Has Evelyn deal flagged hidden value in London-listed wealth management?

NatWest's punchy Evelyn multiple (for pedestrian performance compared to some listed peers) suggests a hungry acquirer might pay a meaningful premium for the 'right' target.

TheInvestors.blog is not investment advice. Please read the disclaimer here.

Wealth manager Evelyn Partners has been under private-equity ownership. It’s being acquired by NatWest.

There’s been plenty of commentary on what this deal means for the ‘40 or so’ private‑equity players in UK advice. Citywire captured it well in their piece: Evelyn’s £2.7bn sale sets high marker for PE sales, noting:

“Other PE investors will be looking to the headline price they negotiated as a marker of ultimate success. It’s a good sign for them that banks seem willing to throw cash around chasing wealth businesses. Barclays, RBC and Lloyds all sounded out Evelyn at some point so it’s not unreasonable to think they will sound out other deals in the coming years.”

But there’s been less said about the implications for London-listed wealth managers. Evelyn competes with quite a few of these, so comparisons are useful. And once you dig into the Evelyn deal, it’s not a huge leap to conclude there might be a big payday looming for shareholders of the ‘right’ listed company.

About Evelyn, financials, acquisition price

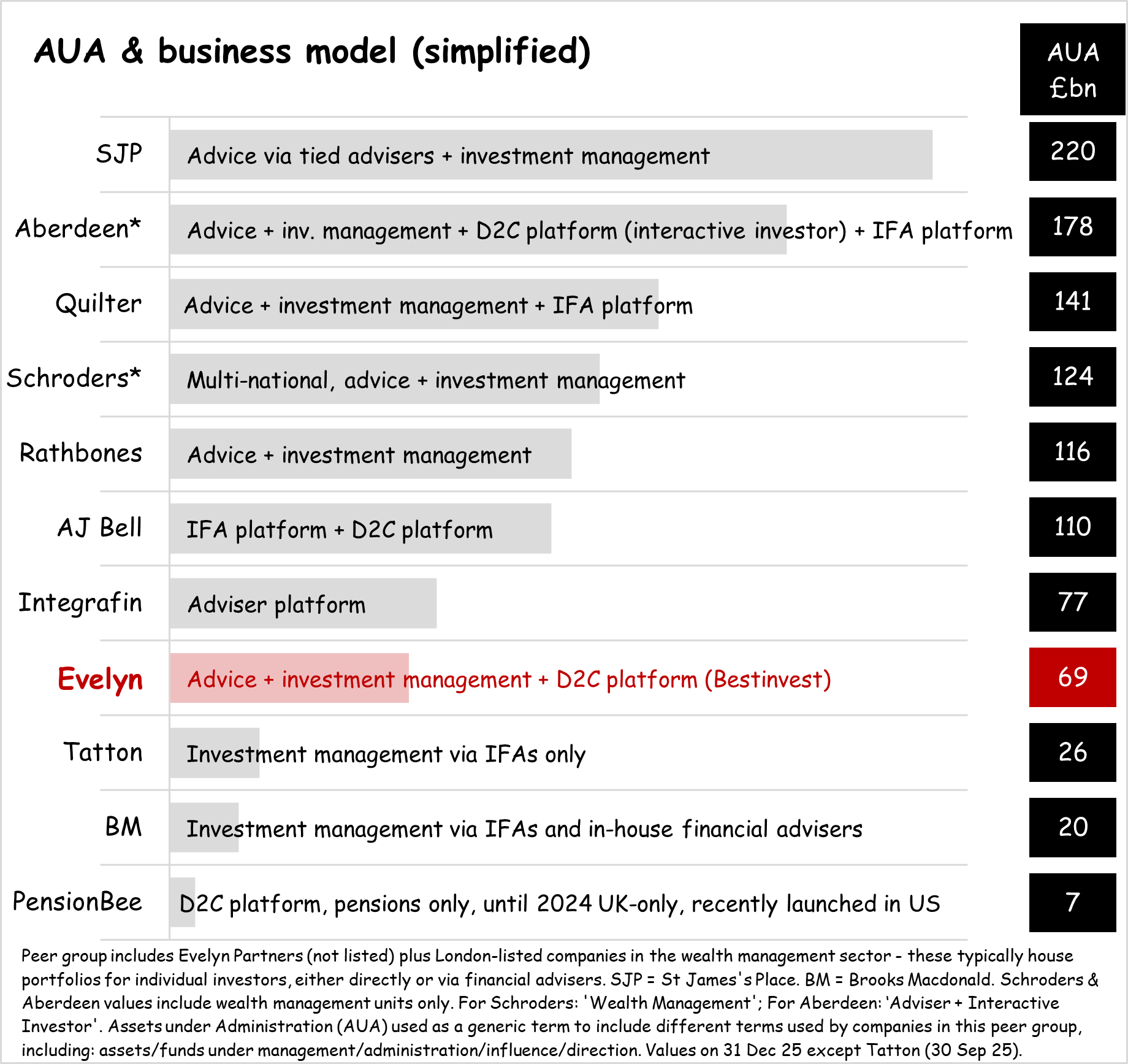

Evelyn has a broad wealth management offering including financial planning, discretionary investment management and a direct-to-consumer platform, BestInvest. It has approximately 270 financial planners and 325 investment managers (source: NatWest acquisition announcement). Here’s how it’s size and business model maps against London-listed wealth management peers. [AUA = assets under administration]

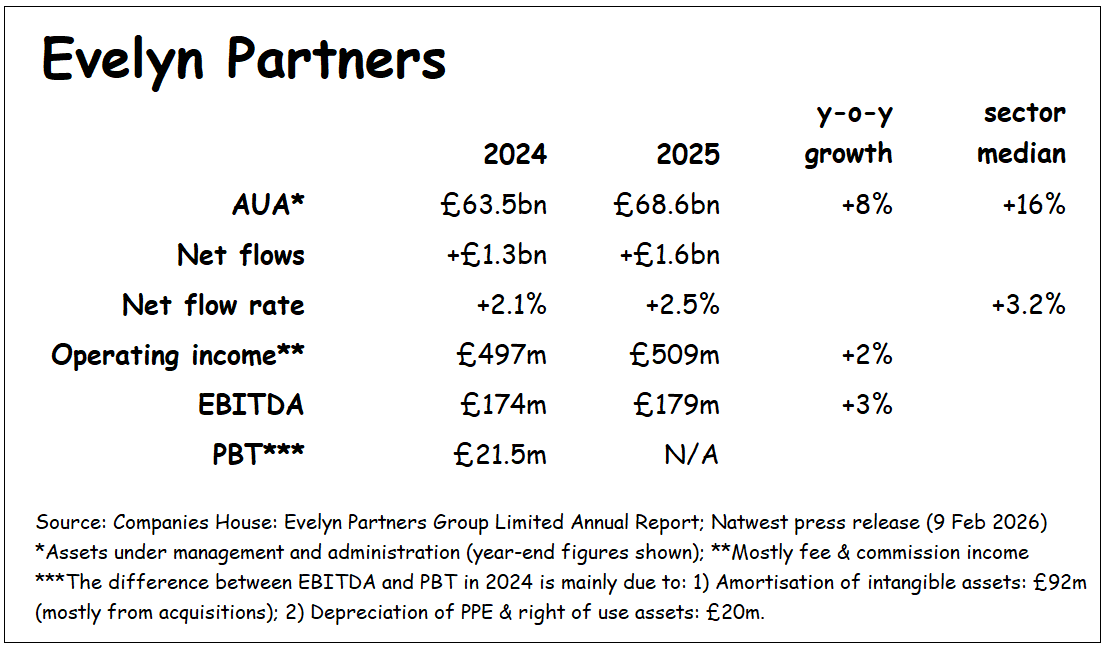

And here’s what we know about some of Evelyn’s key metrics (2025 accounts haven’t been published yet but a few numbers were disclosed with the acquisition announcement):

NatWest is going to be buying the business for £2.7bn enterprise value. Let’s see how that stacks up against others in the listed wealth management space.

Acquisition price looks punchy…

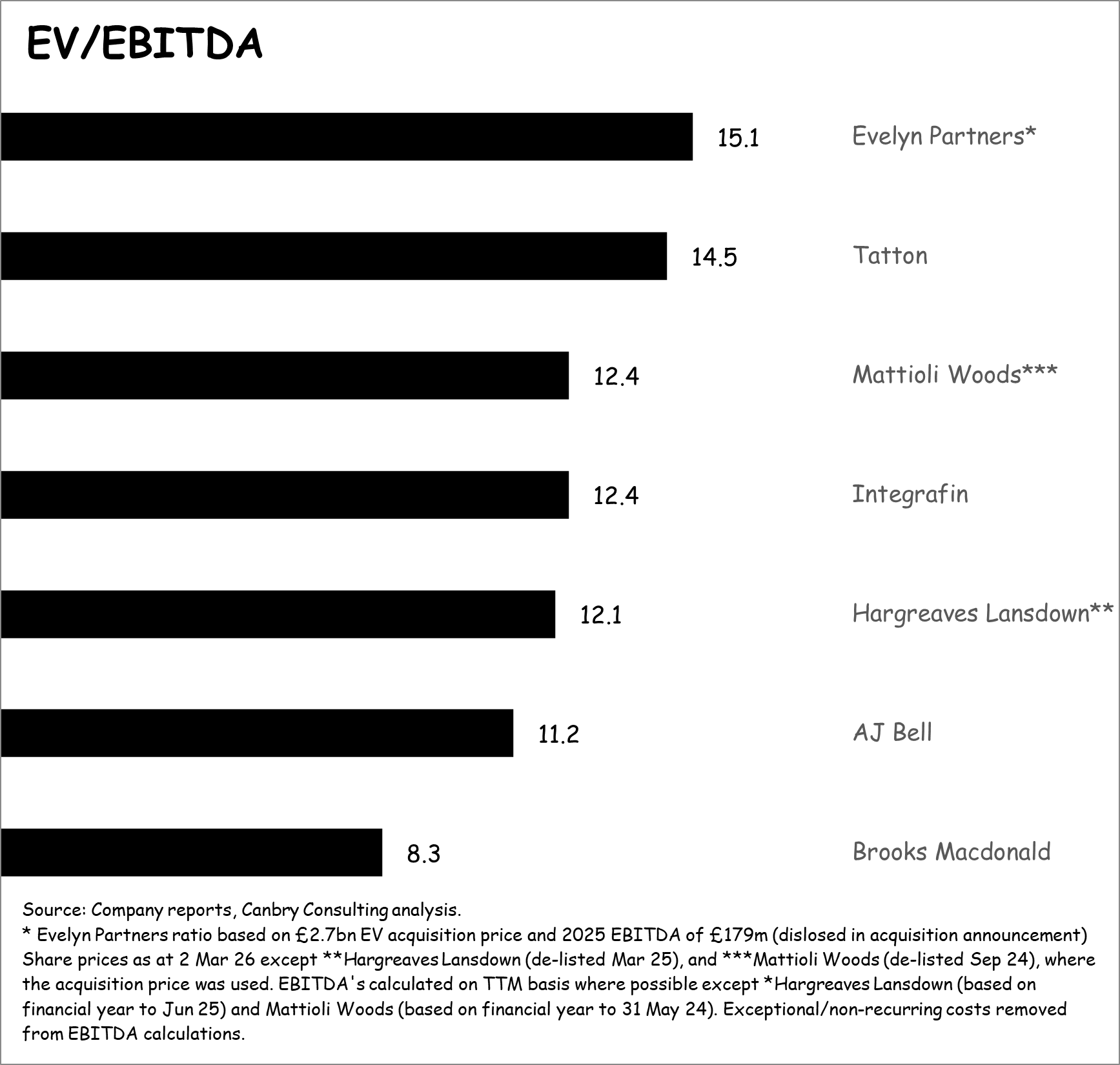

Because we don’t have access to Evelyn’s 2025 profits ‘below’ the EBITDA line, or to its latest balance sheet, the best valuation metric we have is probably the EV/EBITDA multiple, which is around 15. This is higher than the current valuation of all listed peers and the multiple paid for recent acquisitions.

Note the above chart is missing a few comparators, notably St James’s Place (SJP), Quilter, and Rathbones, where Enterprise Value and EBITDA are metrics which don’t make a lot of sense for comparative purposes. This is because of their financial structures. SJP and Quilter house long-term insurance licenses (used to provide clients with certain types of investment bonds and pension-related insurance structures). And Rathbones is a bank (even though its core business is wealth management, it uses its banking license to provide clients with some wealth-management-adjacent deposit and loan services - not transactional banking services).

…especially given fundamental performance

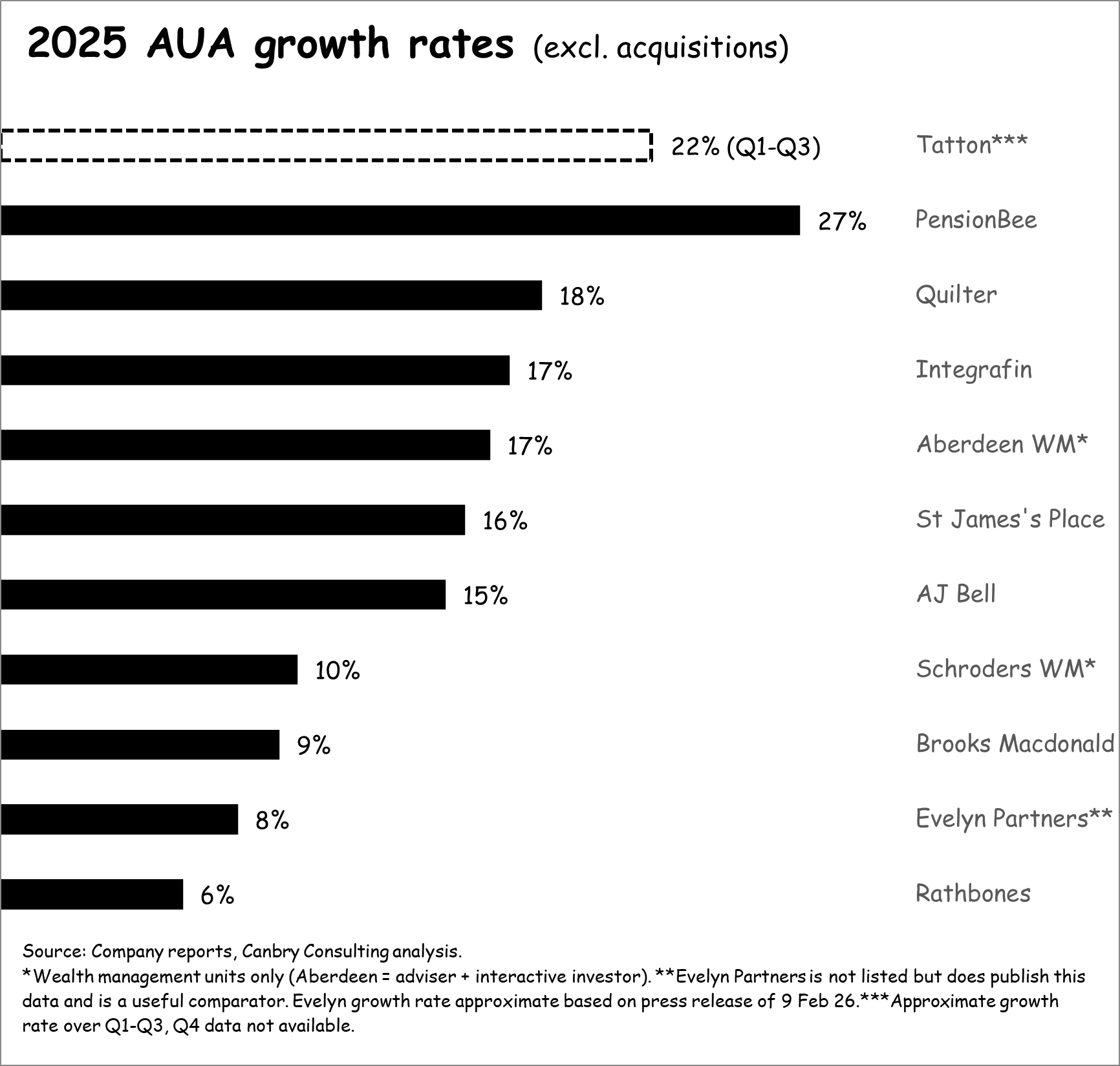

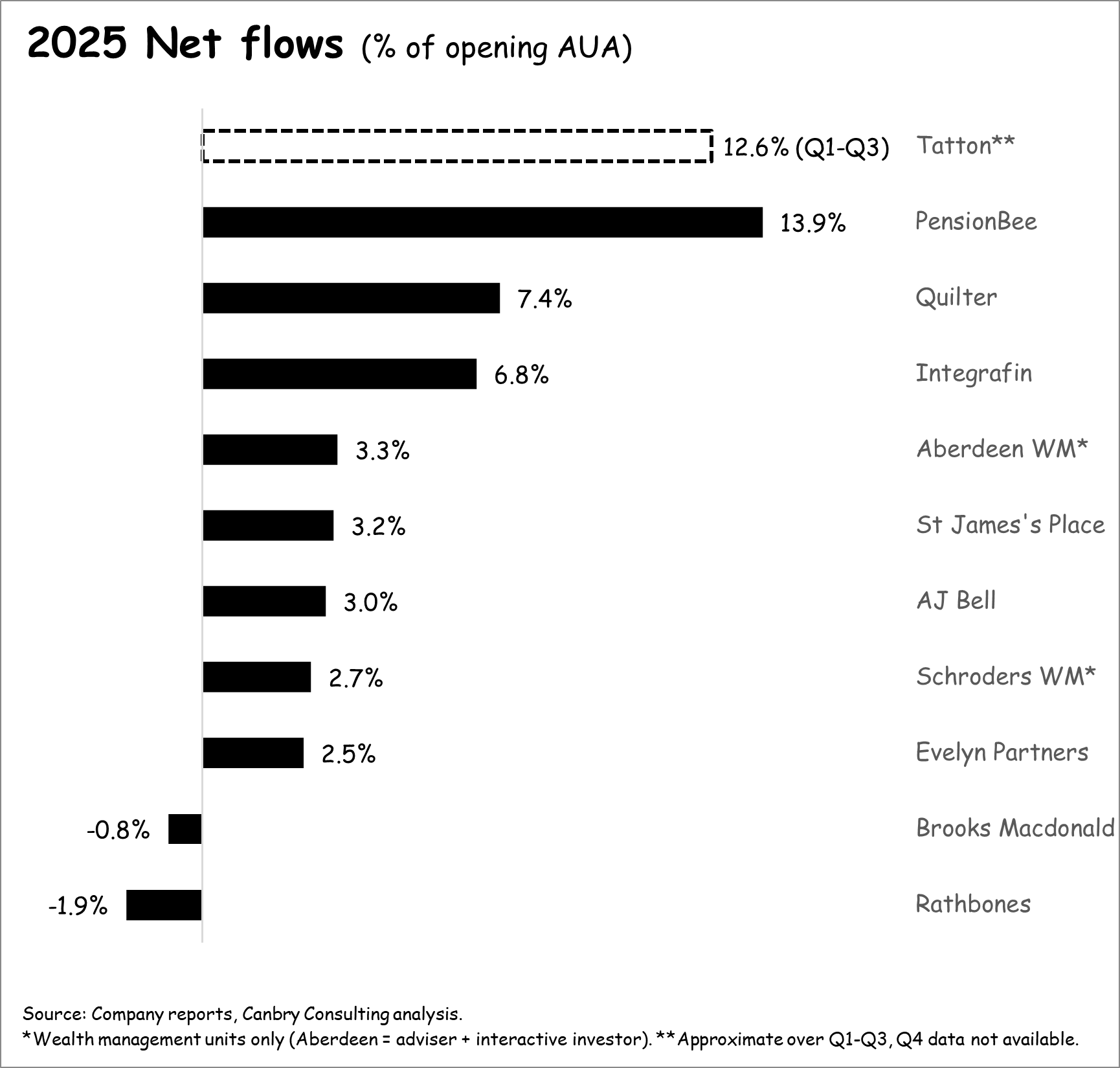

That acquisition multiple might not be a surprise at first glance, but when viewed through the lens of performance versus listed peers, it looks very punchy. While its valuation multiple is higher than peers, Evelyn had the second-weakest AUA growth in 2025…

…the third weakest net flow rate…

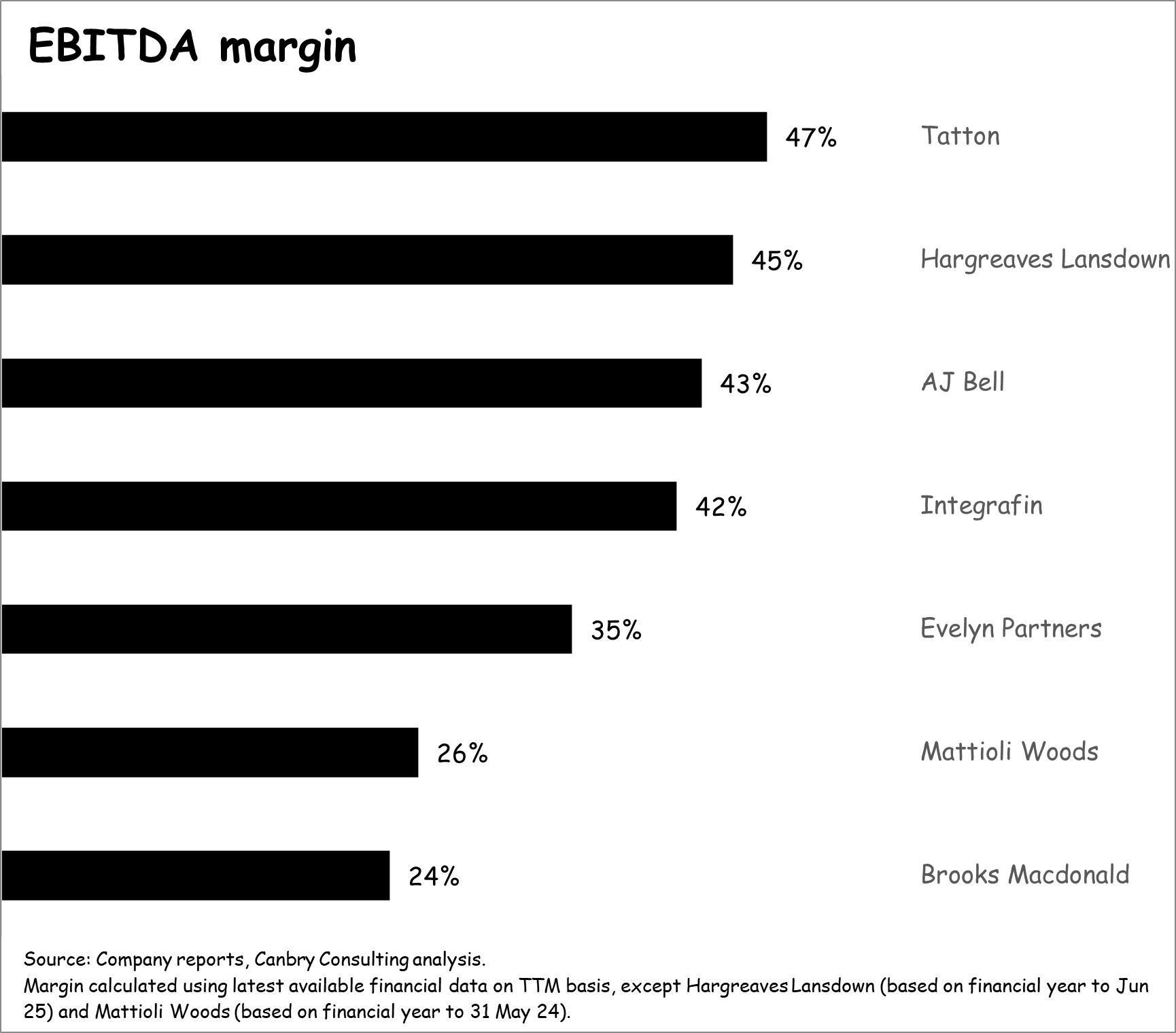

…and an OK but not that impressive EBITDA margin. (Furthermore, its statutory PBT is actually very low - see table above - mostly because of the amortisation charges related to previous acquisitions).

For a more comprehensive analysis of wealth managers’ performance in 2025, see my previous post:

NatWest’s rationale

The comments and comparisons above don’t mean that Evelyn won’t be a good acquisition for NatWest, it may very well be.

In its acquisition announcement, NatWest made the following points about deal rationale:

It diversifies NatWest’s income by increasing fee income (decreasing the proportion of net interest income).

It broadens NatWest’s wealth management offering (currently £59bn AUA compared to Evelyn’s £69bn) which is currently Coutts (high net worth) and NatWest Premier (mass affluent) - with what looks like a clear intention to cross sell across the group: “NatWest Group also intends to deliver significant revenue synergies through bringing Evelyn Partners’ leading financial planning and investment management solutions together with NatWest Group’s full suite of banking and wealth management solutions to our 20 million customers.”

It thinks there are significant cost synergies: “NatWest Group expects the combination of Evelyn Partners with its existing PBWM (private bank and wealth management) business to create material shareholder value, including estimated annual run-rate cost synergies of c.£100 million, equivalent to around 10% of the combined PBWM cost base, with costs to achieve of c.£150 million.”

NatWest management were eager to emphasise that the price made sense to them: “Evelyn Partners generated full year 2025 EBITDA of £179m, meaning that the transaction values Evelyn Partners at the equivalent of 9.7x 2025 EV to EBITDA multiple, including target run-rate cost synergies” (my emphasis).

A fun few minutes for those that are interested and have the time would be to listen to the deal announcement analyst call (from around 6 minutes) - where analysts try to get to the bottom of that ‘future’ 9.7x multiple.

Implications for the listed wealth management sector

NatWest have clearly been prepared to pay for a fair chunk of future synergies. With other large banks (possibly other large financial institutions too) sniffing around the wealth management sector, it’s worth thinking about the potential for acquisitions of London-listed companies, and the potential premium to current pricing that might be paid.

It’s not hard to imagine the strategic rationale for further acquisitions, for example:

With similar logic to NatWest, one of the other major banks could look to beef up its wealth and/or investment management offerings by acquiring say Quilter (£141bn AUA), or Rathbones (£116bn AUA). Quilter also brings a large adviser platform to the table. Rathbones is a bank, so you’d have to think there would be cost savings if acquired by another bank - two banking licenses wouldn’t be needed. The NatWest deal is not a one-off. RBC bought Brewin Dolphin in 2022, when Brewin’s AUA was around £52bn.

D2C platform businesses have been attractive to a range of buyers over the years - giving direct access to a client base and usually a scalable technology platform. Asset manager Aberdeen bought interactive investor in 2022; bank JP Morgan Chase bought Nutmeg in 2021; and insurer Aviva bought Wealthify in 2017 (the latter two were relatively small deals but the strategic rationale is the point here).

And then a host of players (including larger wealth/investment managers) might look at ‘buying scale’ in the fast-growing MPS (model portfolio service) space, by acquiring say Tatton, or Brooks Macdonald.

Then consider the multiple that might be paid if the Evelyn deal is anything to go by. Remember the Evelyn deal is being done at an EV/EBITDA multiple of 15x. That’s going to include an ‘acquisition premium’. And that’s for a company with a 2025 AUA growth rate of 8% and an EBITDA margin of 35%. Now compare that to two listed companies, just as examples:

Tatton currently trades at an EV/EBITDA multiple of around 14.5x (excluding an acquisition premium). But it grew AUA by 22% in just the first three quarters of 2025 (Q4 data not available), and by 30% in its FY to 31 Mar 24. Its EBITDA margin is around 47%.

AJ Bell currently trades at an EV/EBITDA multiple of just over 11x (excluding an acquisition premium). It grew AUA by 15% in 2025, with an EBITDA margin of 43%.

Putting the above strategic and financial points together, it’s not a stretch to suggest the following:

if you accept that the NatWest/Evelyn deal multiple is a reasonable benchmark; and

a large acquirer identifies a strong strategic rationale and/or synergies from an acquisition in the UK-listed wealth management space; then

that large acquirer will probably have to be paying substantially more than a 15x EV/EBITDA multiple (because most listed players have superior economics than Evelyn).

That is likely to mean the target company’s shareholders might realise a very large premium to current share price (given current EV/EBITDA multiples).

The alternative of course is that NatWest could be paying a price that is simply an outlier (on the expensive side). The passing of time and any future deals will show us which of the above is true. It’s going to be a fascinating sector to watch.

Be sure to subscribe to TheInvestors.blog below to keep up to date with further insights into the UK asset and wealth management sectors.

And if you think TheInvestors.blog is worth telling others about and sharing, I’d be most grateful if you do.

Disclosure: At the time of writing, Paul Bryant was a shareholder in a number of the companies mentioned in this publication and covered Tatton Asset Management as an analyst on behalf of Equity Development Limited. Read Equity Development’s research on Tatton here. And please read this link for the terms and conditions of reading Equity Development’s research.