Want to know how UK asset managers differ from each other? 2022’s bear market will show you!

Nearly all asset managers were hurt by negative investment performance in 2022. But capital flows from clients varied hugely between managers. Here's a look into what's going on.

What a difference a year makes

'A rising tide lifts all boats' has some credence when looking at asset managers' (AMs) growth in a bull market. In fact, in 2021, all but one UK-listed AM recorded AUM growth, with a sector median increase of +13% (excluding the impact of acquisitions).

2021 AUM movement excl. acquisitions

That all changed in 2022. Markets turned bearish, and most AMs saw significant AUM reductions, with a median fall of -17%.

2022 AUM movement excl. acquisitions

These AUM movements were influenced by two main factors: investment performance and net flows (new client capital placed with an AM less client capital withdrawals).

Asset class focus a key influence on investment performance

For many, most of the 2022 fall was attributable to the impact of investment performance, with a median negative impact on AUM of -12%.

2022 Investment Performance as % of opening AUM

Two AM’s stand out for their relatively strong investment performance, which was mostly driven by having a high concentration of assets in alternative or ‘non-mainstream’ classes.

Gresham House’s positive performance was mostly attributed to the valuation uplifts of assets in its Forestry division (44% of AUM) and New Energy and Sustainable Infrastructure division (23% of AUM) – both of which invest directly in ‘real’ or physical unlisted assets (with relatively low correlation to equity markets and inflation, according to its annual report – see below).

Man Group’s investment performance was boosted by a strong performance from its absolute return strategies (32% of AUM) which are designed to benefit in rising or falling markets.

Conversely, some AMs’ investment performance was hit hard by having a high concentration of assets in classes that had a particularly bruising 2022, for example:

City of London Investment Group (CLIG) has around 40% of AUM in emerging market equities, where the MSCI EM Index fell 20% in 2022;

Liontrust has around one-third of AUM in sustainable investments, where the FTSE Environmental Opportunities All-Share Index fell 24% in 2022; and

Ashmore has over 80% of AUM in emerging market debt, where EM debt indices fell between 10% and 20% in 2022, depending on the type of debt.

Meanwhile some investment performances, while negative on an absolute basis, could be considered as good performances on a relative basis, for example:

Impax, with 95% of AUM in listed sustainable equities, recorded a -12% investment performance compared to the FTSE Environmental Opportunities All-Share Index (-24%); and

Polar Capital, with around 37% of AUM in technology equities, recorded a -15% investment performance compared to the Dow Jones Global Technology Index (-35%).

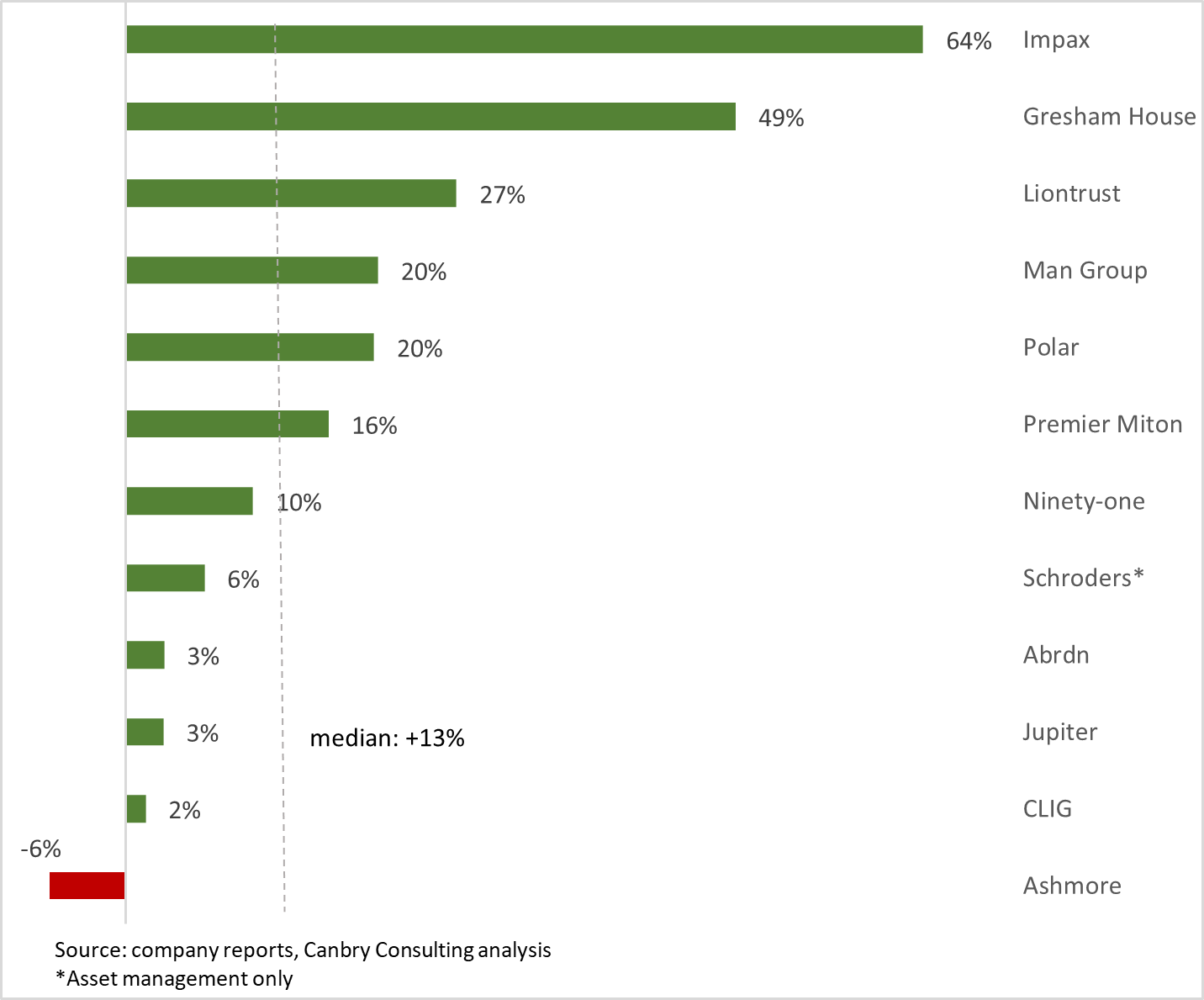

Hidden messages in net flow data

Net flows in 2022 meanwhile showed a much greater divergence between companies.

2022 net inflows, % of opening AUM

Three main factors influenced this divergence.

1. Investment performance’s ‘double whammy’ effect

The first factor is investment performance, which in addition to its direct impact on AUM levels as discussed above, has an indirect impact on AUM levels via its influence on net flows - it can have a ‘double-whammy’ effect.

This could be because of sector rotation, as investors divest out of poorly performing asset classes (or vice versa as was seen in 2021). Or in some cases, it could be because of a loss of confidence in an individual AMs investment ability.

Examples of market-level sector rotation in 2022 included:

emerging market bonds, which saw the biggest outflows on record, according to JP Morgan1;

technology-themed funds, where global net fund flows fell 106% from +US$96bn in 2021 to -US$6bn in 20222; and

sustainable funds, where global net fund flows fell 76% from +US$700bn in 2021 to +US$170bn in 20223 (although notably net flows remained positive).

The effects of this correlation between sector-level investment performance and company-level net flows can clearly be seen in some AMs with a high proportion of AUM in asset classes which performed poorly in 2022, including: Ashmore (emerging market debt); Polar Capital (technology equities); and Liontrust (sustainable investments).

Conversely, on the positive side, Gresham House conducted a number of successful fund raisings during the year, boosting inflows, stating in its annual report: “investors recognised the resilient nature of sectors with less correlation to equity markets and inflation” (referring to real assets such as forestry).

Notably, some AMs bucked the sector investment performance / net flow correlation to a degree. Impax still managed to record positive net flows despite sustainable investments performing very poorly (however as previously noted, its investment performance was better than the sustainable market more generally).

2. Retail investors quicker to withdraw funds

The second factor influencing flows, particularly in a bear market, is the relative exposure to retail versus institutional investors, with retail investors tending to be more skittish when it comes to withdrawing funds during market downturns.

For example, CLIG and Jupiter both saw stark flow differences between institutional investors (positive flows) and retail investors (negative flows) in 2022. CLIG’s CEO wrote: “loss aversion is higher in retail investors, which can trigger greater redemptions in uncertain times, such as experienced in 2022”. While Jupiter’s annual report stated: “Volatile markets and challenging economic conditions weighed upon investor sentiment, particularly in the retail channel in the first half. Despite this, we saw record net inflows in the institutional channel.”.

Liontrust’s net outflows were also mostly driven by its substantial retail investor base (around 70% of AUM), although worryingly, its institutional channel also experienced outflows.

3. Fund structures can be an accelerant or a brake on flows

A third factor – fund structures – has almost certainly played a role in the strong relative flow position of Gresham House (which had the strongest net flows in 2022).

Its most common fund structures are long-term investment vehicles such as Limited Partnerships (suited to investments in real assets such as forestry and sustainable infrastructure), which don’t provide for rapid withdrawal of funds i.e. investors are ‘locked-in’ for a period. Therefore, in an environment when net outflows from funds are common, these types of fund structures will tend to have a strong relative net flow performance.

A maze for investors to navigate

Of course, all three of the above factors can work in the other direction given different market conditions.

Battered sectors can come back into favour and attract capital from previous ‘darlings’. The adjective of ‘skittish’ applied to retail investors who exit sectors first, could change to ‘nimble’ if they are quicker to re-enter sectors with positively changing fortunes. And open-ended fund structures - which have exposed some AMs to faster outflows - also allow for faster inflows, which could turn out to be a relative advantage for some AMs over those with predominantly longer-term investment vehicles.

Investors in the sector are left with a complex maze to navigate. There are certainly high-flyers and strugglers in the asset management sector at the moment. But teasing out market versus company specific factors and cyclical versus structural factors are just some of the issues investors need to get their heads around to establish robust company-level outlooks.

As we head into Q1-23 reporting season, I’ll be watching carefully for continuations or reversals of the above 2022 trends, and be commenting on these developments in future newsletters. Make sure to subscribe not to miss these updates.

Please read the Investing in the Investors disclaimer here.

Disclosure: At the time of writing, Paul Bryant was a shareholder in a number of the companies mentioned in this publication, and covered Impax Asset Management and Polar Capital as an analyst on behalf of Equity Development Limited. Read Equity Development’s research on Impax Asset Management here, and on Polar Capital here. (Please read this link for the terms and conditions of reading Equity Development’s research).

Financial Times, 2 October 2022, Outflows from emerging market bond funds reach $70bn in 2022

Morningstar, Global Sustainable Fund Flows: Q4 2022 in Review