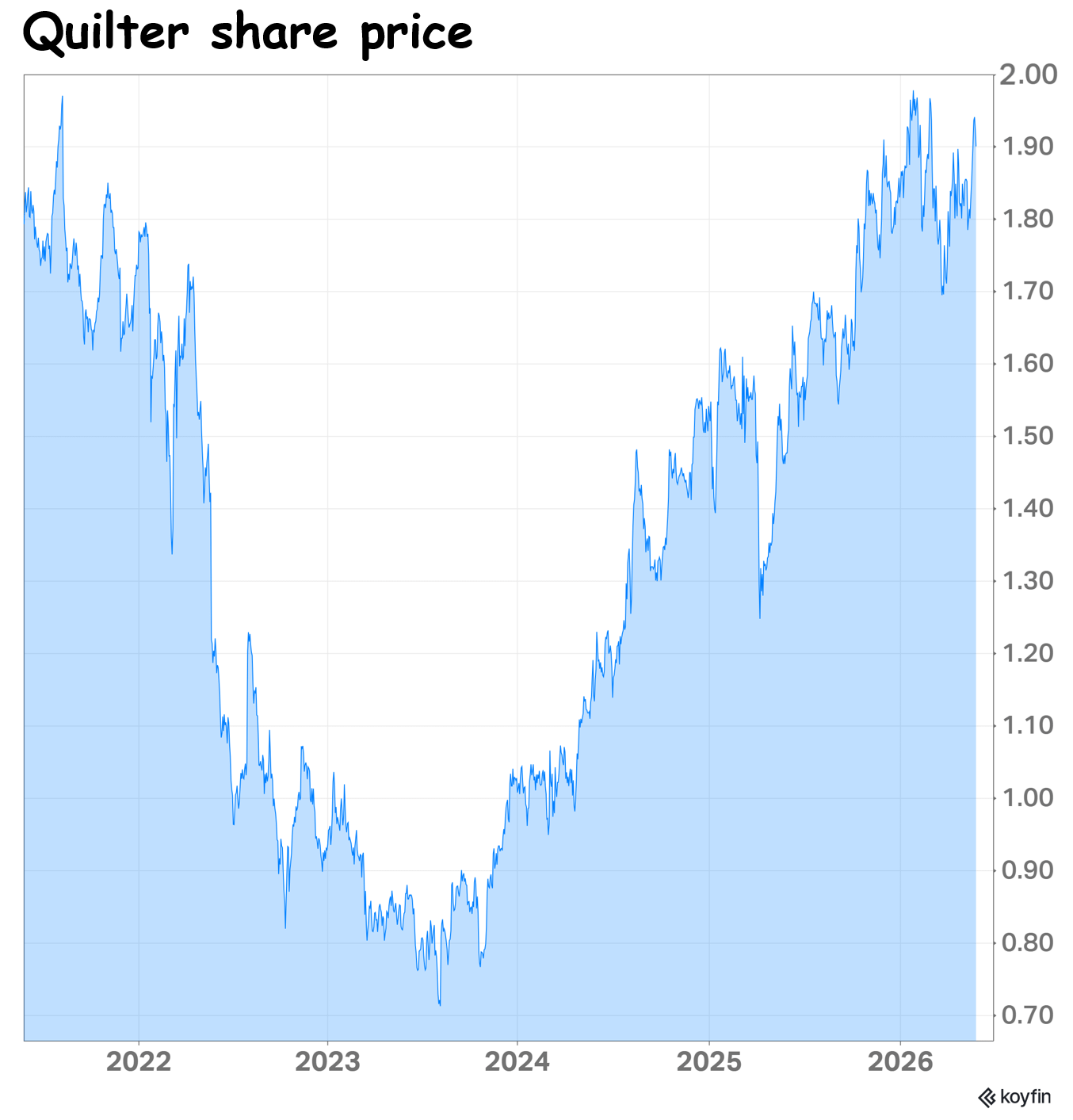

Quilter

Quilter is going strong. Net flows of +£3.0bn in Q1-26 were well up on Q1-25 (£2.2bn). It was the 9th consecutive quarter of positive net flows. AUA is up 19% y-o-y to £142bn. Its WealthSelect MPS offering is a key growth area, reaching £26bn AUA, up 35% y-o-y.

This business looks in so much better shape than back in 2022 and 2023 when it was struggling to maintain positive net flows. The share price is reflecting that though, it’s had a huge recovery and is back to around 2021-high levels.

Integrafin

Integrafin runs the adviser platform, Transact. Net flows were solid at +£1.3bn, up 8% on the £1.2bn of Q1-25. Gross inflows (before outflows) hit a record level £3.1bn. This business has enjoyed steady growth, but the share price has been stuck in the £3-£4 range over the last two years or so. It’s one I will be doing a deeper dive on soon.

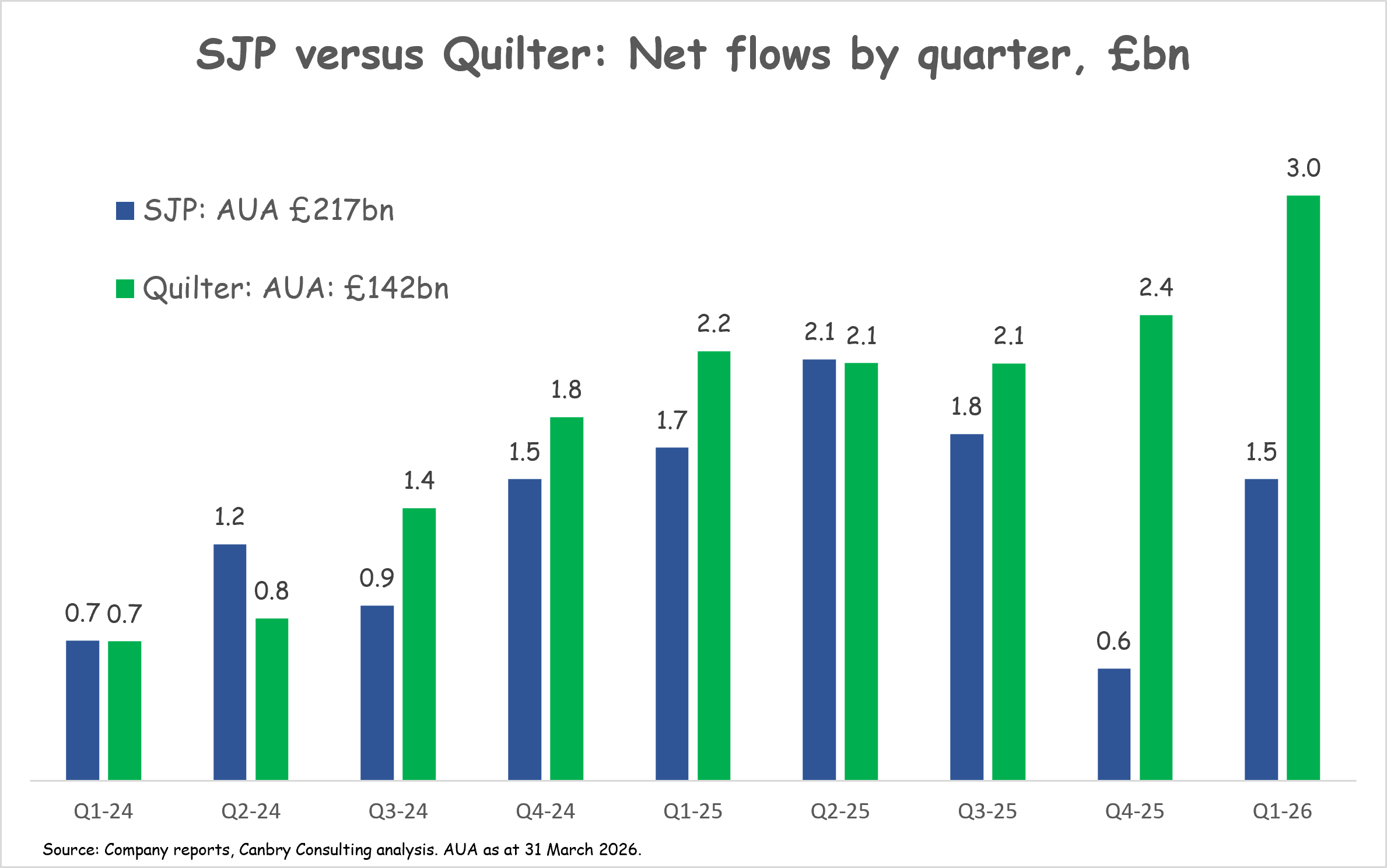

St James’s Place

A so-so quarter for SJP with net flows of +£1.5bn, down from £1.7bn in Q1-25. A little worryingly, flows have also been very inconsistent recently. Just compare SJP’s flows to Quilter, which is good comparator - also a large (albeit smaller than SJP), adviser-led wealth manager. Net flows have diverged quite significantly recently.

Also, SJP’s shares haven’t recovered from the “AI will destroy advisers” pullback of Feb 26 - unlike Quilter’s.

Investors seem a little unconvinced by SJP at the moment.

Brooks Macdonald

Brooks produced a send consecutive quarter of net inflows following an awful run of nine quarters of net outflows. In Q1-26, it generated a marginally positive net flow of +£58m, slightly up on Q4-25 (+£50m) but substantially higher than Q1-25 (-£129m).

The turnaround under Andrea Montague seems to be getting some traction, but it’s not showing up in the share price yet.

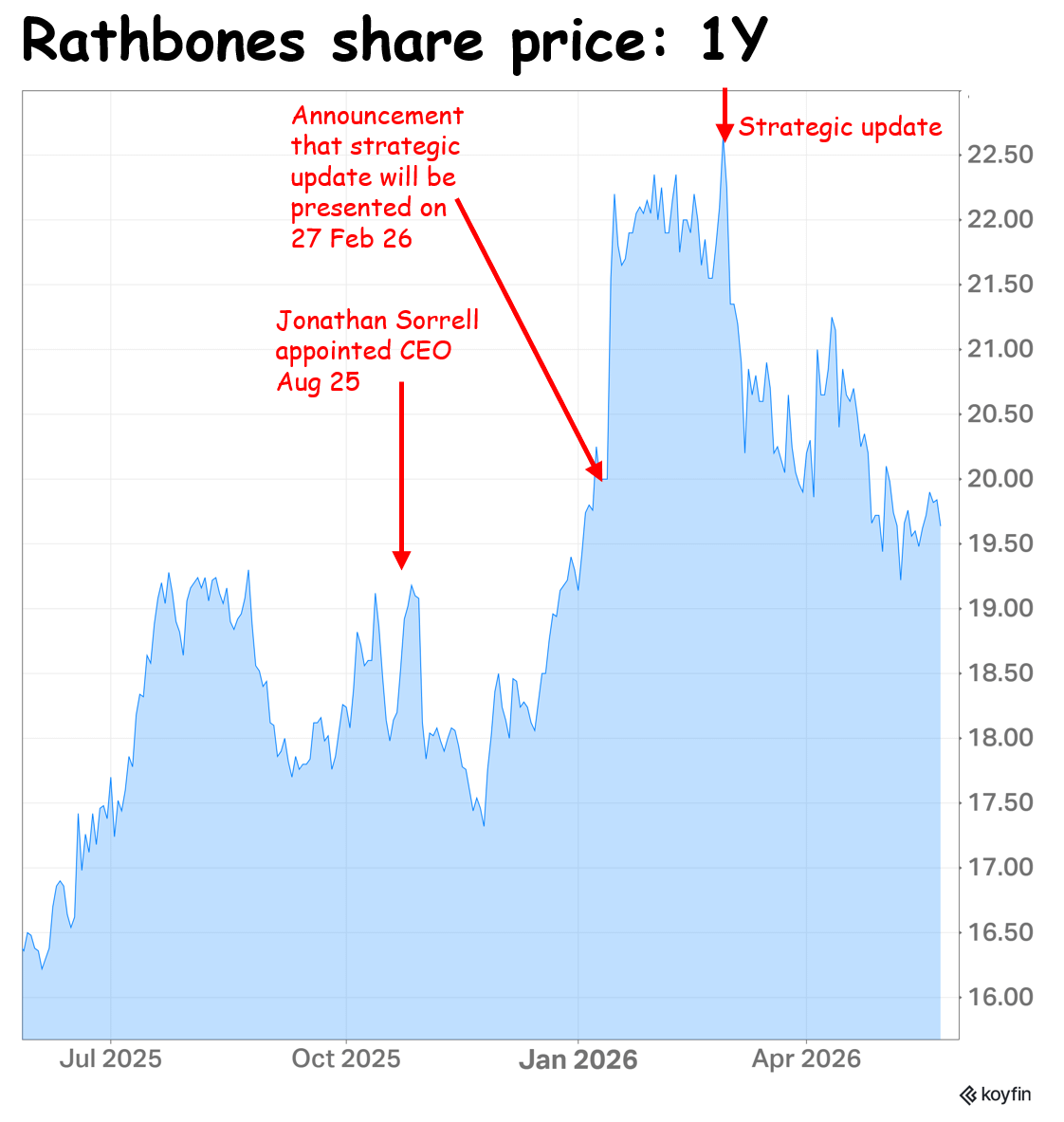

Rathbones

Rathbones is only just beginning its journey under new CEO Jonathan Sorrell, who has made a return to net inflows a top priority. The business has suffered consistent net outflows over the last few years, with its acquisition of Investec Wealth and Investment contributing to these outflows.

Q1 was once again negative with -£0.85bn of net outflows (Q1-25: -£0.78bn). Investors were probably expecting something a bit more dramatic from Sorrell’s strategic update in Feb 26, with the shares rising sharply in anticipation but then falling back after its delivery.

It looks like Rathbones is going to have to start to deliver its promised growth before investors are convinced.

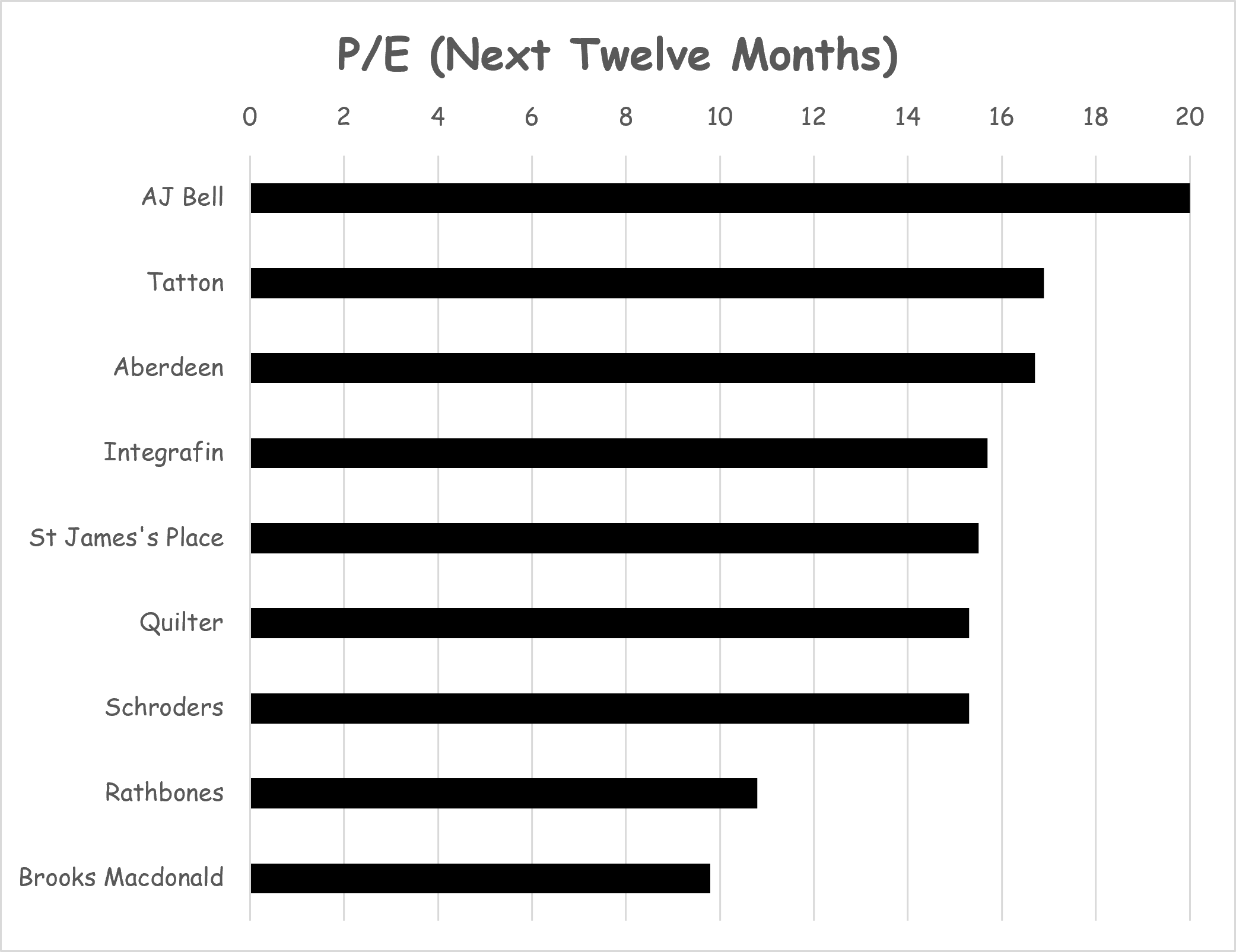

Valuations

A good place to finish this post is a quick look at valuations. Below is a chart of forward PE ratios (source: Koyfin).

AJ Bell and Tatton seem to fully justify their premium rating, and these premiums don’t look excessive. You might argue that Quilter has room to move up into a premium rating too.

Rathbones and Brooks Macdonald carry discounted ratings, right now probably deservedly so. But if their turnarounds gain traction, there’s certainly scope for big move upwards.

Be sure to subscribe to TheInvestors.blog below to keep up to date with further insights into the UK asset and wealth management sectors.

And if you think TheInvestors.blog is worth telling others about and sharing, I’d be most grateful if you do.

Disclosure: At the time of writing, Paul Bryant was a shareholder in a number of the companies mentioned in this publication and covered Tatton Asset Management as an analyst on behalf of Equity Development Limited. Read Equity Development’s research on Tatton here. And please read this link for the terms and conditions of reading Equity Development’s research.