Worrying quarter for wealth managers

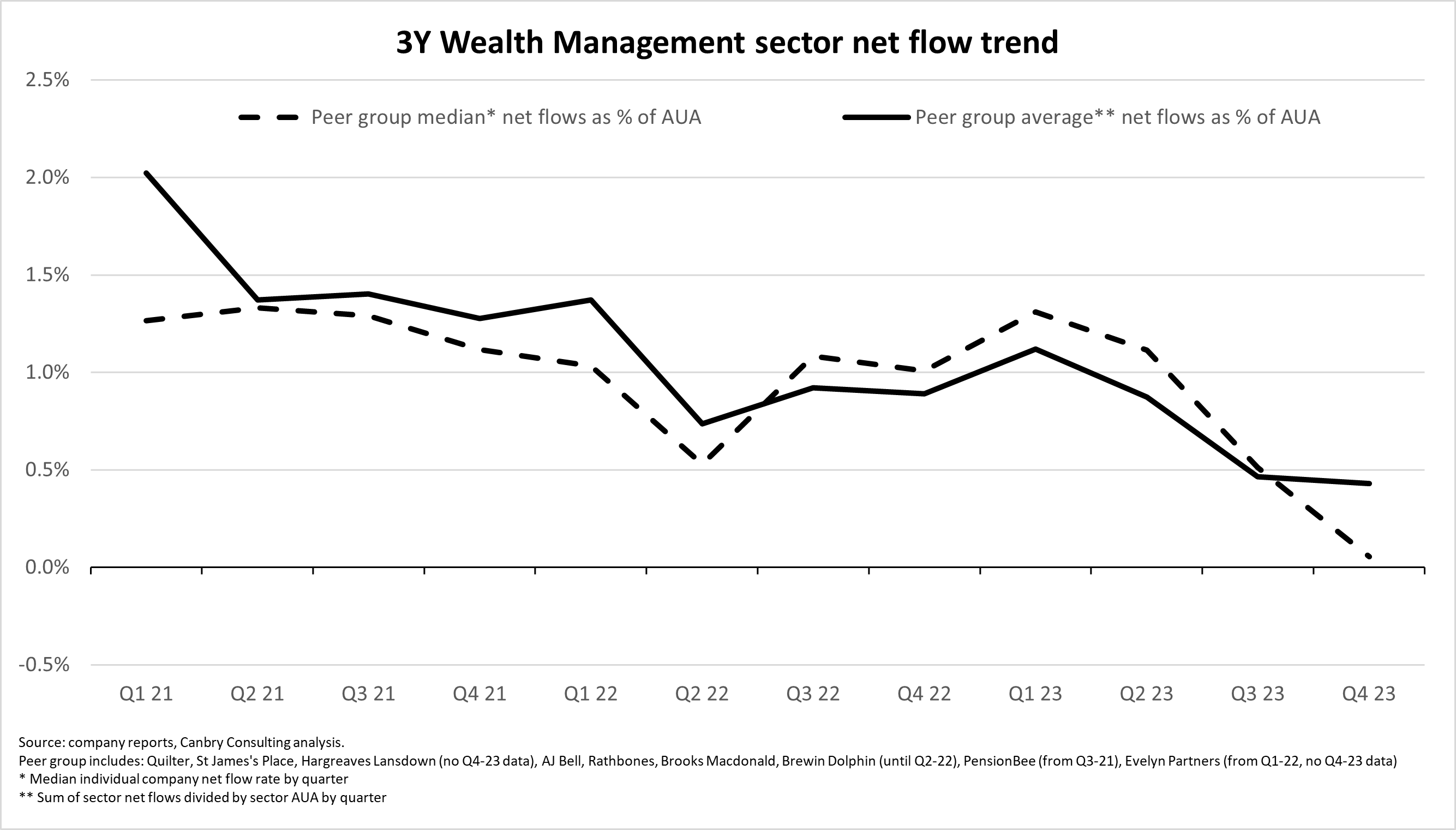

Q4 of 2023 saw strong markets mask weaker flows

This is not investment advice. Please read TheInvestors.blog disclaimer here.

The UK-listed wealth management sector (including wealth managers, investment managers and platforms) appeared to have a rosy enough Q4 of 2023, with some strong AUA/AUM gains.

Buoyant markets, weakening flows

It was buoyant markets that provided the boost. The MSCI PIMFA Private Investors Balanced Index rose 5.5% over the quarter. Meanwhile, net flows were a mixed bag during the quarter.

But comparing aggregate net flows to previous quarters - a worrying downtrend is evident.

Conflicting views on retail investor sentiment

A few companies have highlighted common themes being responsible for these weakening flows:

St James’s Place (25 Jan 24 trading update): “client capacity and confidence to commit to long-term investment have been impacted by the economic environment and short-term alternatives in the form of cash deposit and savings rates”.

Brooks Macdonald (12 Oct 23 trading update) “we saw net outflows, driven by the volatile macroeconomic backdrop and continuing high interest rates, which are leading clients to move towards higher cash holdings, debt repayment and investment in money market funds”.

Rathbones (19 Oct 23 trading update): “a market backdrop that remains challenging and higher outflows as clients use funds to repay debt or prefer to hold assets in cash for the short term”.

But AJ Bell struck a more positive tone in its 18 Jan 24 trading update: “Some of the macroeconomic headwinds experienced throughout 2023 showed signs of improving in the quarter, driving global equity markets higher and easing some of the pressure on household finances. Platform net inflows … were up 63% on … the prior year, reflecting increased confidence among retail investors”.

So there are some conflicting opinions on the state of the UK retail investor. It will be especially interesting to see the comments of the UK’s largest D2C platform, Hargreaves Lansdown, when it releases its interim results on 22 Feb 24, and beyond that, to see if the ‘green shoots’ flagged by AJ Bell translate to a wider pickup in flows.

But let’s look at individual company performances.

PensionBee growth strong but slowing, bigger emphasis on profitability

Being an earlier-stage and smaller company than others in this analysis (£4.4bn AUA compared to next-smallest Brooks Macdonald: £17.6bn), it is a special case.

It’s net flow rate has been far higher than peers since its IPO in Apr 21, but that was off a much smaller AUA base.

And while its growth certainly slowed in Q4 of 23, this was impacted mostly by ratcheting down marketing spend over H2-23 (£2.9m versus £6.8m in H1-23). No doubt, this was in-part to deliver on its IPO target of reaching adjusted EBITDA profitability (on a monthly basis) by end-23 (which it did). PensionBee has stated that it intends to manage the growth versus profitability equation in favour of profitability going forward.

Because of this, I expect growth to be lower than in the recent past, but still well above sector averages. The marketing spend vs growth equation at PensionBee is becoming clearer, with the cost of customer acquisition continuing to fall.

For a more detailed analysis, see my recent Equity Development research note here: Growth still strong, adjusted EBITDA turns positive in Q4.

AJ Bell engine purring

Once again, another strong AUA growth performance from AJ Bell. It’s been a consistent high-flyer and has provided another positive outlook.

You can see a more detailed analysis of AJ Bell’s business in my Q3-23 post here

St James’s Place: further shake-ups afoot?

SJP has historically been a very strong performer when it comes to attracting and retaining client assets. Its net inflows were some distance above the sector average in 2021 and 2022, but since then, have dropped off rapidly.

The group has come under huge pressure from regulators recently over its high fees (which were duly cut), triggering a major fall in its share price. And perhaps, all the noise around fees made clients think twice about their SJP investments over the last year or so, depressing net flows.

It’s certainly a group in flux, with its latest trading update alluding to more changes ahead: “as we start planning our vision for 2030 I am reviewing all elements of our business to ensure we are fully fit for the future and best placed to keep delivering for all our stakeholders."

Waiting for Quilter & Rathbones to deliver

Both of these businesses have underperformed when it comes to growth.

At Quilter, the tone of the most recent outlook statement is bullish:

“The Quilter channel continues to drive strong net flows in both our Affluent and High Net Worth segments. Our focus on reshaping our Advice business is demonstrating clear results, with Quilter channel gross sales per Quilter Adviser increasing 21% on the prior year comparative period.

Our actions to enhance the proposition of our Platform continue to bear fruit. We saw 44% year-on-year growth in fourth quarter gross new business from IFAs onto our Platform in our Affluent segment, resulting in us moving back into a position of net inflows in this channel during the final quarter.”

But shareholders are still waiting for a group-level substantial uptick in net flows.

At Rathbone’s, in the near-term, it’s all about the Investec W&I acquisition (concluded Sep 23). The deal has moved AUA up from around £60bn AUA to £105bn.

However, the first quarter of the combined group was a tricky one. The “Rathbones” discretionary and managed services recorded net inflows of +£392m, but the acquired businesses of Investec and Saunderson House had negative flows of -£327m and -£98m respectively, with a negative net flow position of -£222m at group level.

Weak period for Brooks Macdonald, changes to turn tide?

Brooks Macdonald was an outperformer for much of 2022 and early-2023, but did experience weaker net flows in H2-23 (solid inflows, but higher than normal outflows).

The business has undergone organisational changes and multiple staff changes at senior levels over the last year or so. Shareholders will now be looking for a period of stability and for the changes to turn the net flow tide.

For a more detailed analysis of Brooks Macdonald, you can read my recent Equity Development research notes: FUM up 4.3% in quarter, profit forecast upgraded a touch and Tech investments pave way for staff cuts & margin upside.

Subscribe below to keep up to date with the UK wealth management sector. I’ll be looking for further clues on the outlook as more results come in, and will soon be writing about Mattioli Woods (6th February), Hargreaves Lansdown (22nd February), and Schroders (29th February).

And if you think TheInvestors.blog is worth telling others about and sharing, I’d me most grateful if you do.

Please read theInvestors.blog disclaimer here.

Disclosure: At the time of writing, Paul Bryant was a shareholder in a number of companies discussed in this post, and covered Brooks Macdonald and PensionBee as an analyst on behalf of Equity Development Limited. Read Equity Development’s research on Brooks Macdonald here, and PensionBee here (Please read this link for the terms and conditions of reading Equity Development’s research).