TheInvestors.blog is not investment advice. Please read the disclaimer here.

My Equity Development research note covering Tatton Asset Management’s H1-26 is out.

You can read the full note here.

You can see the management presentation and Q&A with investors here.

And here is the summary of my note:

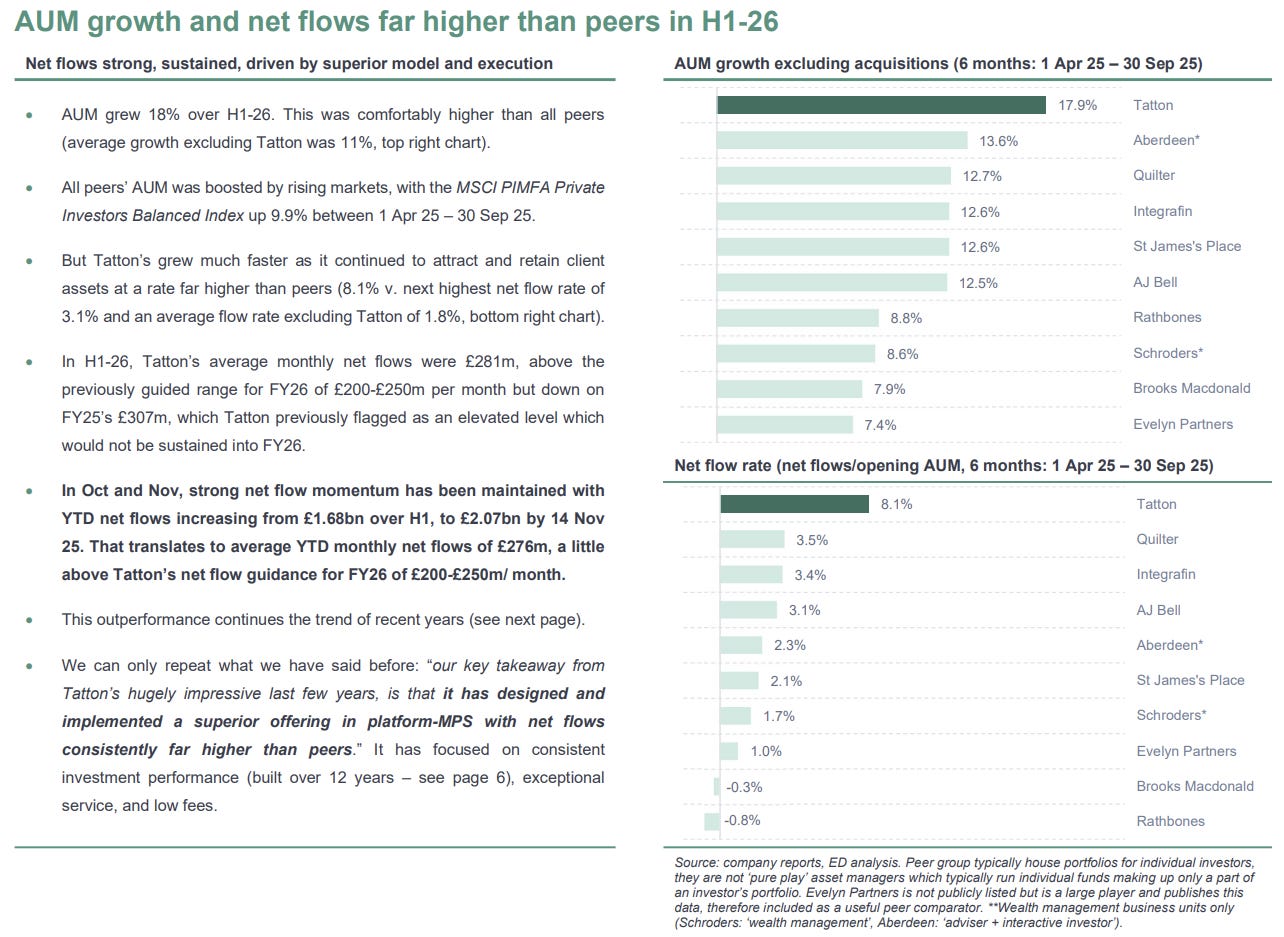

After its Oct 25 trading update, we knew Tatton had maintained its exceptional growth momentum; Assets-Under-Management/ Influence (AUI) were up 18% over H1-26, and net flows remained strong at £281m/ month, above Tatton’s guidance for FY26 of £200-£250m/ month. In the post-results period, AUI growth has continued, up another 5% to £27.1bn on 14 Nov 25. YTD net flows have increased from £1.68bn over H1 to £2.07bn.

With more recent peer data becoming available, we now also know H1 growth and flows were far higher than all peers. And we know H1 growth has translated to an exceptionally strong set of financial results with revenue, profits and net cash all sharply up. Compared to peers, and especially given the macro environment, it is a truly impressive performance.

The balance sheet remains strong with no debt and net cash up 6% over H1 to £34.1m (after paying the final FY25 dividend of £5.7m). An interim dividend of 12.0p is proposed (+26%; H1-25: 9.5p).

We highlight that even after fully acknowledging current macro-economic headwinds and UK budget uncertainty, management’s outlook is strong. Near-term, Tatton has “confidence in delivering results in line with market expectations”. Longer-term, Tatton has “confidence in achieving the £30 billion AUM/I target by FY29”. We note Tatton is ahead of trajectory to deliver on that goal.

Given current momentum, our FY26 forecasts probably look conservative. However, markets are volatile, and we err on the side of caution, maintaining our forecasts and fundamental value of 750p per share.

Be sure to subscribe to TheInvestors.blog below to keep up to date with the UK asset and wealth management sectors.

And if you think TheInvestors.blog is worth telling others about and sharing, I’d be most grateful if you do.

Disclosure: At the time of writing, Paul Bryant covered Tatton Asset Management as an analyst on behalf of Equity Development Limited. Read Equity Development’s research on Tatton here. And please read this link for the terms and conditions of reading Equity Development’s research.