Pollen Street results watch. A winner hit by narrative contagion?

Shares down 25% on a cocktail of private credit & AI disruption worries. That smells like narrative contagion. Iran has muddied the picture further. 26 March results should cut through the noise

TheInvestors.blog is not investment advice. Please read the disclaimer here.

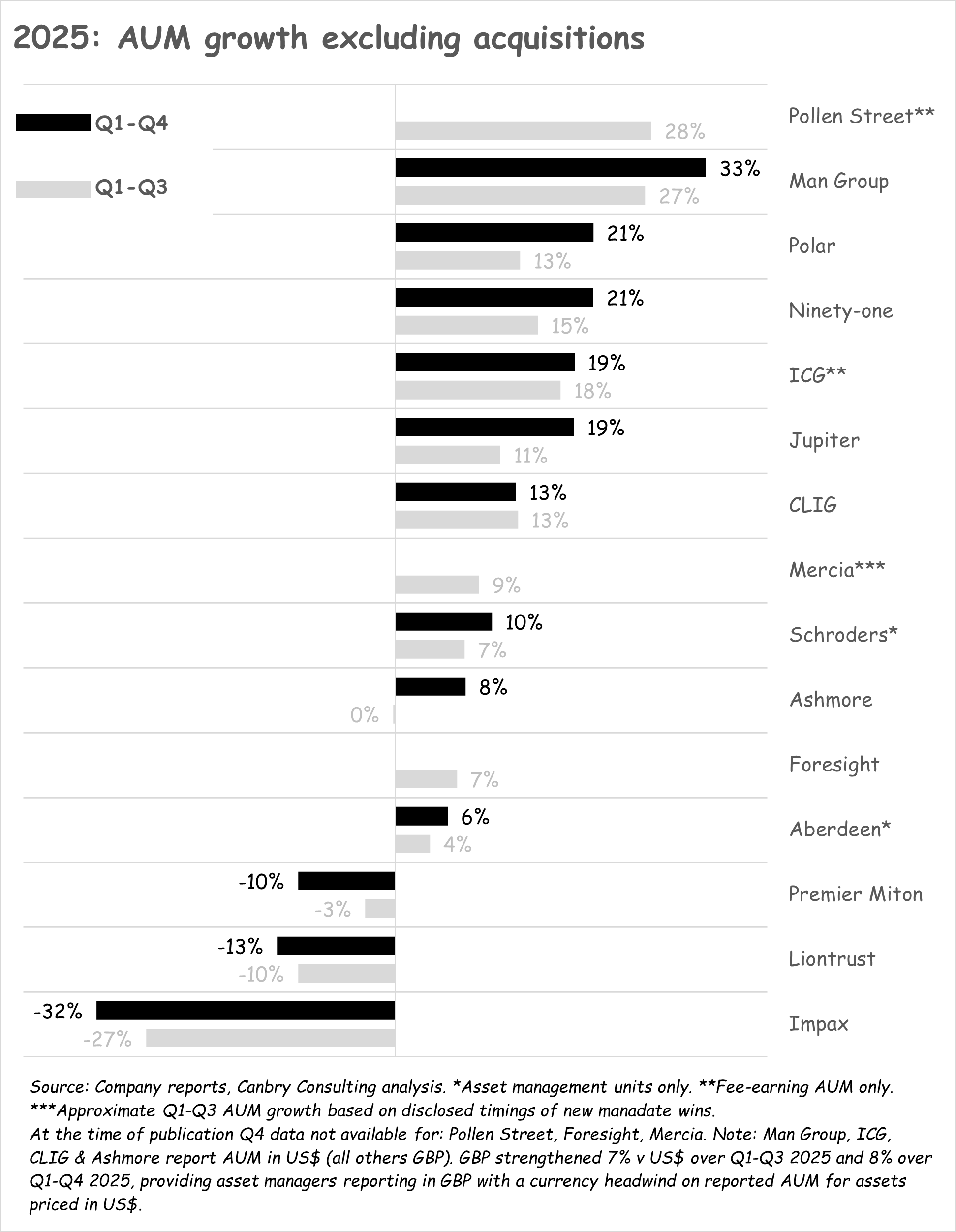

On fundamentals, Pollen Street has been a top performer. Based on its Q3 trading update from Nov 25, it’s probably going to be one of, if not the strongest performers when it comes to AUM growth among London-listed asset managers. We’ll get more details when it reports 2025 results on 26th March.

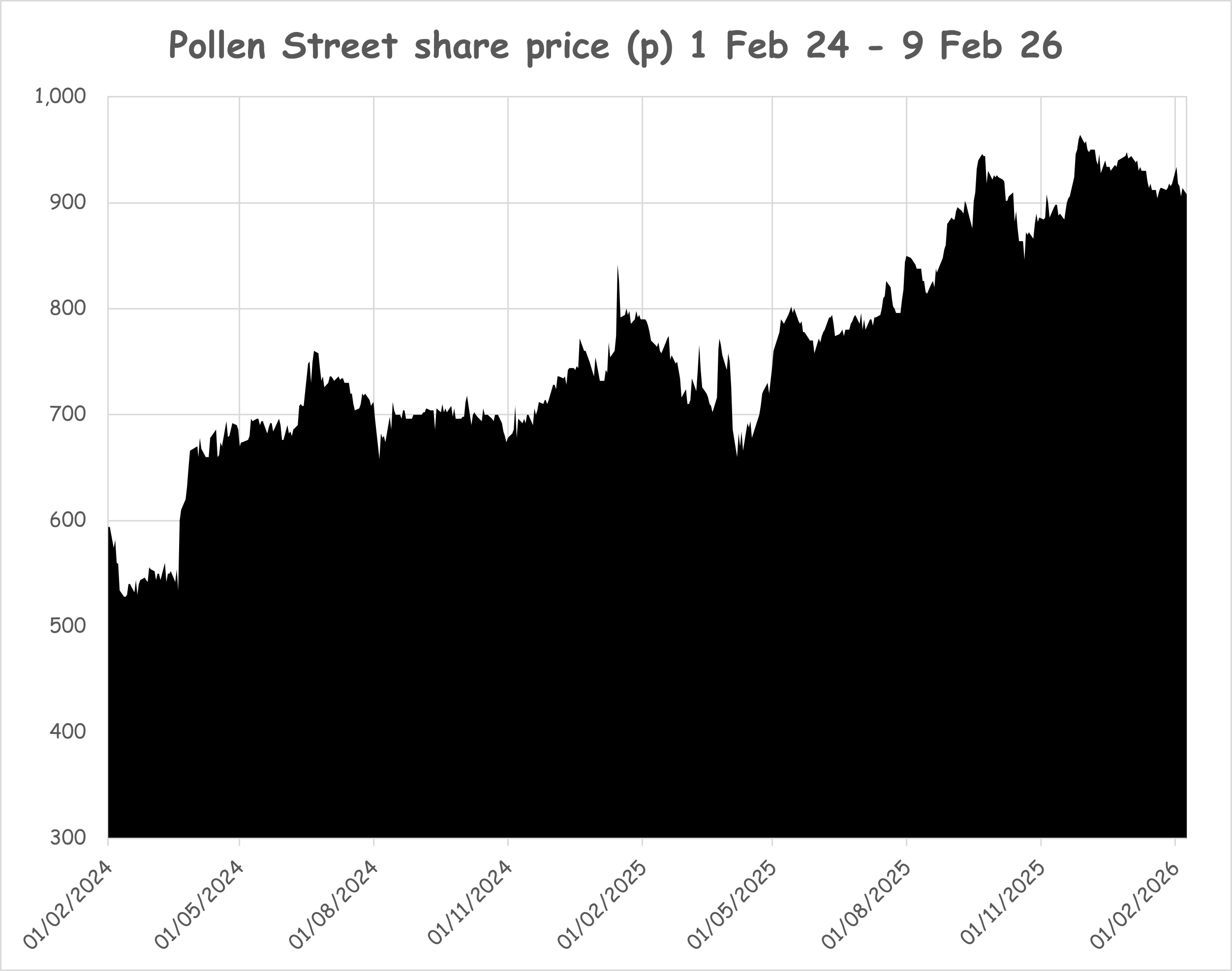

Until earlier this year, it looked like the share price priced recognised this. Pollen Street was priced as a ‘winner’. In this early-Feb 26 post, I wrote…

Three asset managers are clearly priced for higher earnings growth than others: Man Group, Pollen Street, and Ashmore. There’s a case to be made that this makes sense…

… (Pollen Street, the) private equity and private credit specialist is also showing strong growth at AUM and earnings level. Its funds are attracting significant interest from investors all around the world with a Q3 trading update (to 30 Sep 25) showing AUM up 32% y-o-y. EBITDA was up 28% y-o-y in the half-year to 30 Jun 25. The share price seems to have been in a reasonably solid uptrend over the last two years or so.

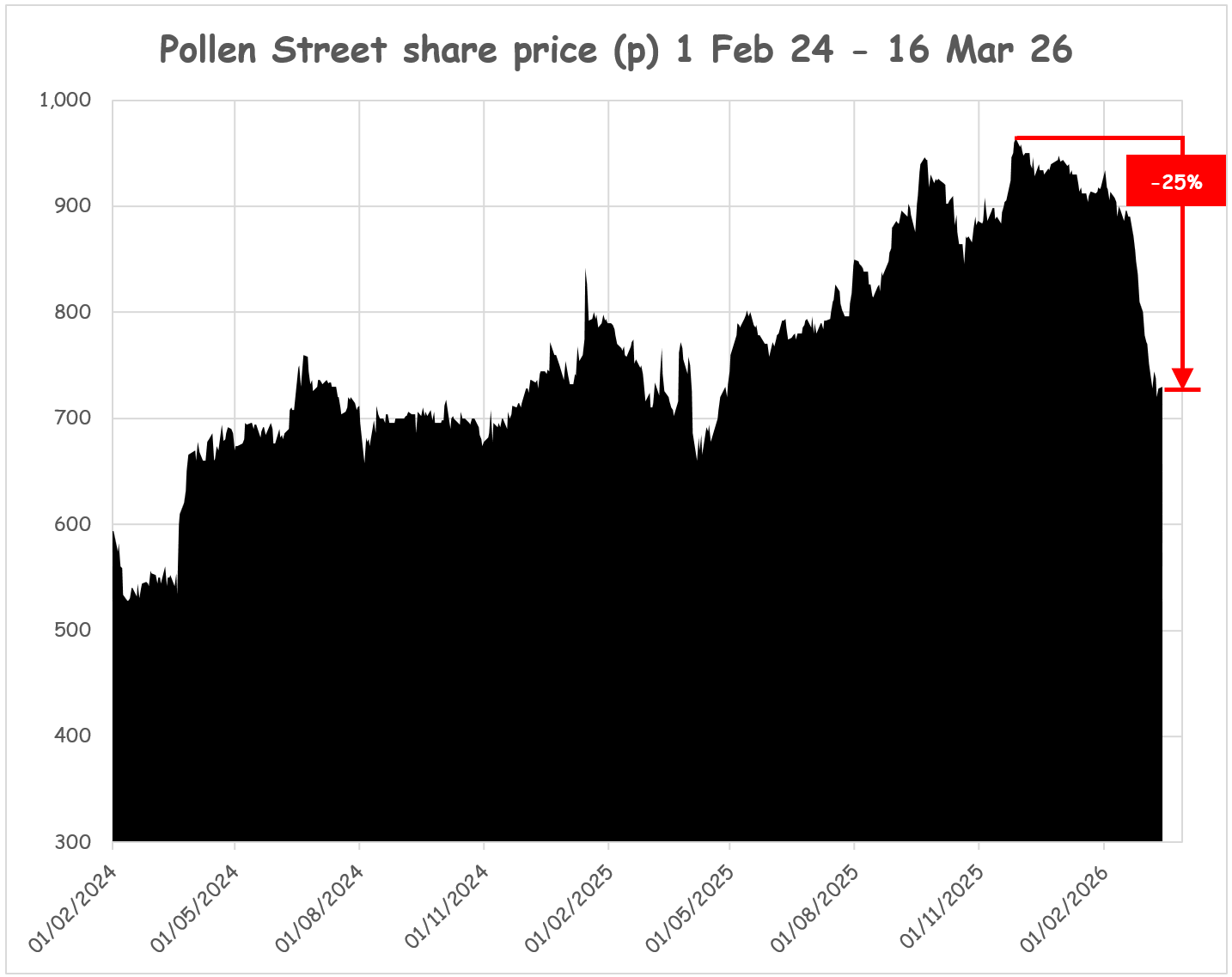

Just six weeks later, that last sentence from the quote above looks very dated! Here’s the updated chart.

That fall has been during a period of virtually no news from the company (RNS’s in 2026 are mostly details of the ongoing share buyback programme and an announcement of some directorate and committee changes - nothing that you’d expect to be needle-moving).

But here’s what did happen in markets:

Private credit fund worries accumulate…

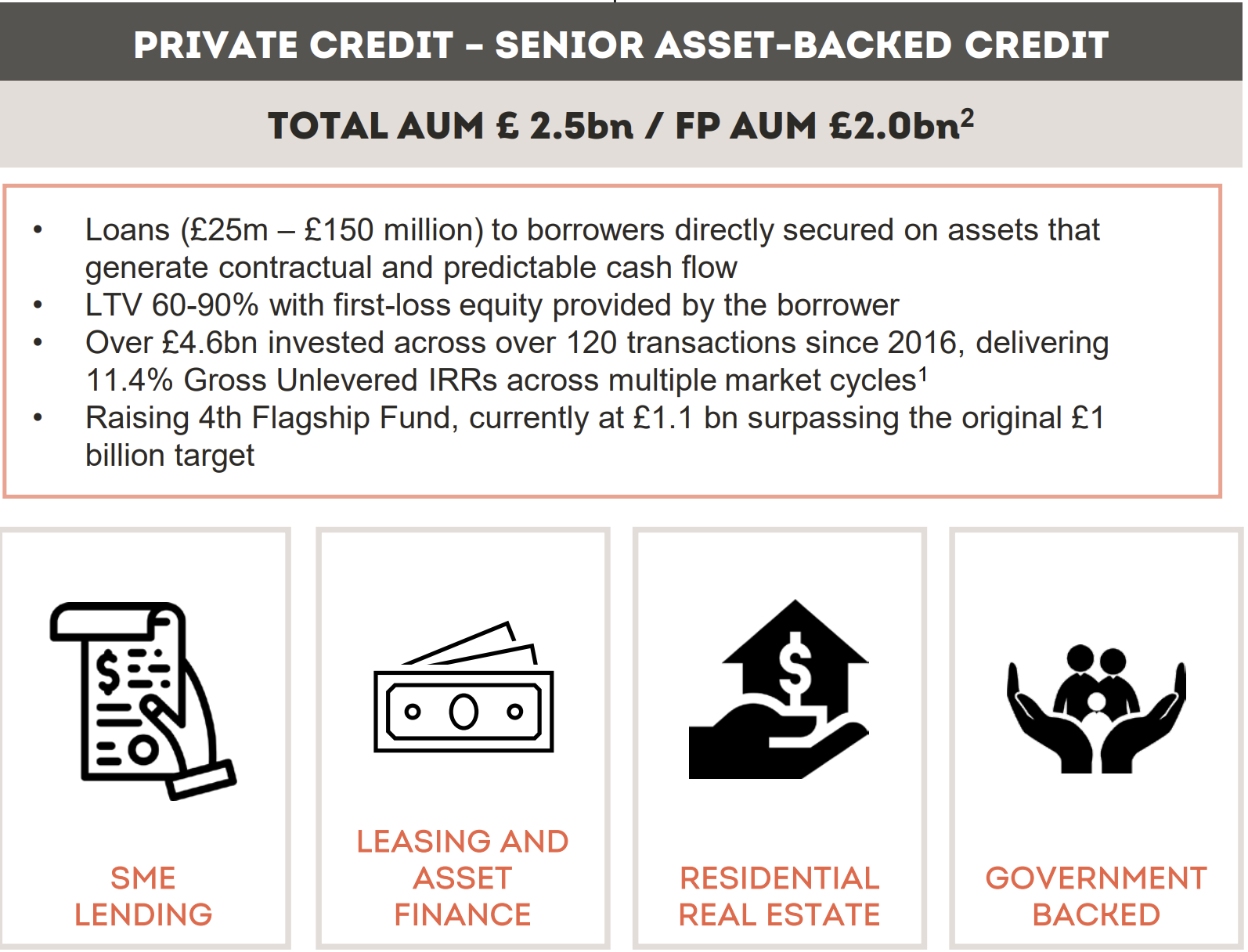

Around 37% (£2.5bn) of Pollen Street’s AUM is in private credit (senior asset-backed credit). The balance is private equity.

But a slow burn of worry around private credit and private credit funds seems to have just accumulated over recent months, and hit the shares of many players in this space - hard (see below). In the US, worries really ratcheted up in Sep and Oct 25 with the Tricolor and First Brands debacles, and Jamie Dimon’s subsequent and now-infamous “when you see one cockroach, there are probably more” comment during the JPMorganChase Q3 2025 earnings call.

Then a bunch of private credit funds restricted or looked to change the terms of withdrawals/redemptions, including funds run by Blackrock, Blue Owl, Morgan Stanley, Cliffwater, and Blackstone. This spurred more widespread worries about the quality of underlying portfolios.

Amidst all of this the problem turned into an AI-linked issue with the launch of new professional-task automation tools by Anthropic. As many private credit loans (especially in the US) have been made to software companies - which some deem to be at risk of massive disruption from AI - the consequence is supposedly a decline in the quality of many private credit portfolios.

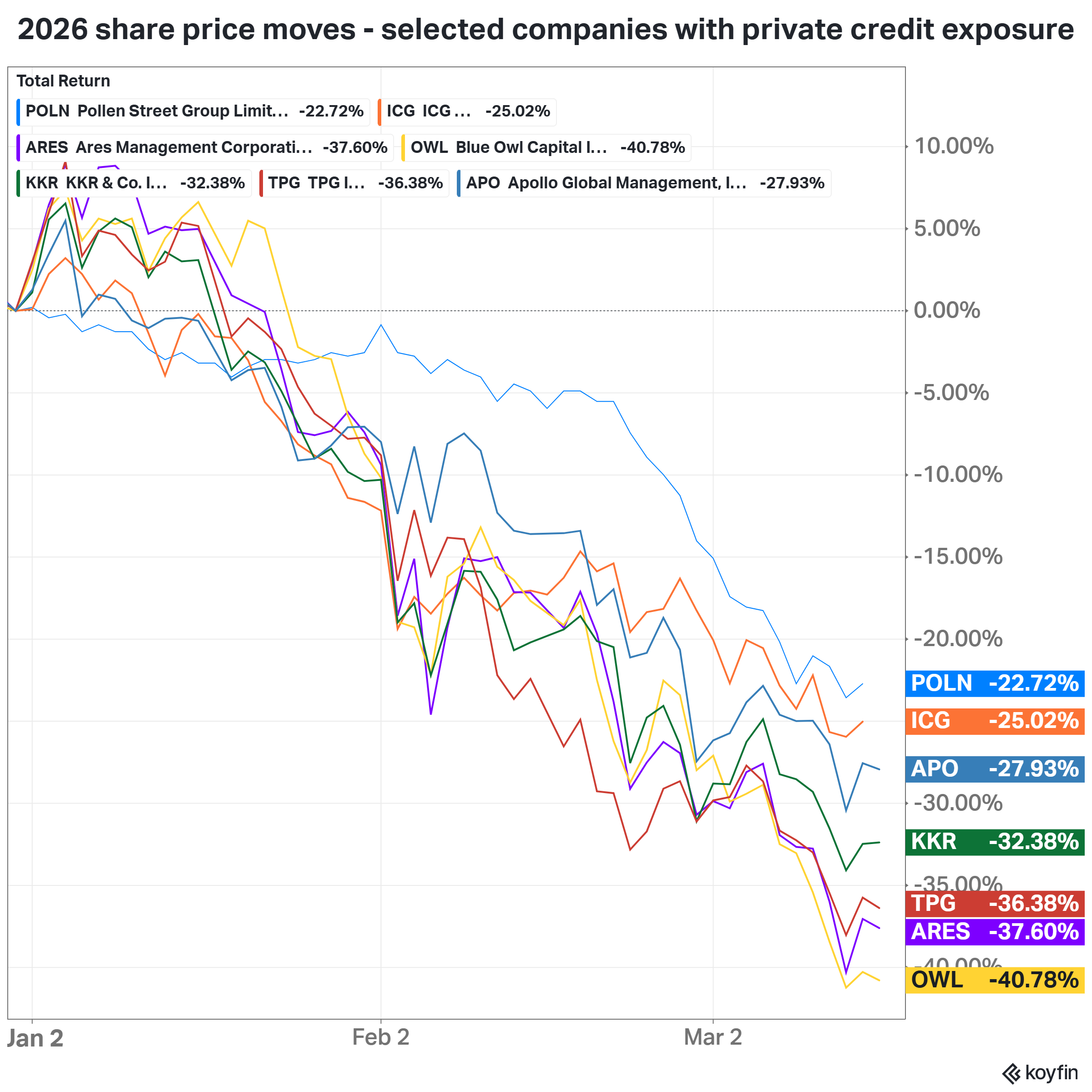

And it really does look like London-listed Pollen Street and ICG (both with private equity and private credit funds) have been dragged down by concerns across the pond (all companies in the chart below are US-listed except POLN and ICG).

…but Pollen Street seems distant from these concerns

Pollen Street’s private credit business seems quite distant from the issues associated with portfolio quality concerns in the US. Here’s a summary of its private credit activities from a company presentation.

Not only is there a geographic distance with 90% of Pollen Street’s lending deployed in Europe (incl. the UK). But one of the key differences between Pollen Street and some of the major concerns in the US (which are often associated with loans to software and other companies), is that Pollen Street’s portfolio is largely asset-backed lending, versus corporate lending.

That means the underlying loans in Pollen Street’s portfolio are underpinned by assets which generate returns to repay loans, and these assets can be taken over by the lender and sold to recoup any losses if the borrower gets into difficulty. Corporate lending on the other hand would be relying on the performance of a business (e.g. a software company) to generate cash flow to repay a loan (although some of these loans will have collateral too).

In November 2025, Pollen Street held a Private Credit Teach In, which is an hour or so of really drilling down into the weeds of its private credit business. It’s freely available, and I would recommend any shareholder or potential shareholder watch the whole thing to improve their understanding of what Pollen Street’s private credit business really is.

AI concerns spill into Private Equity too

It’s also possible that some of Pollen Street’s share price fall from just before mid-February could have been related to AI concerns around its private equity portfolio. This portfolio has a very tight sector focus, as illustrated below (source: Pollen Street).

And some of these sectors are in the crosshairs of AI disruption worries too. This (10th Feb 26) Bloomberg article - Wealth Manager Stocks Sink as Traders Flee Next AI Casualty - sums it up:

An artificial intelligence tool aimed at creating tax strategies sparked a selloff in wealth-management stocks Tuesday as investors fear the business could be at risk from automated advice.

The innovation puts the wealth-management industry in the crosshairs of AI competition, the way it did for software stocks and private credit firms last week and insurance brokerage shares on Monday.

But this story and some of the market moves around it seem very much based on “narrative contagion”, where the share prices of companies in specific sectors get hit because of AI concerns - often when a new AI sector-specific tool is released.

These moves look panicky and without deep fundamentals-based research, but they are more than blips. For example, at time of writing, UK wealth manager St James’s Place had only recovered 6% of the 20% fall which took place between 10 and 16 Feb 26.

Iran war muddies picture further

Of course, on top of some of these sector-specific reasons for Pollen Street’s share price fall, is the broader market turbulence brought about by the war in Iran and its fallout.

We just don’t know how this will impact Pollen Street yet.

What I do expect though, is for the results commentary and presentation on 26th March 2026 to shed some light on exactly where Pollen Street stands in relation to some of these widespread market concerns, and if it can shrug off narrative contagion. I’ll be writing about those results, so be sure to subscribe below.

Subscribe to TheInvestors.blog to keep up to date with the UK asset and wealth management sectors.

And if you think TheInvestors.blog is worth telling others about and sharing, I’d be most grateful if you do.

Disclosure: At the time of writing, Paul Bryant was a shareholder in Pollen Street.